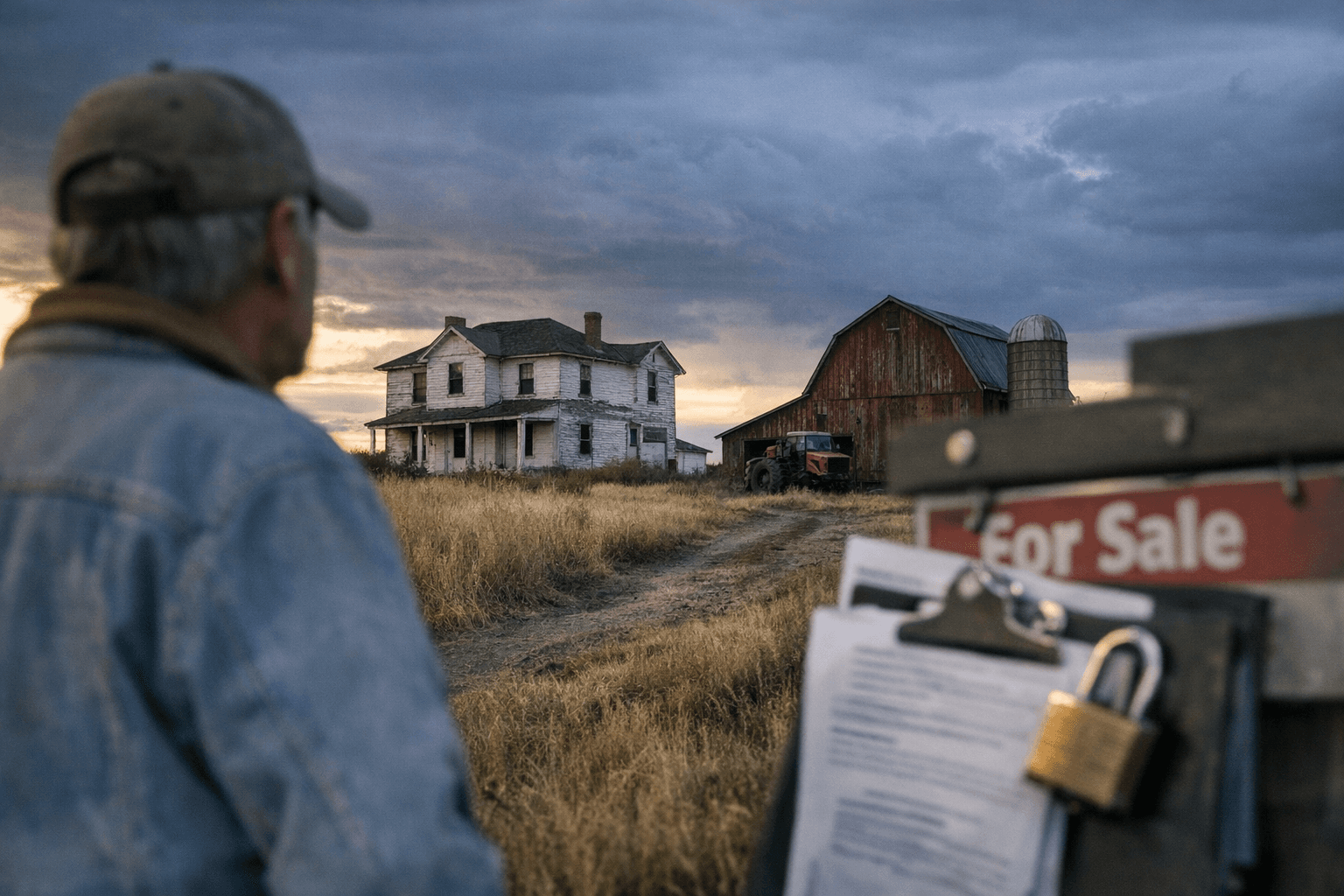

Logan County foreclosure notices show homes, farms in process

Seven Logan County properties were in foreclosure on April 20, including five in Sterling and two on the county’s rural edges. Some sales had already been continued, giving owners more time before a final sale.

Seven Logan County properties were moving through the foreclosure pipeline on the April 20 public trustee notice, and five of them were clustered in Sterling. The list also included a home on County Road 76 near Peetz and a property in Atwood, showing that the stress was not limited to town addresses.

The Sterling entries were spread across Beattie Street, Elm Street, Park Street, State Street and South Tenth Avenue. That pattern makes the notice more than a stack of paperwork: it points to pressure touching both neighborhoods and the county’s surrounding rural housing stock, where residential and agricultural loans can both wind up in the same public process.

A foreclosure notice does not mean a homeowner has already lost a property. It shows where a loan stands in the formal process, along with the grantor, beneficiary, original principal amount and, in some cases, a continued sale date. Those continuances matter because they can give borrowers more time to work with lenders, cure a default or otherwise avoid a completed sale. Colorado law also allows cure deadlines to be extended when a sale is continued.

Logan County’s public trustee is the county treasurer, and the office posts sale information publicly and can provide it directly. The county’s online document index is updated daily, though it may contain omissions or corrections, so the April 20 notice should be read as a snapshot rather than a final accounting.

The broader numbers help explain why a handful of filings can reverberate locally. Logan County had an estimated population of 20,755 and 8,815 housing units, with an owner-occupied housing rate of 68.3 percent. Median owner-occupied home value was $228,100, median monthly owner costs with a mortgage were $1,462, and median household income was $55,074.

That combination of relatively modest incomes and mortgage costs means even a small foreclosure list can affect neighbors, lenders, tax collections and future buyers. Borrowers who think a lender or servicer violated single-point-of-contact or dual-tracking rules can file complaints with the Colorado Attorney General or the Consumer Financial Protection Bureau, though that does not stop the foreclosure process. The April 20 notice fits a pattern seen repeatedly in 2024 and 2025, with filings continuing to surface in Sterling and the county’s outlying communities.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?