3 ways to boost savings with 4% accounts this month

The best 4% account is the one that fits your timeline. Emergency savers need access, while rate-chasers can trade liquidity for a fixed yield.

Best for emergency savers: high-yield savings accounts

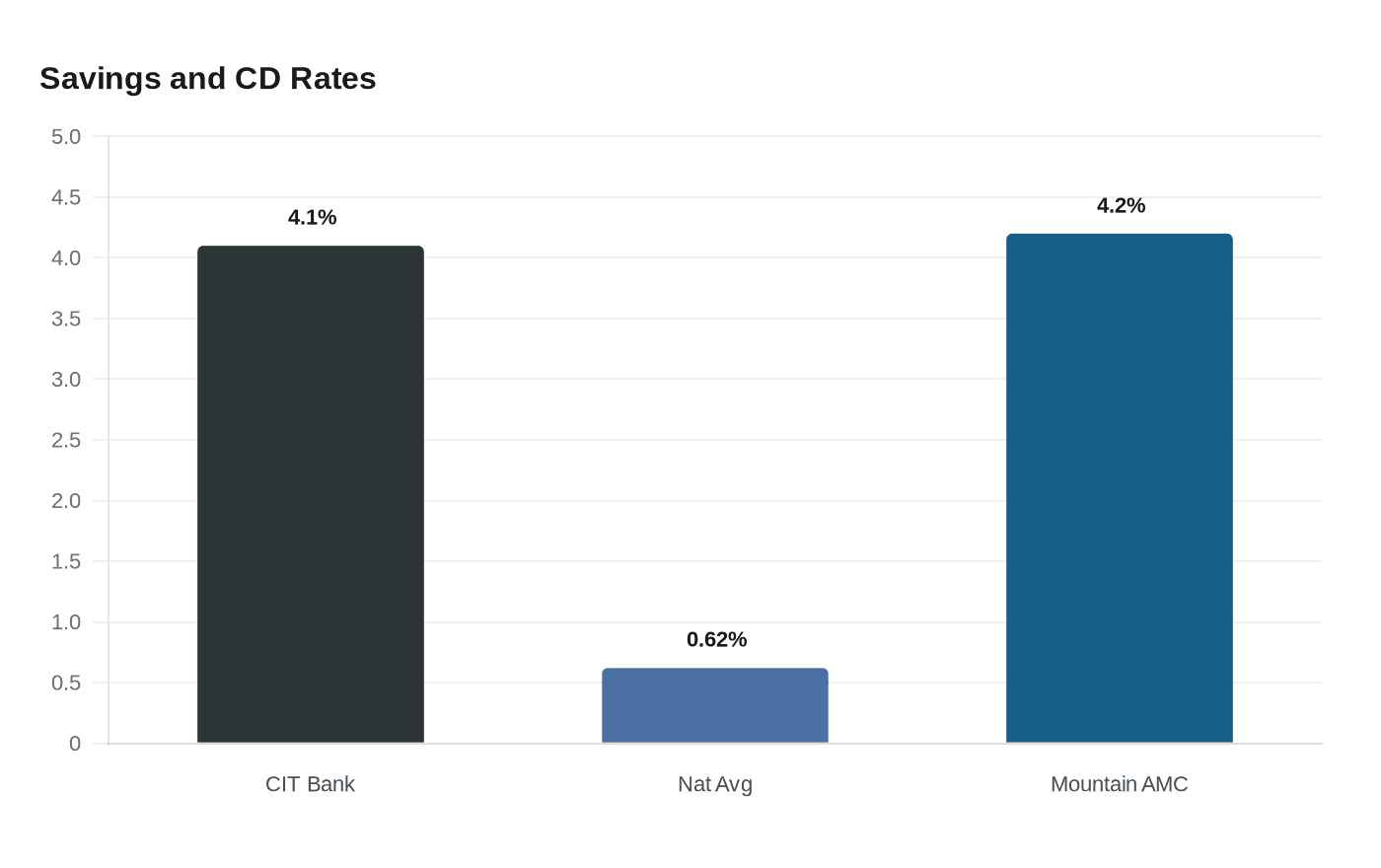

If the money is your safety net, accessibility beats squeezing out the last basis point. Bankrate’s top high-yield savings rate for June 2026 is 4.10% APY from CIT Bank, roughly six times the 0.62% national average, and CNBC Select says the best returns it is seeing are around 4% APY. That spread is large enough to matter, especially when you are parking cash that still needs to be there tomorrow morning.

High-yield savings accounts are the most flexible of the three options because you are not committing the money to a fixed term. That liquidity is what makes them useful for emergency funds and short-term reserves, and it is why these accounts remain the default choice for people who want a stronger return without losing access. Bankrate notes that top high-yield savings accounts often do not charge fees and typically require only low minimum deposits, which lowers the barrier to getting started.

The catch is that the headline APY is not the whole story. Many top accounts in the market can still carry balance caps, direct-deposit rules, or other activity requirements, so the real return can depend on how you use the account and how much cash you keep in it. On a $10,000 balance, 4.10% APY works out to about $410 a year before taxes, compared with about $62 at the national average. That gap is the reason 4% accounts still deserve attention, even in a cooling rate environment.

Best for short-term cash holders: a 4% savings account with few strings attached

For money you expect to need soon, the right move is usually not just finding the highest APY. It is finding the account that keeps the cash usable while still paying close to 4%. CNBC Select says the best returns it is seeing on high-yield savings accounts are around 4% APY, which means this is still a strong place to park cash that is not locked up elsewhere. The point is not to chase a headline; it is to preserve options.

That is where the practical tradeoffs matter most. Accounts with fees, minimum balance hurdles, or caps on the amount that earns the best rate can shave down the benefit quickly, especially if your balance is uneven or larger than the cap. Some savers will be better off with a slightly lower advertised rate if the account is simpler to hold and easier to use every day. In other words, the highest rate is not always the best fit for every saver.

The after-tax picture reinforces that point. Interest is taxable, so the gap between a 4% account and a 0.62% account shrinks once taxes are factored in, but it does not disappear. What matters is the net return you actually keep after account rules, fees, and taxes. For short-term cash, the winning account is usually the one that pays well, stays liquid, and does not force you into hoops just to earn the rate you were promised.

Best for rate-chasers: CDs that lock in today’s yield

If your goal is to lock in a yield and you can leave the money alone, a CD makes more sense than a savings account. Bankrate’s top CD rate for June 2026 is 4.20% APY from Mountain America Credit Union, and CNBC Select describes CDs as savings vehicles that pay a fixed rate over a set term. That fixed-rate structure is the appeal: you give up flexibility, but you gain certainty.

This is the strongest option for cash you know will not be needed until a specific date. If savings rates drift lower over the term, a CD preserves the rate you opened with. If rates rise later, you will not benefit from the upside, which is the tradeoff for locking in today’s yield. That makes CDs especially attractive for rate-chasers who care more about guaranteed income than daily access.

The market backdrop also matters. Bankrate says the best CD and savings rates it is tracking are typically found at online banks or credit unions rather than traditional brick-and-mortar banks, so the highest yields are often outside the branch network most people use for checking. For savers willing to move money, that can be the easiest way to capture a 4% plus return without taking equity-market risk. The best 4% account is the one that matches your timeline: keep emergency money liquid, use a high-yield savings account for near-term cash, and use a CD when the rate matters more than immediate access.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?