$50,000 earns more in a short-term CD than a money market account

A $50,000 saver can squeeze out more income in a short-term CD, but the advantage is small unless you can live without easy access to the cash.

The yield edge is real, but it is not huge

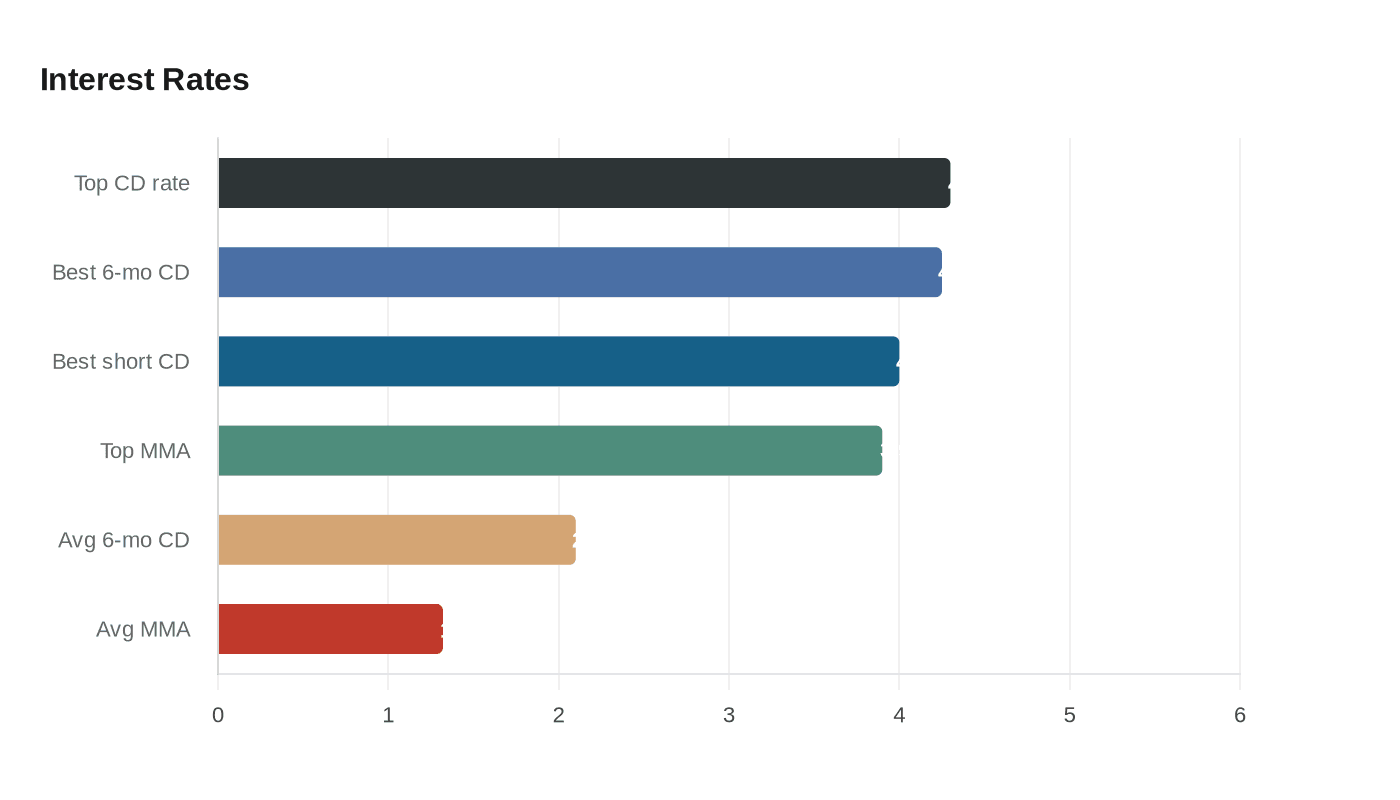

A $50,000 balance earns more in a short-term CD than in a money market account right now, but the size of the advantage is modest enough that flexibility still matters. The best short-term CD rates are hovering around 4% APY, while the top money market accounts are closer to 3.90% APY.

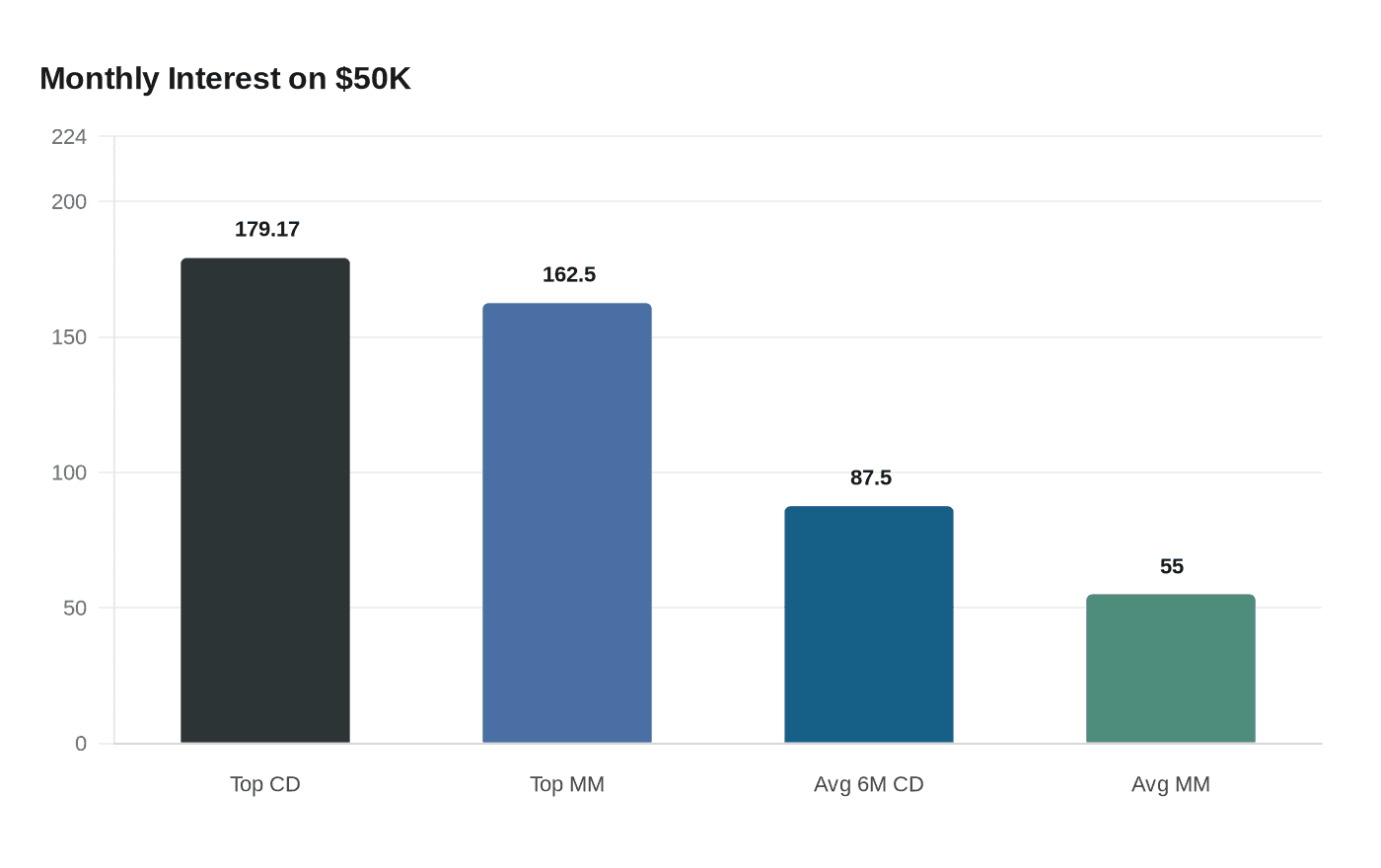

That spread looks small on paper, yet it adds up in real dollars. At 4.30% APY, $50,000 generates about $179.17 in monthly interest. At 3.90% APY, the same balance earns about $162.50 a month, a difference of roughly $16.67 each month.

What the top rates are telling savers

Bankrate’s June 2026 tracking puts the top CD rate at 4.30% APY from First National Bank of America, and its broader view of the market says the best CD rates are still around 4% APY, with the highest yields on short-term CDs. NerdWallet’s June 2026 roundup shows the best 6-month CDs at up to 4.25% APY, while its money market list shows top APYs up to 3.90%.

That pattern matters because it shows where banks are competing hardest. Short-term CDs are still the place where institutions are willing to pay up for locked-in deposits, while money market accounts tend to price a bit lower in exchange for easier access to your cash.

Why the national averages look much lower

The gap becomes even more obvious when you look at FDIC national rate data. As of May 18, 2026, the average 6-month CD rate was 2.10%, and the average money market rate was 1.32%. On a $50,000 balance, that works out to about $87.50 a month in a 6-month CD and about $55.00 a month in a money market account.

Those averages are useful because they show how far the market sits below the best promotional offers. The FDIC says its national averages are based on the $10,000 and $100,000 product tiers, so they are a broad market benchmark rather than a tailored quote for a specific saver. For anyone with $50,000, the headline rate is only part of the story, but the spread between top offers and national averages is still large enough to shape the decision.

Liquidity is the tradeoff that changes the math

This is where the choice stops being about yield alone. Money market accounts generally give you easier access to funds, which makes them better if you may need part of the $50,000 for an emergency, a tax bill, tuition, or a home repair within the next few months. CDs, by contrast, pay a fixed rate in exchange for locking money up for a set term.

That lockup can be worthwhile if you are confident the cash can sit untouched. It can also be costly if you have to break the CD early, because withdrawal penalties can erase some or all of the extra interest. The higher the rate gap and the longer the money stays deposited, the more sense a CD makes.

The break-even point for a $50,000 saver

The cleanest way to compare the two options is to look at the yield difference over your likely holding period. At the top tracked rates, the CD pays about $16.67 more per month than the money market account on a $50,000 balance, which is about $100 over six months and about $200 over a full year.

That gives you a simple break-even test:

- If you may need the money in the next few months, the extra yield may not justify giving up liquidity.

- If you can leave the money alone through a 6-month term, the CD’s higher rate becomes more meaningful.

- If an early-withdrawal penalty would wipe out more than about a month or two of extra interest, the money market account may be the safer choice.

A practical reading of the numbers says this: the CD’s advantage is real, but it is not large enough to ignore access to cash. A saver who values flexibility highly may accept a slightly lower rate to avoid penalties or forced timing.

How rate-change risk tilts the decision

The Federal Reserve still uses interest-rate policy as a major monetary tool, and deposit rates remain sensitive to those settings. That makes rate risk a central part of the decision. A CD locks in today’s rate, which helps if deposit yields drift lower over the next several months. A money market account can move more easily as banks adjust to policy shifts, which means your yield can fall if the rate environment softens.

That protection is one reason short-term CDs are attractive now. If you think the next Fed move could pressure deposit rates lower, fixing a 4% plus yield for a short term has value beyond the headline APY. If you expect to need the money soon, though, the ability to move quickly can matter more than the possibility of locking a rate.

Who each option suits over the next 3 to 12 months

If your time frame is short, the money market account usually wins on convenience. It is the cleaner choice for cash you may need within 3 months, especially when the rate difference is only a few tenths of a percentage point.

If you can commit for 6 months, a short-term CD starts to look more attractive. NerdWallet’s best 6-month CD list shows rates up to 4.25% APY, which is above the best money market rate it tracked at 3.90%, and the FDIC averages show the broader market still pays much less than those top offers. That combination makes a 6-month CD appealing for money that can sit still through the term.

If your horizon is closer to 12 months, the choice depends on whether you want certainty or access. A CD gives you a fixed return and shields you from rate declines, while a money market account keeps your cash available and leaves you free to move quickly if something changes. For a saver holding $50,000, the right answer is not about squeezing every last basis point; it is about deciding whether the extra roughly $200 a year at the top rates is worth giving up flexibility.

The bottom line

For $50,000, the best short-term CD does pay more than the best money market account, but the gap is narrow enough that liquidity still deserves equal weight. If you can truly leave the money alone, the CD’s fixed rate is a sensible way to lock in income. If you may need the funds, the money market account’s easier access can be worth more than the extra yield.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?