$90,000 CD deposits still qualify for federal insurance, can earn 4% APY

A $90,000 CD is still federally protected and can earn about $3,600 a year at 4% APY, but taxes, inflation and penalties can shrink the real payoff.

A $90,000 CD still sits comfortably inside federal insurance limits

A $90,000 certificate of deposit is large enough to deserve a second look, but not too large to fall outside standard federal protection. The Federal Deposit Insurance Corporation covers deposits up to at least $250,000 per depositor, per insured bank, per ownership category, and that insurance applies dollar-for-dollar to principal plus any interest accrued or due through the date of default.

That matters because a $90,000 CD balance is generally well within the limit if it is held in a single ownership category at one FDIC-insured bank. In plain terms, the deposit itself is not the risk. The bigger question is whether the return justifies giving up liquidity for months or years.

What 4% APY means in real dollars

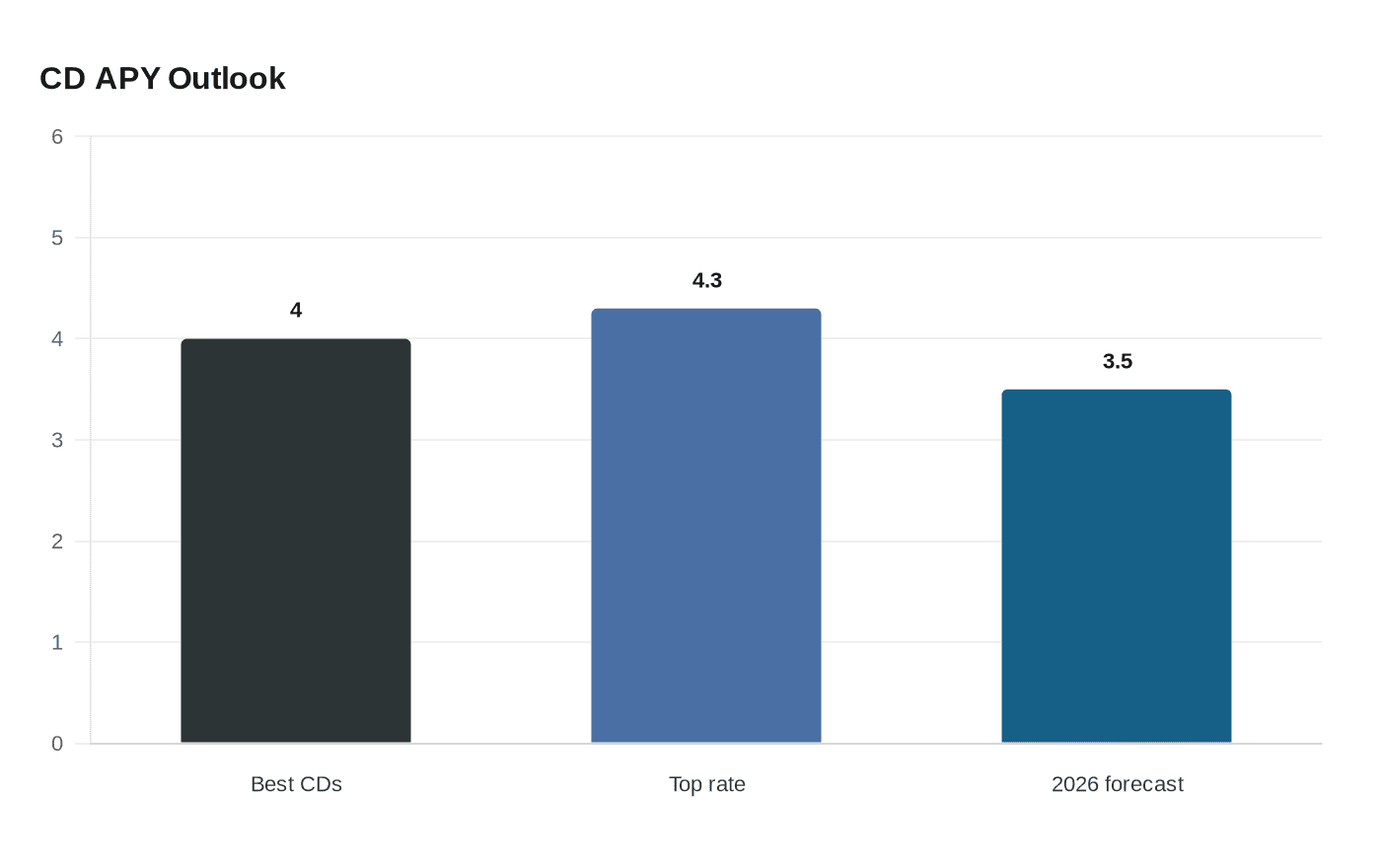

At about 4% APY, a $90,000 CD would earn roughly $3,600 over a year before taxes, assuming the money stays deposited for the full term and the rate is sustained for that period. Bankrate says the best nationally available CD rates in May 2026 are around 4% APY, with its top tracked rate at 4.30% from First National Bank of America.

That difference can be meaningful, but not life-changing. At 4.30% APY, the annual interest on $90,000 comes to about $3,870 before taxes. In a low-risk savings product, the appeal is less about outsized gains and more about locking in a known return when cash yields are still respectable.

The catch: early withdrawals can turn a good rate into a costly mistake

A CD is a type of savings account that typically requires you to keep money deposited for a fixed term. If you pull funds out early, the bank usually charges a penalty fee, which can reduce or even wipe out the interest you expected to earn.

That penalty is what makes the product different from a high-yield savings account. With a savings account, your balance remains liquid. With a CD, you are trading flexibility for rate certainty, and the cost of that trade can be steep if cash needs come up unexpectedly.

Taxes and inflation change the answer

The headline APY is not the same as your spendable return. CD interest is taxable, so the amount you keep after federal and state taxes will be lower than the advertised yield, and the size of that haircut depends on your tax bracket and where you live.

Inflation matters just as much. If prices rise faster than the CD’s after-tax yield, the purchasing power of the money falls even though the account balance grows. That is why a CD can look solid on paper while still losing ground in real terms, especially if the rate drops over the course of a longer term.

Why the rate outlook argues for acting with care

Bankrate’s 2026 forecast says the highest one-year CD APY could be about 3.5%, suggesting yields may drift lower as the year goes on. Ted Rossman, Bankrate’s senior industry analyst, has said the highest rate for one-year CDs will be 3.5% APY.

That outlook raises a timing question for savers: locking in a rate now may protect you if yields slide, but waiting could mean accepting a lower return later. For a $90,000 deposit, even a few tenths of a percentage point matter. The difference between 3.5% and 4.0% is about $450 a year on principal of this size, before taxes.

How the FDIC views rates and why some banks are constrained

The FDIC’s national-rate framework uses a weighted average of rates paid by insured depository institutions and credit unions. That framework is part of a broader set of interest-rate restrictions that can limit less-than-well-capitalized banks from offering rates that significantly exceed prevailing market levels.

For savers, that means the best headline rate is not always available everywhere, and not every institution can chase the same pricing. A bank’s capital condition can affect what it is allowed to offer, which is one reason the market for CDs can vary even when the product itself seems simple.

When a CD beats a high-yield savings account, Treasuries, or cash

A CD tends to make the most sense when you know you will not need the money for the full term and you want a guaranteed return. If the goal is to park a specific sum for a known period, especially when rates are near 4% APY, the certainty can be valuable.

A high-yield savings account fits better when flexibility matters. Treasury bills and other short-term government securities can compete on yield and may offer different tax treatment, while cash left completely liquid gives up return but preserves full access. For a $90,000 balance, the right choice depends on three questions: how long the money can stay put, how much rate certainty matters, and how much liquidity you are willing to sacrifice.

The bottom line for a six-figure saver with a five-figure CD

A $90,000 CD is still well protected under FDIC rules, and at current best-in-market rates it can produce a meaningful stream of interest. But the true return is smaller after taxes, smaller again after inflation, and potentially much smaller if an early withdrawal penalty is triggered.

That is why the real decision is not whether a CD is safe. It is whether locking away $90,000 for a set term beats keeping the money liquid, buying a Treasury with similar yield, or waiting for better rates later. In today’s market, the answer depends less on the headline APY than on how much flexibility the saver can afford to give up.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip