A $20,000 two-year CD could deliver strong returns now

A $20,000 two-year CD can outpace average savings rates, but taxes, inflation and early-withdrawal risk trim the real gain.

A $20,000 two-year CD looks compelling right now, but the real story is less about the headline rate than the gap between average and best-in-class offers. The Federal Reserve kept its target range at 3.50% to 3.75% on April 29, 2026, the FDIC’s May 2026 average for a 24-month CD under $100,000 was 1.50%, and top online two-year deals were running around 4% to 4.25% APY, with Forbes Advisor noting that the best two-year CDs can pay roughly 10 times what the average financial institution pays.

How a two-year CD works

A certificate of deposit is a savings account offered by banks and credit unions that requires you to keep your money deposited for a specified length of time. The CFPB says withdrawing money early usually means paying a penalty fee, which is the main tradeoff for locking in a fixed return. CDs are still widely viewed as low-risk because deposit insurance generally covers up to $250,000 per depositor, per insured institution, and the FDIC’s rate-cap framework helps explain why some institutions can advertise rates well above the national average.

The FDIC’s national-rate cap for a 24-month CD is calculated as the higher of the national rate plus 75 basis points or 120% of the current Treasury yield plus 75 basis points. That matters because the national average can stay muted even when aggressive online banks and credit unions are paying much more. In practice, the current market is giving savers a wide spread to shop, not a single uniform rate.

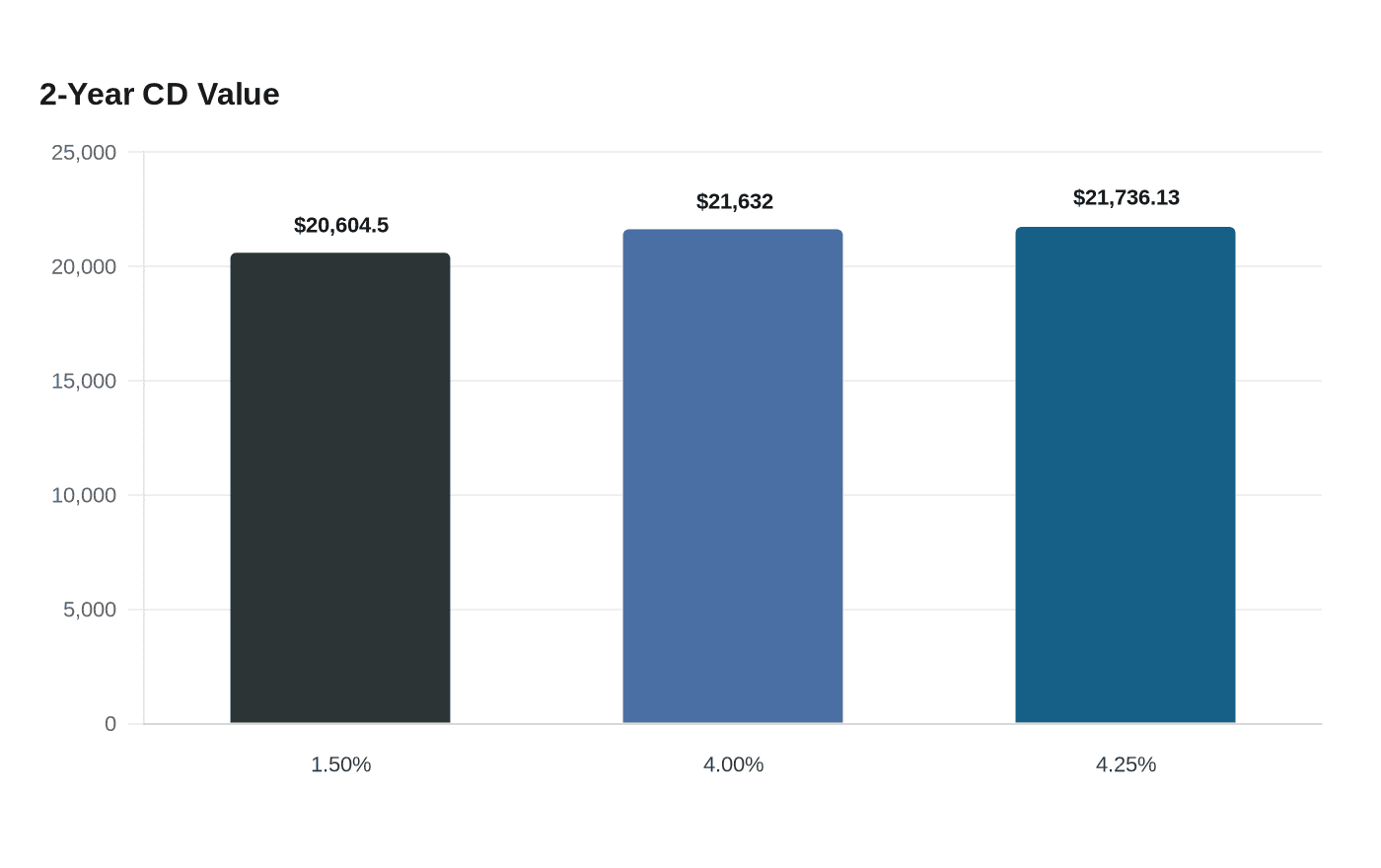

What $20,000 actually earns

At 4.25% APY, a $20,000 CD grows to $21,736.13 over two years, or $1,736.13 in interest. By contrast, at the FDIC’s 1.50% national average for a 24-month CD, the same deposit would end at $20,604.50, for $604.50 in interest. That means a strong online offer can deliver about $1,131.63 more before taxes. Even at 4.00% APY, the ending balance would still reach $21,632.00.

That difference is why shopping around matters. Bankrate’s June 2026 roundup says the best CD rates are still around 4% APY, with the top tracked rate at 4.25%, and its two-year guide specifically tells savers to compare offers because the best rates pay far more than the national average.

Taxes and inflation trim the headline yield

The gross return is not the same as the money you keep. The IRS says most interest is taxable in the year it becomes available to you, so your after-tax return depends on your marginal rate. That means the $1,736.13 of interest from a 4.25% APY CD gets smaller as soon as tax comes into the picture.

Inflation is the second quiet drag. The Bureau of Economic Analysis said the personal consumption expenditures price index rose 3.5% year over year in March 2026, while core PCE was up 3.2%, and the Fed still aims for 2% inflation over the longer run. If inflation stayed at 3.5% a year, a 4.25% APY CD would leave about $20,290.91 in inflation-adjusted value after two years, which is only about $290.91 above principal in today’s dollars before taxes.

That is the key consumer lesson: a CD can produce a positive real return, but not a huge one once price growth and taxes are folded in. The advertised APY is the starting point, not the finish line.

Who this makes sense for now

A two-year CD makes the most sense if you already know the money will not be needed for the full term. Bankrate says CDs are best for people who want a guaranteed return that is typically higher than a savings account, while savings accounts and money market accounts fit shorter-term goals better. If you are parking cash from a bonus, inheritance, tax refund or another balance you can truly leave untouched, the CD can do its job well.

It also fits savers who want to reduce decision-making. A fixed-rate CD removes the temptation to move money around chasing the next headline yield, and it gives you certainty in a rate environment that is still elevated relative to recent years. For a cash bucket that already has a purpose and a date, certainty has value.

Who should stay more liquid

If there is any meaningful chance you will need the money early, a CD is the wrong place to put it. The penalty for breaking the term can wipe out part of the interest, and that risk is especially painful when the balance is supposed to serve as a backup fund or near-term spending money. Bankrate points savers toward checking accounts for everyday access and savings or money market accounts for shorter-term goals, which is the better fit for emergency funds, home down payments and other cash that may have to move quickly.

Historical context also keeps expectations grounded. Bankrate’s historical review says three-month CDs paid about 18.3% APY in early May 1981, a reminder that the double-digit CD era was tied to a very different inflation backdrop. Today’s 4%-class offers are strong by recent standards, but they are not a return to that world.

The bottom line is straightforward: a $20,000 two-year CD can still be a strong parking place for money you do not need, especially if you can lock in a rate near 4% to 4.25% APY. But once taxes, inflation and the cost of losing liquidity are counted, the product works best as a precision tool for idle cash, not as a replacement for money that needs to stay flexible.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?