AI boom pushes U.S. stocks to records as market concentration deepens

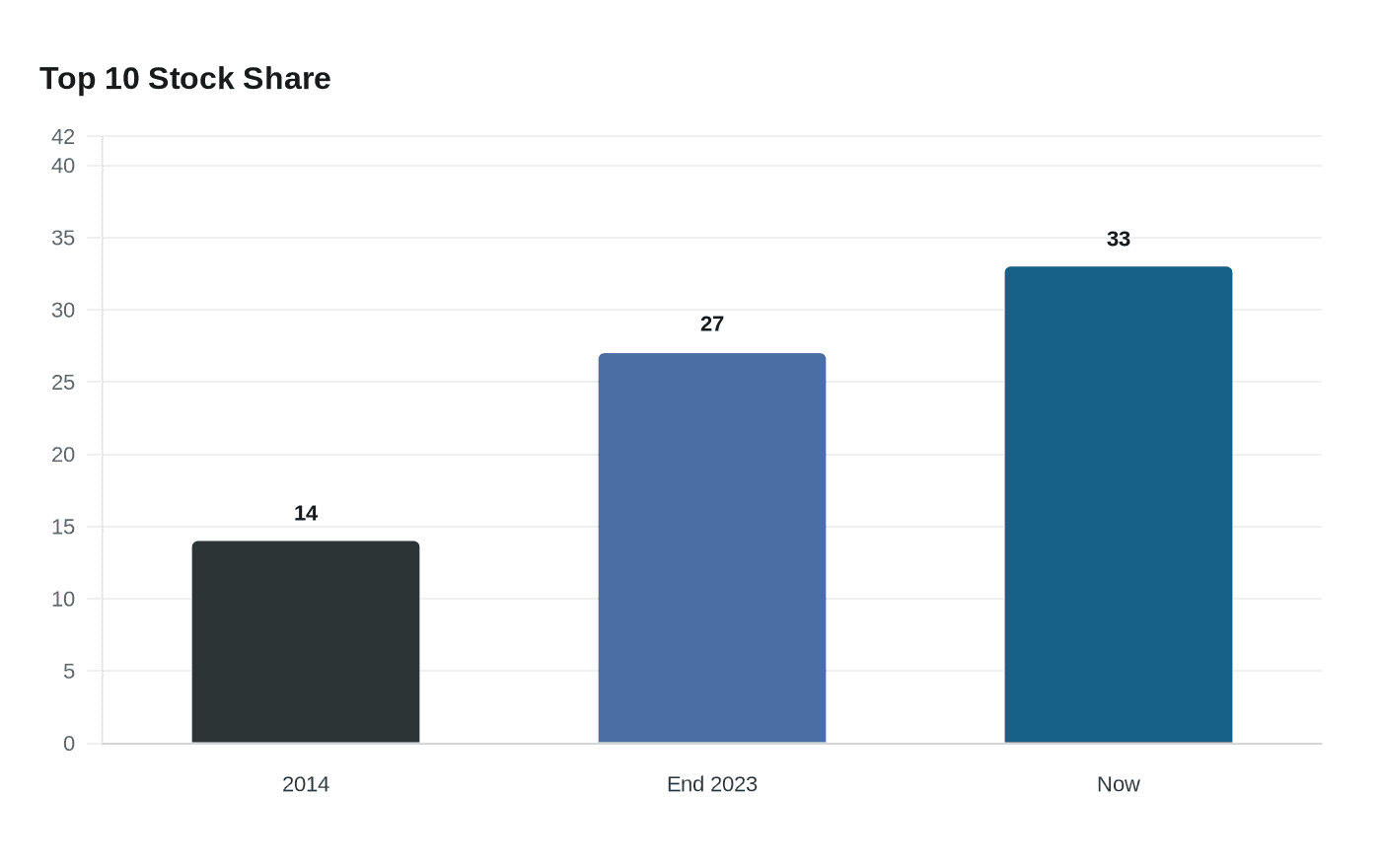

Record highs in the S&P 500 and Nasdaq mask a narrower advance, with the top 10 U.S. stocks now carrying 33% of market value.

AI enthusiasm has pushed U.S. stocks to record highs, but the deeper story is how much of the rally now depends on a shrinking group of giants. The S&P 500 closed at a record on Friday, even above the peaks of the internet bubble, while the Nasdaq also hit fresh highs as Nvidia and other technology stocks extended gains on the back of stronger April U.S. jobs data and expectations that the Federal Reserve will stay steady.

That strength, however, has come with a sharp rise in concentration. Morgan Stanley figures cited by Reuters show the top 10 U.S. stocks now make up 33% of total market value and 37.5% of the MSCI USA Index, a reminder that index gains can look broad even when they are being driven by a very small number of names. Morgan Stanley said in a June 4, 2024 report that the top 10 U.S. stocks had already climbed from 14% of total market capitalization in 2014 to 27% at the end of 2023.

The scale of that dependence became clear in 2023, when Morgan Stanley said the appreciation of the Magnificent Seven accounted for more than half of the S&P 500’s 26.3% gain. Reuters also noted that Goldman Sachs analysts said the top tech stocks accounted for 53% of the S&P 500’s returns last year, while LSEG estimates show about two-thirds of the projected $150 billion increase in first-quarter earnings this year is expected to come from technology and communications services. In other words, the market’s headline strength is now tightly linked to the earnings power of a few dominant companies.

That is not necessarily a flaw, market strategists argue, but it is a structural risk. J.P. Morgan Research said in February 2024 that the rise in U.S. stock concentration was the steepest in 60 years. Historically, periods of rising concentration since 1950 have tended to produce stronger annualized U.S. equity returns than periods when concentration was falling, Morgan Stanley said, suggesting investors have often been rewarded for staying with the winners even as the market narrows.

The pattern is visible beyond Wall Street. Lazard Asset Management said on March 3, 2026, that TSMC alone made up 12.5% of a passive emerging-markets portfolio benchmarked to the MSCI Emerging Markets Index, and that the top 10 holdings accounted for 32.4% of the index as of January 31, 2026. MSCI says that benchmark covers about 85% of each country’s free-float-adjusted market capitalization. Samsung makes up about 20% of South Korea’s benchmark index, while TSMC is about 40% of Taiwan’s.

The question for investors is no longer whether concentration exists. It is how much exposure to accept to keep riding the AI boom, and how much downside to bear if leadership cracks. With the market leaning harder on a handful of mega-caps, the next setback in the rally could be far less diversified than the last one.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?