AI, Defense and Electrification Could Push Copper Demand 50% by 2040

A new S&P Global study projects global copper demand will rise about 50% by 2040, creating a potential annual shortfall of roughly 10 million tonnes unless mining and recycling expand substantially. The finding raises urgent questions for policymakers and investors about permitting, financing and recycling capacity as electrification, data-center growth and defense modernization drive metals demand.

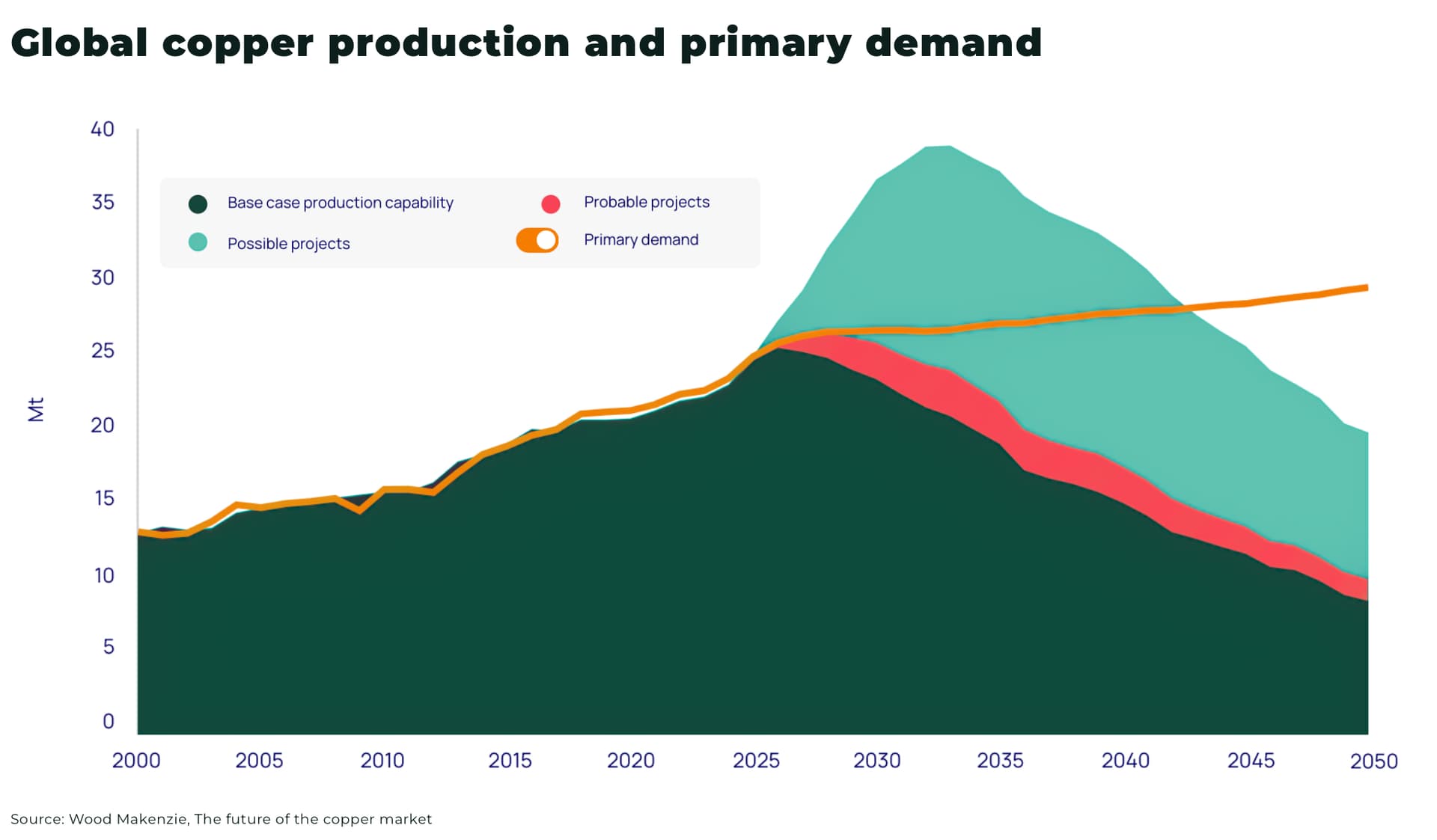

S&P Global released a consultancy study on Jan. 8, 2026, projecting that annual global copper demand will climb from about 28 million metric tons in 2025 to roughly 42 million metric tons by 2040. The central forecast points to a structural gap on the order of about 10 million tonnes per year by 2040 unless mining output and secondary supply rise materially.

The study identifies the ongoing global shift toward electrification as the primary long-term driver. Dan Yergin, S&P vice chairman and an author of the report, described copper as "the metal of electrification." Beyond electric vehicles, renewable generation and grid expansion, S&P highlights two emergent demand vectors that intensify the outlook: artificial intelligence infrastructure and defense modernization. Combined, S&P estimates that AI-related data centers and increased defense spending could add roughly 4 million tonnes of copper consumption per year by 2040.

S&P documents a recent surge in data-center investment as an indicator of this trend, noting more than 100 new data-center projects were launched in the prior year, with combined capital commitments just under $61 billion. The firm projects installed data-center capacity could grow nearly fourfold by 2040 under central scenarios, intensifying demand for copper wiring, cooling systems and power distribution.

On the defense front, S&P vice president Carlos Pascual, a former U.S. ambassador to Ukraine, underscored the inflexibility of military demand, calling it "really inelastic." Rising defense budgets in multiple regions tied to geopolitical tensions are expected to require durable supplies of copper for modern weaponry, communications and power systems.

Supply-side dynamics compound the risk of shortages. S&P expects global mined copper production to peak near 33 million tonnes in 2030, constrained by declining ore grades and persistent hurdles in permitting, financing and construction of large projects. Recycling will expand, the study projects, more than doubling to roughly 10 million tonnes per year by 2040, but even that increase leaves a large residual deficit.

The analysis excludes potential supply from deep-sea mining and treats some demand scenarios as explicitly hypothetical. One illustrative example flags humanoid robots as an early-stage risk: if 1 billion such machines were operating by 2040, S&P estimates they would demand about 1.6 million tonnes of copper per year, or roughly 6 percent of current global consumption.

Regionally, Asia is expected to supply about 60 percent of incremental demand through 2040, while North America, Europe and the Middle East each show notable increases tied to digitalization and clean-energy build-out. For markets and policymakers, the implications are immediate. A multi-decade structural shortfall would likely put upward pressure on copper prices, incentivize new exploration and recycling investment, and intensify calls for faster permitting and financing mechanisms.

Closing a roughly 10-million-tonne annual gap will require coordinated action from mining companies, recyclers and governments. Without that, S&P warns that copper could become a bottleneck for the technologies central to decarbonization, AI deployment and defense modernization.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?