AML3D Holds A$16.5M Orders, Low A$3.25M Revenue; H2 Could Be Record

AML3D holds A$16.5 million of orders in hand while recognising only A$3.25 million of revenue in H1; the company says material delays pushed much of the income into H2 FY26.

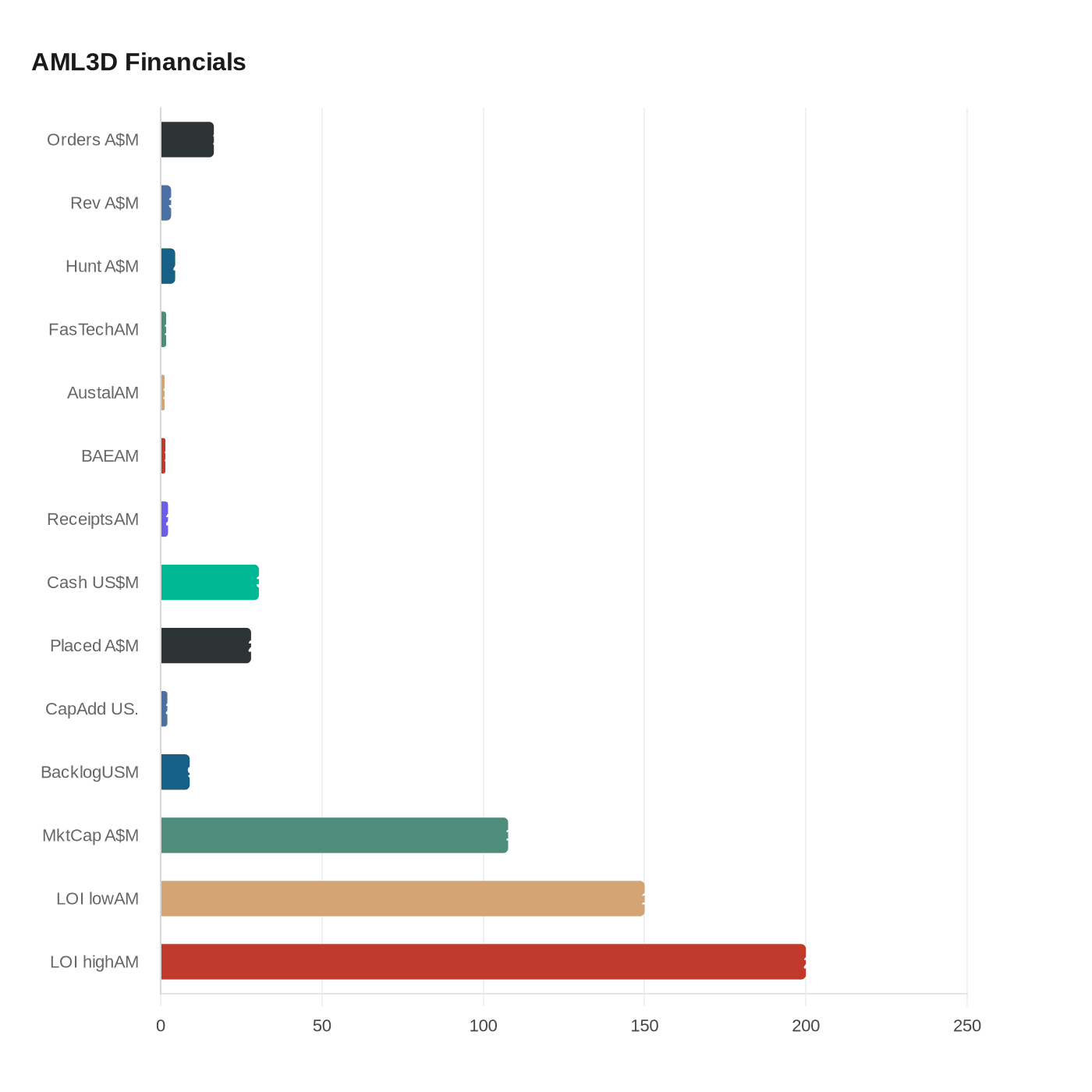

AML3D reported approximately A$16.5 million in orders in hand for the half-year ending December 31, 2025, while recognising just A$3.25 million of revenue in the period, and said the timing shifts could make the second half of FY26 a record. The company attributed the lower first-half revenue - roughly a 30% decline versus the prior corresponding period - to raw material delays and extensions to project timelines that pushed revenue into H2 rather than cancelling work.

Named contracts underpinning the A$16.5 million ledger include a A$4.5 million sale of two custom ARCEMY X systems to Huntington Ingalls Industries’ Newport News Shipbuilding division, a roughly A$1.69–A$1.7 million ARCEMY X order from FasTech LLC, a A$1.2 million portable ARCEMY Small for Austal USA, and an approximately A$1.47 million alloy/material feasibility program with BAE Systems UK. The order mix keeps AML3D firmly in defence, shipbuilding and industrial markets while expanding into utilities and European channels.

The FasTech order carries detailed delivery steps: AML3D will supply the FasTech ARCEMY X from its U.S. Technology Centre in Stow, Ohio, and to expedite delivery will transfer a 6,000 pound (about 2.7 tonne) positioner from systems already operating at Stow, then replace it with a new ARCEMY X to maintain production capacity at the centre. The FasTech unit is expected to be installed and operational during Q3 of FY26 and will be the ninth ARCEMY system installed in the U.S. The company press release includes the line fragment "AML3D CEO Sean Ebert said: [...]" as supplied in the announcement.

AML3D said approximately 87% of first-half revenue came from U.S. customers, and it highlighted new contracts in the U.S. utilities sector alongside continued U.S. Navy work. The company has been leveraging a U.S. Department of the Navy Letter of Intent that TipRanks and other summaries flag as identifying an estimated A$150-A$200 million additive manufacturing opportunity through 2030; management reporting also framed the LOI as projecting demand for 100 systems and up to 1,600 components by 2030.

On cash and receipts, customer receipts rose 360% year-on-year to A$2.3 million in the December 2025 quarter, while year-end cash reserves were reported at US$30.40 million following a A$28.03 million placement in December 2024 and capital additions of US$2.09 million to support R&D and U.S. expansion. Orders in backlog have been reported as exceeding US$9 million for FY26 delivery in the company’s annual reporting.

Market metrics show a current market cap around A$107.7 million and TipRanks flagged a Technical Sentiment Signal of Strong Buy even as the most recent analyst rating listed was Hold with an A$0.19 price target. AML3D’s near-term outlook now hinges on delivery schedules and raw-material timing; as the company put it in external coverage, "So, what they are saying is that the orders are there, but the revenue is just coming later.

Know something we missed? Have a correction or additional information?

Submit a Tip