AppMagic: Mobile games revenue grew just 0.2% in 2025

AppMagic data shows global mobile games revenue rose just 0.2% in 2025, signalling a maturing market with tougher competition and shifting opportunities for developers and publishers.

Global mobile games revenue barely moved in 2025, rising 0.2% year-on-year as downloads grew 4.6%, down from 6.6% the prior year. The slowdown follows a stronger 2024 when revenue expanded 3.0%, and AppMagic frames the change as a market shifting from broad expansion to tighter competition.

AppMagic says the market is "[entering] a more mature and competitive phase," and highlights "rising saturation" and "exhaustion" in regions that previously drove growth. "Together, these trends point to a maturing gaming market where competition is intensifying around a relatively fixed base of users and spending, rather than broad-based market expansion." That dynamic helps explain why downloads can still climb while headline revenue stalls.

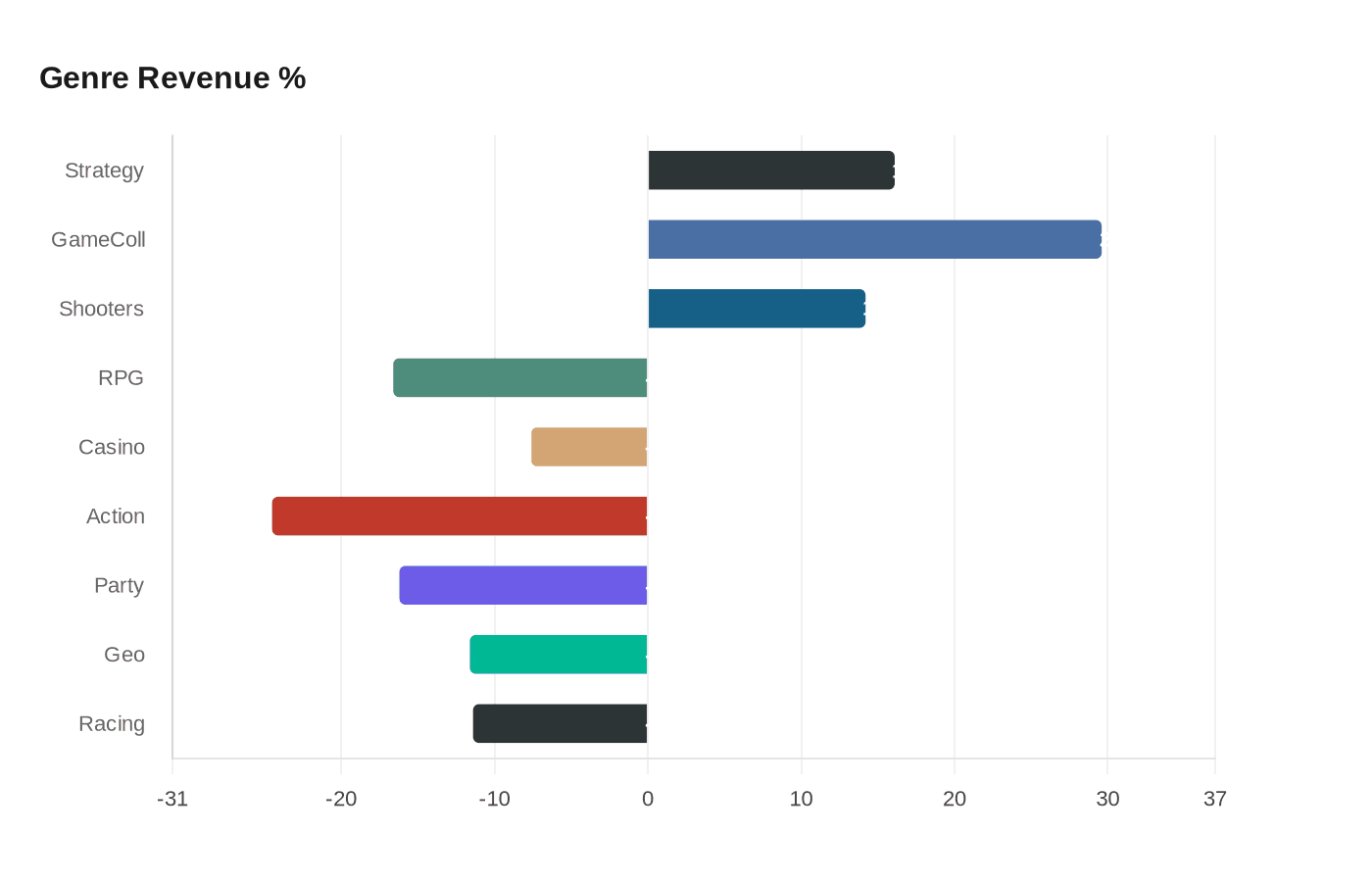

Genre-level results show a clear redistribution of opportunity. Strategy games were a bright spot, with revenue up around 16% and downloads up roughly 15% year-on-year; GameDevReports gives the strategy revenue as +16.1% for precision. Game Collection titles jumped fastest at +29.6%, while shooters grew +14.2%. By contrast, RPG revenue fell 16.6% and casino revenue fell 7.6%, with casino downloads plunging 15.8%. Action games saw the steepest revenue drop at -24.5%, and other declines included party games -16.2%, geo-based -11.6%, and racing -11.4%.

Retention and concentration are key pieces of the puzzle. AppMagic data cited by GameDevReports shows midcore retention slipping at all stages; D365 retention dropped by 12% in 2025 (again, not percentage points). In 4X strategy, an intensifying oligopoly pushed the top-10 games to 64% of subgenre revenue in 2025, up from 47% in 2023. Strong newcomers are still emerging in that space; Kingshot, launched in 2025, is cited as an example.

Regional shifts are uneven. Latin America shows steep download declines in several countries - Colombia -10.0%, Ecuador -9.8%, Peru -8.9%, Argentina -8.4% - even as Argentina and Colombia posted revenue increases of +33.2% and +23.6% respectively. AppMagic flags stagnation across the Top 10 mobile games markets, with small gains in the UK, Germany and France offsetting declines in key Asian monetisation markets such as South Korea. Country-level download changes include India +1.1%, United States +2.6%, Brazil -5.1%, Indonesia +8.0% and Russia -2.9%.

Monetisation channels complicate the headline. AppMagic’s report covers App Store and Google Play only, while its D2C and alternative payment analytics for the United States show D2C revenue rising 26% year-on-year. GameDevReports cautions: "❗️Please, note that revenue here is shown excluding D2C payments. The real picture may differ." Sensor Tower presents a different trendline, with downloads down since 2023 and revenue growing faster than AppMagic reports, underlining methodological gaps between providers.

What this means for developers and publishers is practical: prioritize retention and long-term engagement over short-term install spikes, test D2C and alternative payment strategies where legal and viable, and consider subgenre focus - strategy and game collection are where scale is moving now. Expect tougher user-acquisition economics and more consolidation in midcore subgenres; monitor adjusted revenue figures that include D2C to get the full picture.

Know something we missed? Have a correction or additional information?

Submit a Tip