AstraZeneca beats profit forecasts, keeps 2026 outlook on strong drug demand

AstraZeneca lifted first-quarter profit above forecasts as oncology and rare-disease sales surged, but the beat also underscored how much growth still depends on premium specialty drugs.

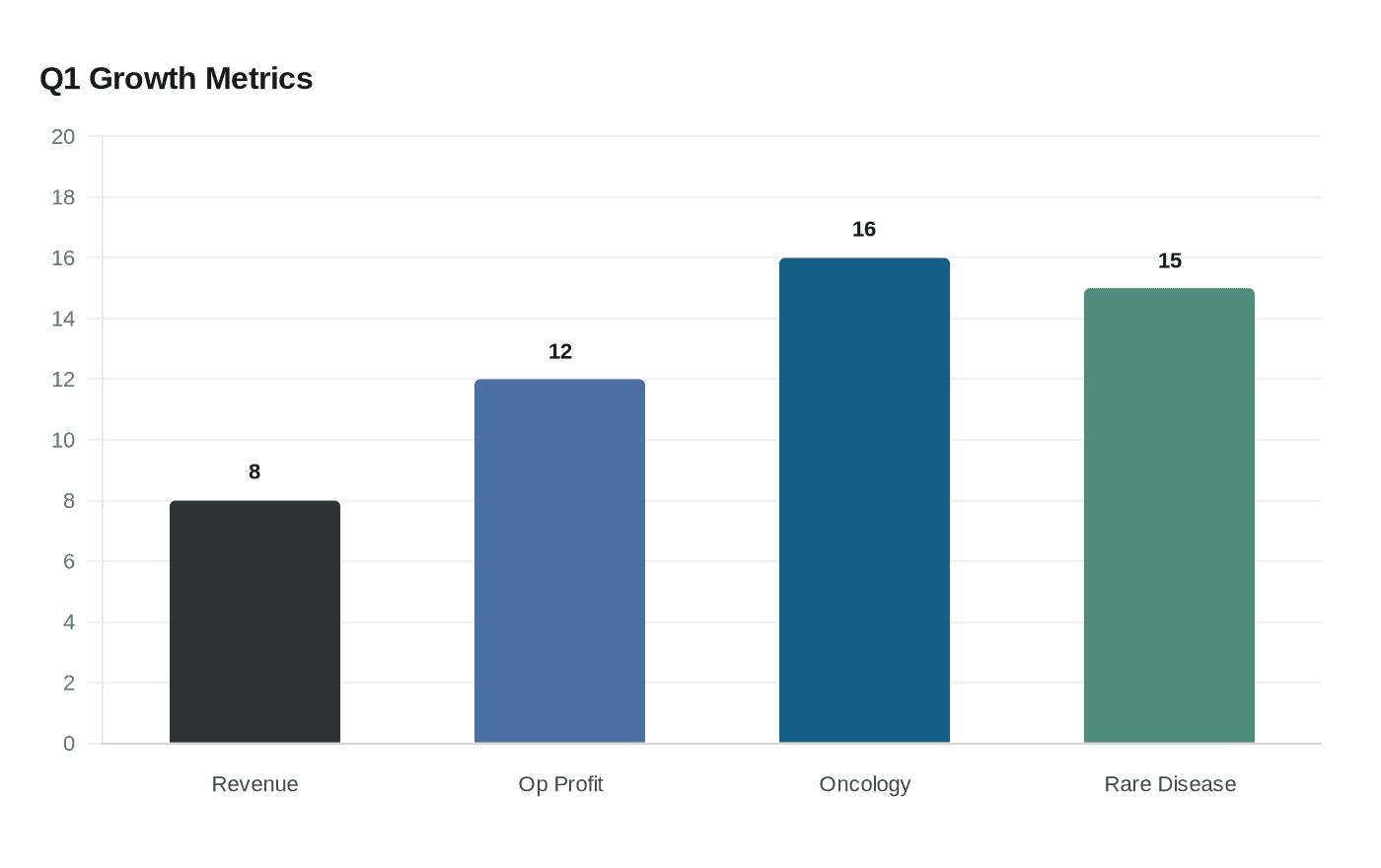

AstraZeneca’s first-quarter results showed a company running hot on specialty medicine demand, even as the broader question lingers over how much of that growth comes from innovation and how much from pricing power. The drugmaker reported revenue of $15.288 billion, up 8% at constant exchange rates, with core earnings per share of $2.58 and core operating profit up 12%. It also reaffirmed its 2026 outlook, signaling confidence that the momentum behind its cancer and rare-disease portfolio will hold.

The strongest proof was in the mix. Oncology sales rose 16% in the quarter and rare-disease sales climbed 15%, showing that AstraZeneca’s growth engine is still being driven by high-value specialty medicines rather than a broad recovery across the rest of the portfolio. Enhertu, the antibody-drug conjugate recorded alongside Daiichi Sankyo, generated combined sales of $1.422 billion in the quarter. The company said total revenue topped $15 billion and pointed to consistent commercial execution as the basis for the beat.

That performance fits the long-term strategy Pascal Soriot has been pursuing: build a pipeline and commercial footprint large enough to sustain much bigger sales later in the decade. AstraZeneca’s 2030 ambition is to launch at least 20 new medicines and reach $80 billion in annual revenue, up from $45.8 billion in 2023. The company said it remains on track for that goal and beyond, helped by a series of expected launches this year, including baxdrostat, camizestrant and gefurulimab if regulators approve them.

The company is also committing heavily to the United States and China, two markets central to both growth and policy risk. AstraZeneca has announced a $50 billion U.S. investment plan through 2030 and a separate $15 billion China investment plan in 2026. That spending reflects a broader industry calculation: to protect future growth, big drugmakers must keep building manufacturing, research and commercial scale in the markets that matter most, even as patent cliffs, pricing pressure and geopolitics threaten margins.

Pipeline progress is helping justify that reinvestment. AstraZeneca said it posted positive Phase III readouts for tozorakimab in COPD and efzimfotase alfa in hypophosphatasia, and it logged 14 approvals in major regions since its fourth-quarter 2025 results. Still, the market reaction was restrained, with Reuters reporting the shares down about 1% after the release. That suggests investors had already priced in much of the upside, even as the quarter confirmed that specialty drugs remain the clearest path to AstraZeneca’s next phase of growth.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?