Bank of Japan Raises Rates to 0.75 Percent, Highest Since 1995

The Bank of Japan unanimously raised its short term policy rate by 25 basis points to 0.75 percent at a meeting ending December 19, 2025, marking the highest level in roughly 30 years. The move signals a continuing exit from decades of ultra loose policy, with implications for wages, markets and the cost of Japan's public debt.

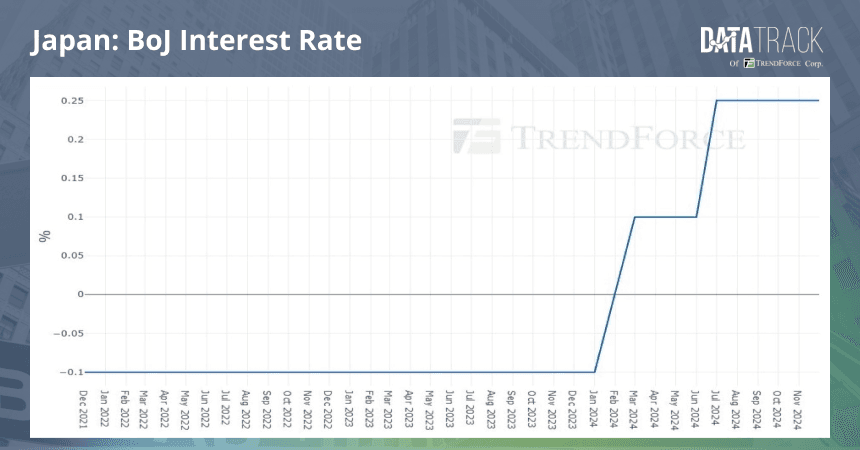

The Bank of Japan on Friday raised its key short term policy rate by 25 basis points to 0.75 percent, a unanimous decision that policymakers described as a further step away from decades of ultra loose monetary settings. The increase, announced at the close of a two day meeting that ended on December 19, 2025, is the central bank's second rate hike this year and marks the highest policy rate since September 1995.

Officials framed the decision as a calibrated move that preserves support for economic activity while responding to more persistent price pressures and stronger wage dynamics. The Bank said real interest rates are expected to remain “significantly negative” and that accommodative financial conditions will continue to firmly support economic activity. Officials highlighted recent corporate profit growth and an expectation of steady wage increases in 2026 as central inputs to their deliberations.

Market reaction was immediate. Ten year Japanese government bond yields climbed past 2 percent after the announcement, reflecting investor reassessment of future rate paths and the interplay between central bank policy and fiscal financing needs. Trading desks and economists widely viewed the hike as broadly in line with market expectations, and analysts noted that the December move follows a similar rise in January.

The policy shift carries pronounced fiscal and political consequences. Higher short term rates raise the specter of increased borrowing costs for Japan's deeply indebted public sector, a point underscored by observers and policy commentators. The government last month enacted a roughly 117 billion dollar stimulus package that includes household subsidies, higher defense spending and investments in semiconductors and shipbuilding. That fiscal expansion comes as markets and policymakers weigh the trade off between sustaining demand and containing long term debt servicing burdens.

Former BOJ policy board member Kiuchi Takahide framed the change as an orderly transition. He described the decision as part of an “exit from monetary easing, not a tightening,” and said the bank will likely need to raise the policy rate further, potentially toward around 1.25 percent with increases occurring in stages through to 2027. Such a path would keep policy in a gradual normalization mode even as the central bank maintains that its stance remains accommodative in real terms.

Historical context points to the scale of the shift. According to long run series, Japan's policy interest rate has averaged about 2.22 percent from 1972 through 2025, with an all time high of 9.00 percent in December 1973 and a record low of minus 0.10 percent in January 2016. The return to positive and rising policy rates reflects a global pattern of higher inflation and tighter monetary settings, but Japan's experience is distinct because of its long era of near zero and negative nominal rates.

Looking ahead, markets will parse incoming wage and inflation data for evidence that price pressures are durable, while the government must balance stimulus priorities against rising financing costs. The Bank of Japan has signaled a cautious, data dependent approach, and investors and officials now prepare for a period of gradual normalization that will test the resilience of households, firms and public finances.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?