Canada’s new sovereign wealth fund faces scrutiny over Alberta’s cautionary lessons

Canada’s new fund will be judged less by its launch than by the rules that protect it. Alberta’s record shows how quickly public wealth can be pulled back into budgets.

The governance test

A sovereign wealth fund is only as durable as the rules that govern it. Ottawa can announce a new national pool of capital, but the real test will come later, when governments face deficits, political pressure and the temptation to treat long-term savings as short-term cash.

That is the warning from Alberta, where the Heritage Savings Trust Fund has spent decades proving a simple lesson: deposit rules, political discipline and withdrawal limits matter more than the splash of a launch. Without those guardrails, a fund meant to protect future generations can become another source of budget relief for the present.

What Ottawa is promising

The Prime Minister’s Office announced the Canada Strong Fund on April 27, 2026 as Canada’s first national sovereign wealth fund. The federal government said it would begin with an initial contribution of $25 billion and would invest alongside the private sector in Canadian projects and companies.

Ottawa is presenting the fund as part of a broader push to speed up major projects and build a stronger, more resilient and more independent Canadian economy. The pitch is both practical and political: the fund is meant to help finance nation-building projects and, at the same time, earn money.

But the basic mechanics are still unclear. Key details remain unresolved, including how the fund will generate returns, which kinds of projects it will back, and what structure will keep it from becoming just another arm of the federal state. The government has not yet fully settled whether the model will look like a classic state investment fund, a co-investment platform or a hybrid of the two.

That uncertainty is not a footnote. It is the story.

Why Alberta is the benchmark

Alberta’s Heritage Savings Trust Fund was created in 1976 with high ambitions and a familiar promise: turn resource wealth into a permanent public asset. The Alberta Heritage Savings Trust Fund Act received royal assent on May 19, 1976. In 1976-77, 30% of the province’s non-renewable resource revenue was directed into the fund, amounting to $620 million, and Alberta also made a special $1.5 billion transfer from its General Revenue Fund on August 30, 1976.

The original goals were clear: save for the future, strengthen or diversify the economy, and improve Albertans’ quality of life. Later provincial materials describe the Heritage Fund as Alberta’s main long-term savings account, and say it is supposed to retain part of its net income to keep pace with inflation.

Those are the right instincts for any public wealth fund. They also show why the rules matter so much. A fund can be designed for intergenerational fairness, but if lawmakers can repeatedly treat it as a reserve to be tapped, the promise fades.

How politics hollowed out the promise

Alberta’s fund never grew as large as it might have, because political withdrawals kept pulling money away. CBC reported in 2024 that more than $40 billion of interest from the Heritage Savings Trust Fund had been diverted into general provincial revenues over nearly five decades. In the same reporting, Alberta added $2.8 billion to the fund, bringing it to a record $30 billion.

That history is the cautionary tale Ottawa cannot ignore. A fund may be created with the language of stewardship, but once it is inside the machinery of government, every future cabinet inherits the same question: should this money stay protected, or should it help solve today’s fiscal problem?

Alberta’s oversight structure shows how formal the process can be without fully insulating the fund. The legislative committee tied to the Heritage Fund reviews quarterly reports, approves the annual report and holds a public meeting with Albertans about investment activity and performance. That transparency matters, but transparency alone has not prevented repeated raids on the fund’s earnings.

For communities, the stakes are not abstract. A sovereign wealth fund should be more than an accounting device. If it works, it can spread the benefits of natural resources and national investment across generations instead of concentrating them in one political cycle. If it fails, it can deepen the old pattern in which public wealth is promised to everyone but continually redirected to plug immediate holes.

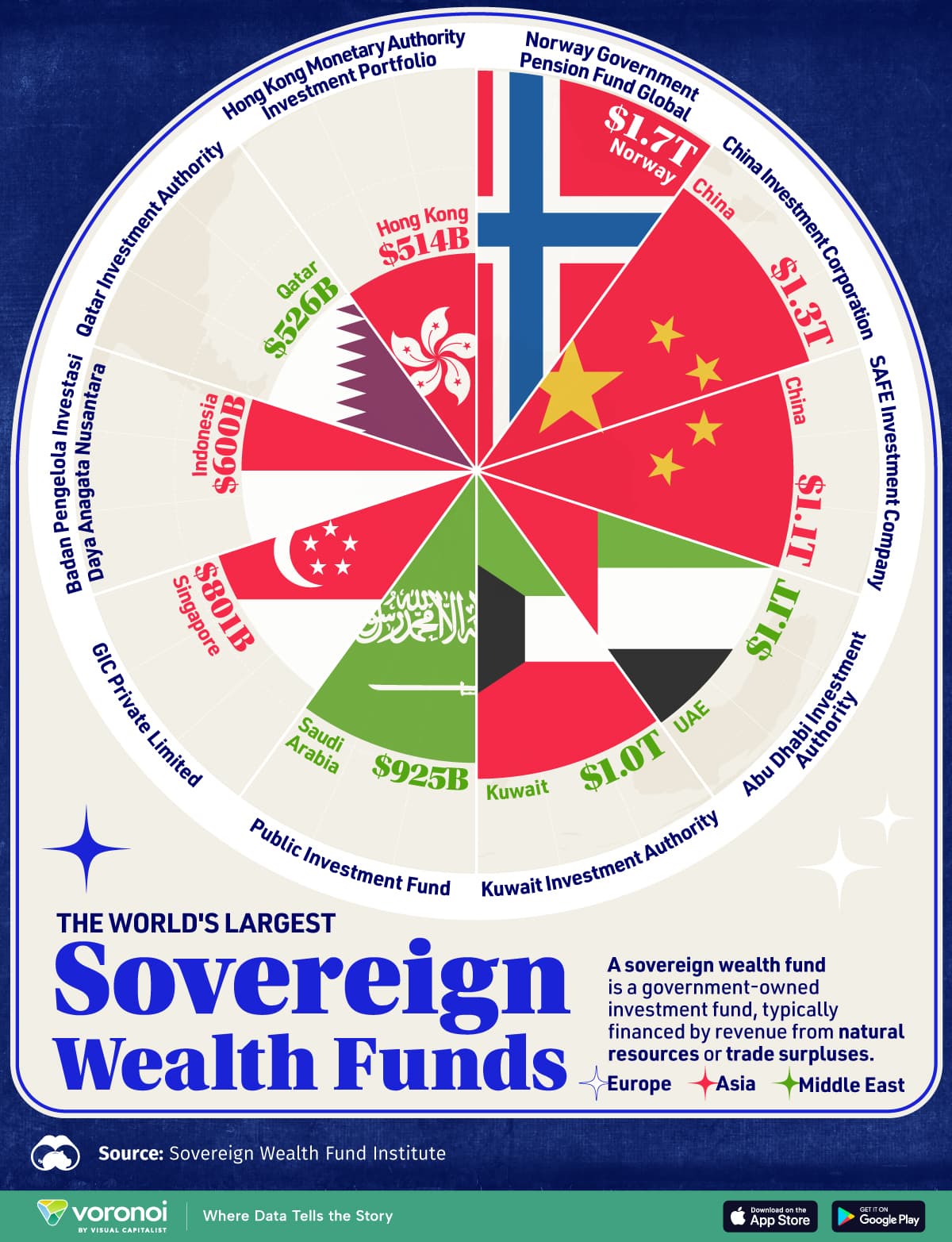

What the global example looks like

Canada is not entering an empty field. More than 100 sovereign wealth funds exist around the world, ranging from small state-level or Indigenous funds to global giants.

Norway’s Government Pension Fund Global is the most obvious benchmark. Norway says the fund is meant to manage oil and gas wealth for current and future generations, a mandate that makes its intergenerational purpose explicit. On March 27, 2026, Norway’s Ministry of Finance presented its 2026 white paper on the fund, and the public value display showed roughly NOK 20.656 trillion when accessed in early May 2026.

Norway’s scale is vast, but the lesson is not about size alone. It is about discipline, structure and the political patience to let the fund compound rather than consume it.

The questions Ottawa still has to answer

For the Canada Strong Fund to become a lasting national asset, the federal government will need to settle a few basic questions quickly and convincingly.

- What will count as an eligible investment, and what will not?

- Will withdrawals be capped, delayed or tied to strict conditions?

- Who will govern the fund, and how much independence will it have from day-to-day politics?

- Will earnings be reinvested, protected from routine budget use, or partly available for federal priorities?

- How will Ottawa keep the fund from becoming a convenient pot of money when political pressures rise?

Those are not technicalities. They are the difference between a public wealth fund and a public slush fund.

The danger for Ottawa is that the Canada Strong Fund could sound transformative while remaining structurally fragile. The opportunity is larger: if the rules are strong enough, Canada could build a genuine long-term asset that helps finance strategic investment without sacrificing future generations to present-day politics. Alberta’s record shows how easy it is to do the opposite.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?