China Clears Small Overdue Debts, Seeks to Restart Household Lending

China's central bank unveils a one off credit repair program to remove records of small overdue personal debts from official credit files, provided borrowers fully repay them by March 31, 2026. The measure targets pandemic era credit damage, aims to revive sluggish household borrowing, and will be implemented centrally by the PBOC's Credit Reference Center beginning in 2026.

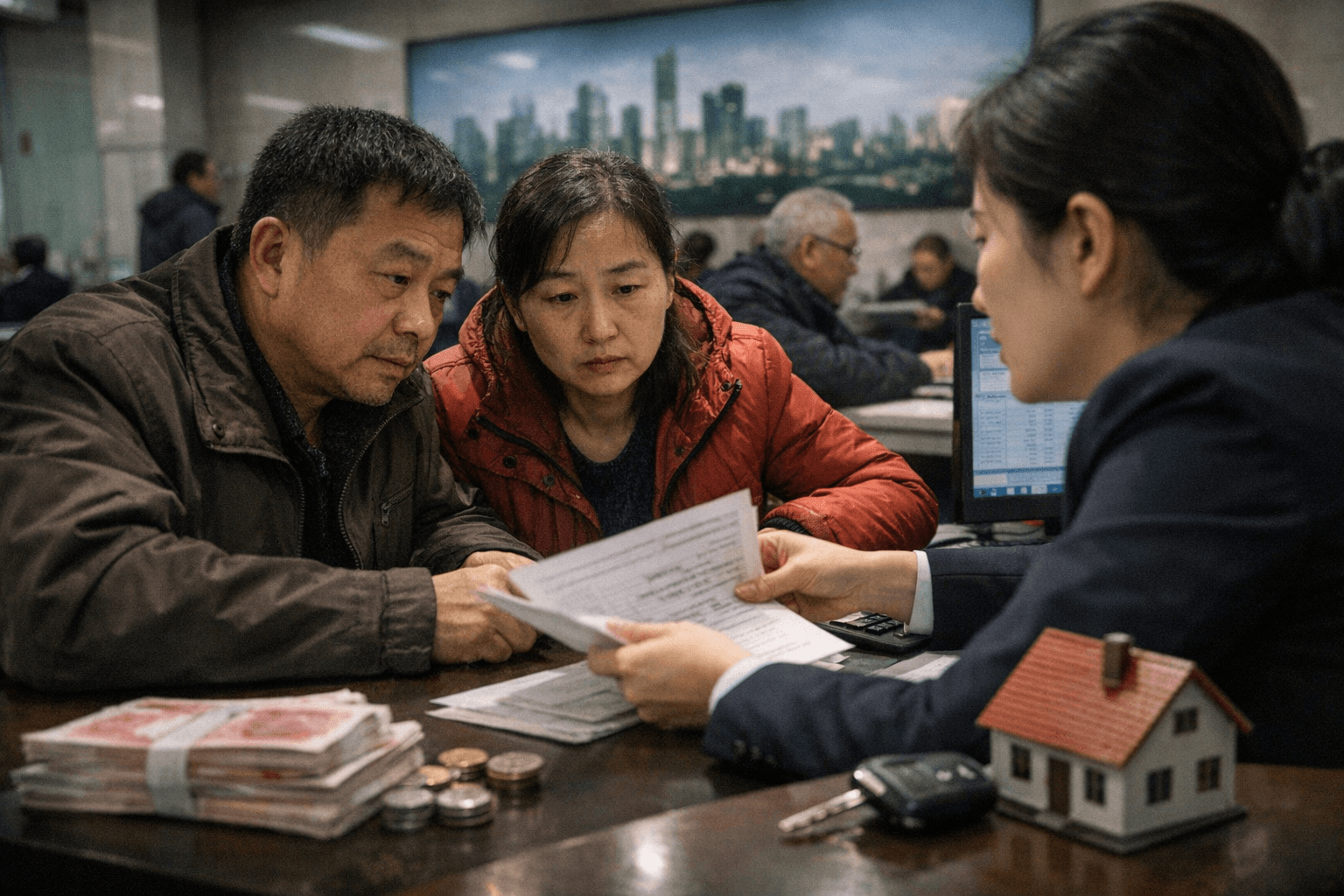

China's central bank and financial regulators announce a one off credit repair policy that will erase records of small overdue personal debts from the national credit database if borrowers repay them within a set window. The People’s Bank of China says individual overdue items of up to 10,000 yuan, roughly $1,420, incurred between January 1, 2020 and December 31, 2025 will qualify for removal once fully repaid by March 31, 2026.

The move is explicitly framed as part of post pandemic credit reconstruction aimed at alleviating the long tail of pandemic era arrears that continue to weigh on consumers' credit profiles. The PBOC instructs its Credit Reference Center to carry out the technical and administrative steps, and to process eligible cases centrally in batches beginning in 2026. Authorities say affected borrowers will not need to file individual applications for their records to be cleared.

By excising small overdue entries, regulators hope to reduce barriers that have kept households from accessing new loans, particularly for mortgages and consumer credit products where automated credit scoring can penalize even modest past delinquencies. Household borrowing in China has been sluggish since the pandemic and the property sector downturn, and policy makers are increasingly focused on measures that can restore credit supply and household consumption without large scale fiscal outlays.

The policy's ceiling of 10,000 yuan limits the scope to relatively small liabilities, and its one time nature reduces the immediate risk of moral hazard that might arise from a recurring forgiveness program. Still, key questions remain about how the change will play out in practice. It is not yet clear how quickly cleared entries will be reflected on commercial credit platforms, whether third party credit bureaus and private lenders will reload or reinterpret consumer files, and how institutions will treat accounts that are on payment plans or currently delinquent but brought current by the March cutoff.

The centralized, batch processing mechanism could accelerate implementation compared with a case by case application system, but timing details and technical timetables have not been fully disclosed. Regulators have set a clear repayment deadline of March 31, 2026 for eligibility, and have confined the incurrence window to the six year period beginning January 1, 2020. Those parameters make the scheme administratively straightforward, but they also leave unresolved how many consumers will benefit and what the aggregate value of removed debt will be.

For financial markets, the announcement could nudge credit conditions looser by improving credit scores for a subset of consumers and by signaling continued policy attention to demand side measures. Lenders may respond by adjusting underwriting criteria or marketing to previously marginal borrowers, though any sizable shift will depend on how commercial databases and bank risk models incorporate the cleared records.

The measure fits a broader pattern of Chinese policy makers seeking to repair household balance sheets and restart private sector credit growth after the prolonged shocks of the pandemic and property slump. The immediate impact will hinge on operational details and lender reactions, and those remain the priorities for journalists and analysts to monitor in the coming weeks.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?