China launches overnight reverse repo tool to fine-tune liquidity

China’s central bank offered 300 billion yuan through a new overnight reverse repo facility, sharpening focus on weak credit demand and cautious policy easing.

China's central bank said it conducted overnight reverse repo operations for the first time on Monday, offering 300 billion yuan to financial institutions as it widened the tools it uses to manage short-term liquidity. The move gave markets a clearer signal that Beijing wants more precision in funding conditions without committing to broad rate cuts.

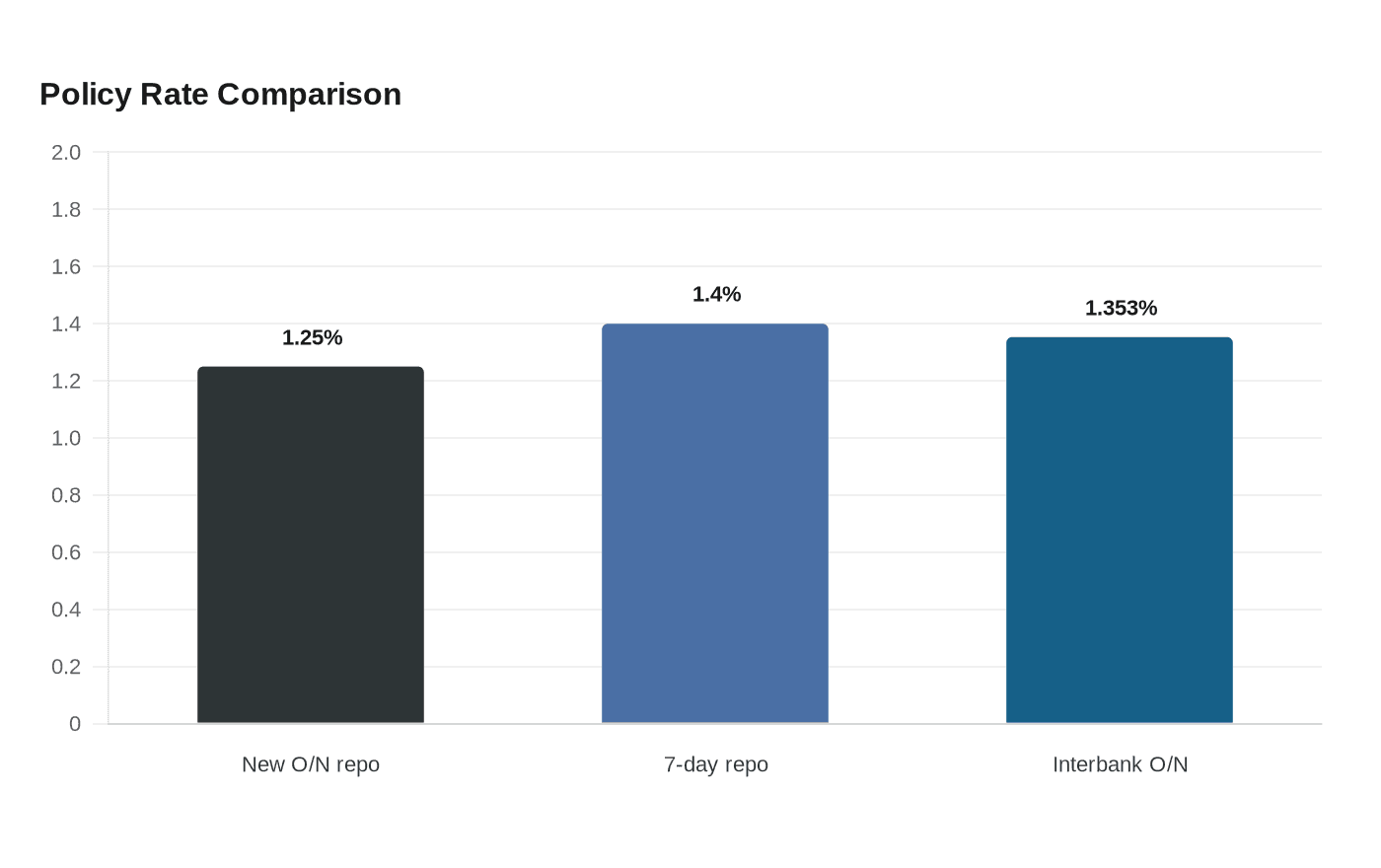

An overnight reverse repo is a short-term operation in which the central bank injects cash into the banking system against collateral, then takes that cash back the next day. In China’s case, the new facility sits alongside the seven-day reverse repo, which remains the main policy benchmark. Reuters sources said the inaugural overnight rate was set at 1.25%, 15 basis points below the seven-day rate of 1.4%, while the PBOC also added 157.5 billion yuan through seven-day reverse repos at the unchanged 1.4% rate.

That combination matters because it points to strain beneath the surface of China’s financial system. Officials are trying to support liquidity while avoiding a message that the central bank is moving into a larger easing cycle. The benchmark overnight repo in the interbank market traded at 1.3533% on Monday, about 2 basis points lower than the previous close, a sign that funding conditions were already fairly calm even as the PBOC stepped in with a new backstop.

Pan Gongsheng previewed the shift at the Lujiazui Forum in Shanghai on June 17, saying the PBOC would improve short-term interest-rate regulation and expand overnight reverse repo operations. State-media summaries of that forum said the central bank would build on temporary overnight repo and reverse repo operations introduced in July 2024 and narrow the operating corridor to 25 basis points above or below the seven-day reverse repo rate, reducing it from 70 basis points to 50 basis points.

Analysts at ING and ANZ said the design helps the PBOC preserve the seven-day instrument as its key policy signal while adding flexibility for month-end and quarter-end swings in liquidity. Before the debut, market expectations clustered around 1.30% to 1.35% for the new rate, and a Bloomberg-linked preview said a 1.25% rate or lower would be read as a de facto rate cut.

The timing also reflects the broader bind facing Beijing. Credit demand has been uneven, property weakness continues to weigh on growth, and direct financing through bonds and equities is taking on a larger role in the financial system. By refining overnight tools rather than moving the seven-day rate, the PBOC is signaling both caution and limits: it can fine-tune funding stress, but it is still trying to avoid the kind of broad easing that would imply deeper economic trouble.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?