China's December loan surge masks weakest annual lending since 2018

China's banks extended 910 billion yuan of new loans in December, but full‑year 2025 lending fell to the lowest level since 2018, underscoring fragile domestic demand.

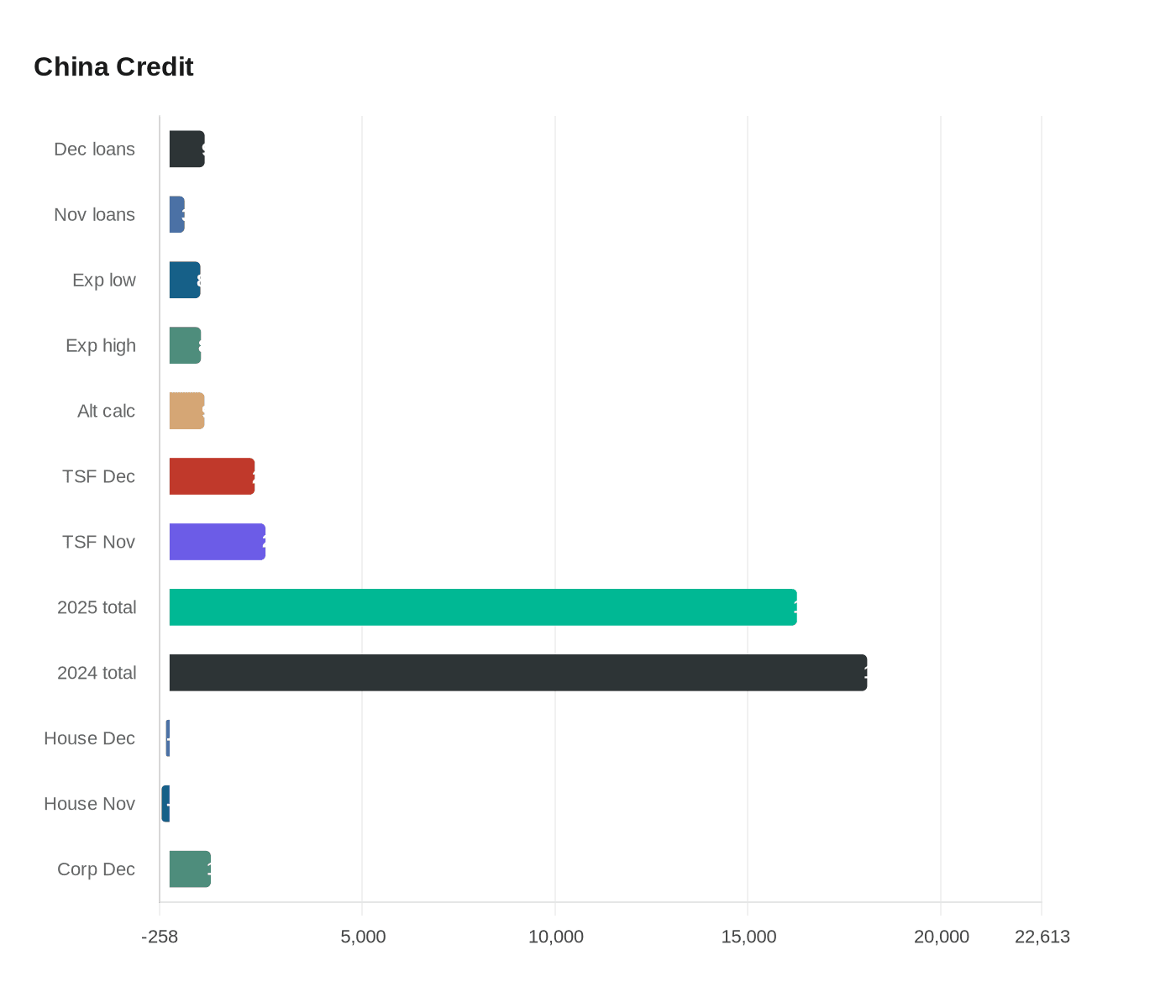

Chinese banks extended 910 billion yuan ($130.5 billion) of new yuan loans in December 2025, a sharp monthly rebound from 390 billion yuan in November, the People's Bank of China (PBOC) data released on Jan. 15 show. The month‑end surge outpaced market expectations, which had centered around 800-815 billion yuan, and slightly exceeds alternative calculations that put the total at about 908 billion yuan.

The broader picture, however, remains grim. Total social financing (TSF), the PBOC's wide measure of credit that includes non‑bank funding, was 2.21 trillion yuan in December, down from 2.49 trillion yuan the previous month. The M2 money supply accelerated to an 8.5% year‑on‑year rise in December from 8.0% in November, stronger than some forecasts and signaling rising liquidity even as borrowing appetite stayed muted.

For the full year, new yuan loans totaled 16.27 trillion yuan in 2025, the weakest annual total since 2018 and down from 18.09 trillion yuan in 2024. That decline highlights persistent softness in credit demand through the year despite episodic policy support. Calculations derived from the PBOC's cumulative series show household loans, including mortgages, contracted by about 91.6 billion yuan in December after a 206.3 billion yuan decline in November, while corporate lending expanded by roughly 1.07 trillion yuan for the month. The PBOC does not publish a detailed monthly breakdown, so these sectoral changes are derived by subtracting January‑to‑November cumulative figures from January‑to‑December totals.

Policymakers have stepped up targeted measures aimed at reviving lending. The central bank cut the rate on some structural monetary tools by 25 basis points in recent months and Beijing rolled out a 500 billion yuan policy‑based financing instrument in September to support project financing; authorities say that tool was fully deployed by late October and has backed more than 2,300 projects with total planned investment of roughly 7 trillion yuan. Officials also directed wider local government bond issuance to replace off‑balance‑sheet debt, a move that supported credit flows earlier in the year but whose offsetting impact has waned.

Analysts describe December's surge as a year‑end revival driven by corporate borrowing and the tail‑end effect of policy initiatives, rather than a broad rebound in household demand. The divergence between a strong single month and a weak annual total leaves the economy vulnerable: external resilience, including a near‑record trade surplus of nearly $1.2 trillion in 2025, has provided some support, but it has not fully offset domestic weakness in consumption and property investment.

Looking ahead, the policy mix appears likely to emphasize fiscal action more than an aggressive credit push. The PBOC has signaled a tolerance for a slower pace of credit growth, while fiscal tools and targeted financing are expected to carry much of the stimulus burden in 2026. For growth to reaccelerate sustainably, analysts say demand in the property sector and household consumption will need to recover, a process that could take many quarters even with continued policy support.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?