Chipmakers Hit Record Highs as Intel Turbocharges AI Rally

Intel jumped more than 24% to a record $83, pushing its market value above $416 billion and dragging rivals higher on AI demand.

Intel’s surge to a fresh record was enough to pull much of the chip complex with it, but the rally still looked more like a bet on AI-fueled earnings than a clean read on broad economic strength. Intel jumped more than 24% to $83 in early trading, lifted its market value above $416 billion and blew past its dot-com era peak. AMD and Arm each rose more than 11%, while Nvidia climbed more than 1%, a sign that traders were buying the idea that inference demand could put central processors back at the center of the AI buildout.

The immediate trigger was Intel’s first-quarter report and forecast, which showed demand from AI-services firms strong enough that the company sold chips it had already written off. Intel beat Wall Street estimates on revenue and profit, then guided second-quarter sales to $13.8 billion to $14.8 billion, above analyst expectations. HSBC and at least 22 other brokerages raised price targets after the report, with Intel’s median target moving to $75 from $46.50 a month earlier. The message from the numbers was clear: chip buyers are still spending, and they are spending hardest where AI data centers need Xeon server CPUs and other high-performance parts.

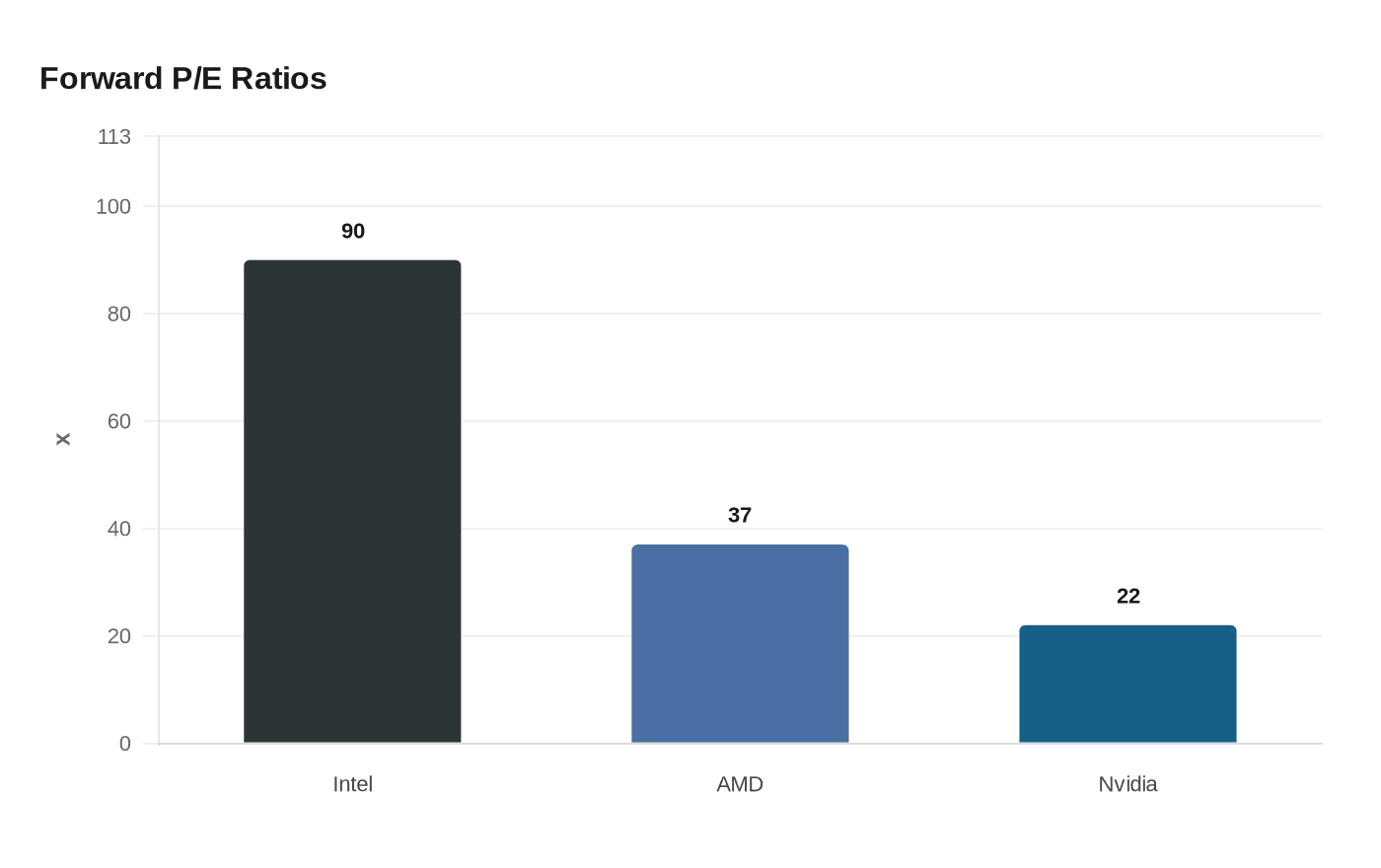

Yet the valuation gap shows how much momentum is already embedded in the trade. Intel was valued at about 90 times forward earnings, its highest multiple on record, compared with about 37 times for AMD and 22 times for Nvidia. That kind of pricing says investors are paying not just for orders and margins, but for a turnaround story that may still need several quarters of execution to justify itself. Intel also picked up a symbolic boost earlier in the week by securing Tesla as a customer for its next-generation 14A chipmaking process tied to Elon Musk’s Terafab project, reinforcing the idea that foundry ambitions are now part of the stock story as much as AI demand itself.

For retirement accounts and index investors, that concentration is the risk. When a small cluster of semiconductor names drives the advance, passive funds can absorb the downside quickly if AI spending normalizes, pricing eases or the second quarter lacks the inventory benefit Intel enjoyed in the first. The rally rests on real demand, but it is also carrying a heavy dose of expectation, and that leaves chipmakers vulnerable if the market decides the AI story has moved ahead of the earnings.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)