Citi initiates TeraWulf at buy, sees 39% upside after 500% surge

Citi’s new buy call on TeraWulf lands after a 500% rally, with a $36 target still implying nearly 40% upside from Friday’s $25.83 close.

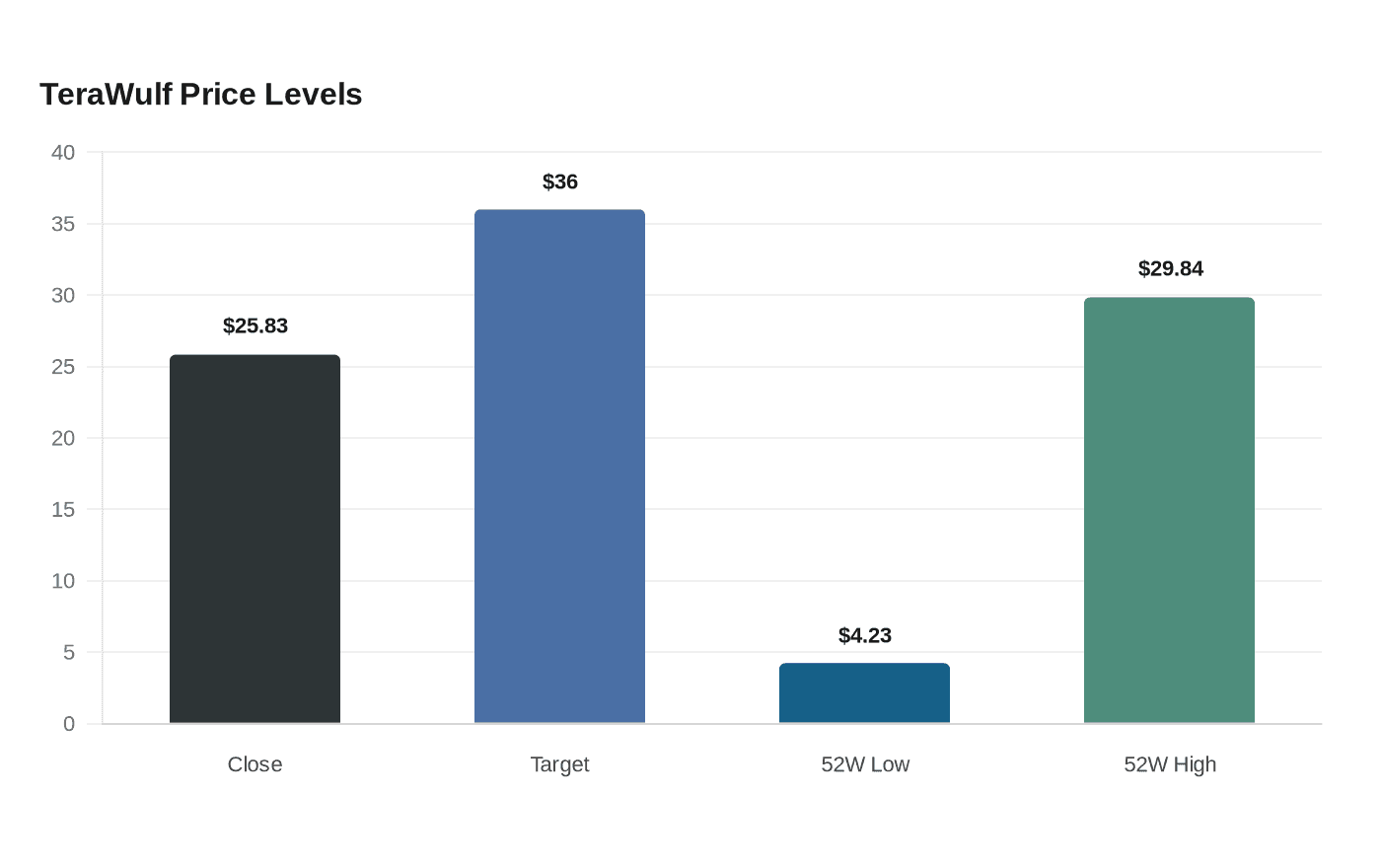

Citi began coverage of TeraWulf with a buy rating and a $36 price target, a call that still leaves about 39.4% upside from Friday’s close of $25.83. The stock has already climbed more than 500% over the past year, giving TeraWulf a market value of about $12.80 billion and a 52-week range that has swung from $4.23 to $29.84.

The call puts a spotlight on a trade that has been moving beyond simple bitcoin-mining exposure. TeraWulf describes itself as an owner and operator of energy-advantaged digital infrastructure built for high-performance computing and artificial intelligence, and its 2024 annual report said it was using scalable infrastructure and low-cost, predominantly zero-carbon energy to support both bitcoin mining and HPC hosting. That positioning has turned the company into a way for investors to bet on power, land and data-center capacity as much as on software or semiconductors.

The company has been trying to prove that shift in hard numbers. In August 2025, TeraWulf announced two 10-year HPC colocation agreements with Fluidstack, then later said Fluidstack’s contracted critical IT load at Lake Mariner in New York had risen to about 360 MW after an expansion. In May 2026, TeraWulf said first-quarter revenue was expected to land between $30 million and $35 million and adjusted EBITDA between $0 million and $3 million, while also saying it had closed a $250 million revolving credit facility.

Its first-quarter 2026 results showed both the promise and the strain of that pivot. TeraWulf said HPC lease revenue made up 62% of total revenue, with $21 million generated from 60 MW of energized capacity at Lake Mariner. The company also reported a large net loss driven by non-cash items, a reminder that the earnings story is still being rebuilt around contracted power and hosting rather than legacy mining economics.

That tension is what makes Citi’s call notable after such a sharp run. A fresh bullish rating can reinforce the idea that investors are paying for durable infrastructure demand tied to AI buildout and data-center bottlenecks. It can also raise the bar for what comes next, because after a 500% advance, further upside depends on TeraWulf converting more power assets into long-duration cash flow and hitting its target of 250 to 500 MW of new contracted capacity a year.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?