Company Pushes Deeper Into AV Industry With Consumer-Facing Bet

Uber is trying to turn AVs into a platform business, not just a ride option, and the real prize is controlling demand before carmakers do.

Uber is moving from app to operating layer

Uber is no longer treating autonomous vehicles as a side bet. The company has launched Uber Autonomous Solutions, built Uber AV Labs, and stitched together partnerships that put its app in front of robotaxi riders while supplying partners with data, mapping, support, and fleet tools. That is a classic race against disintermediation: if Uber can own the consumer surface and the operational rails, it stays central; if not, the AV makers can use the same cars to pull the customer relationship away.

The company’s latest moves show how broad that ambition has become. In February, Uber said Autonomous Solutions would organize its AV push around infrastructure, user experience, and fleet operations, giving partners more than raw access to demand. By spring, Uber was adding hotel bookings and new travel tools to the app, a sign that it wants the consumer relationship to extend beyond one ride and into a wider daily-use platform.

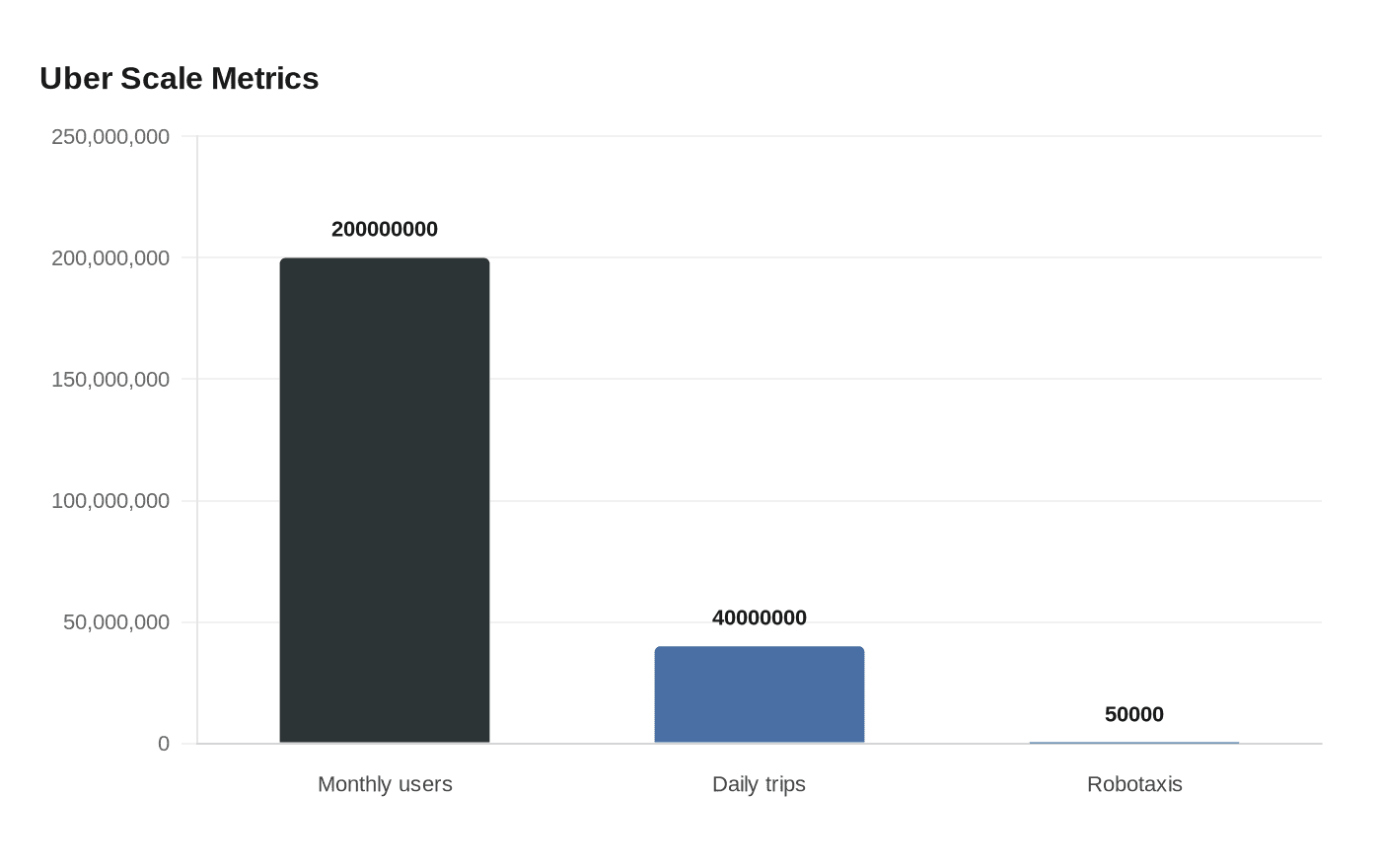

Why the consumer app still matters most

Uber’s strongest asset may be less the cars than the habit. The company said in its full-year 2025 results that it had more than 200 million monthly users completing more than 40 million trips every day, a scale that gives it an unmatched place to launch new mobility products. The strategic logic is simple: AV developers need riders, and Uber already has the digital storefront where those riders start their search.

That is why the consumer-facing bet matters as much as the backend tools. Uber’s platform strategy is not limited to robotaxis alone. The company has been folding in hotels, travel integrations, shopping features, and broader in-app services, while Dara Khosrowshahi has framed the effort as deepening Uber’s role in daily life and becoming an app for everything. In AV terms, that means the company is trying to make the Uber app the place where a user books, compares, and repeats mobility choices, regardless of whose car is underneath.

Data is the sharpest weapon in the AV stack

If customer demand is the front door, data is the engine room. Uber AV Labs says autonomy has become a data and modeling race, and it argues that few companies have more real-world driving data than Uber because of its billions of trips. Uber Autonomous Solutions adds that its data-collection fleets and dashcam networks have captured over 100,000 hours and millions of miles of footage across the US and Europe, which it uses to help partners train toward Level 4 autonomy.

That matters because the company is not only selling access to riders. It is also trying to sell the industrial plumbing of autonomy: training data, dynamic mapping, regulatory access, financing, real-time support, and the software layer inside the vehicle. In practice, that means Uber is positioning itself as a utility partner for AV companies that need scale but do not want to build every back-office function from scratch.

The partnership model gives Uber leverage, but also exposes the risk

Uber has been moving quickly to populate its network with partners rather than building the cars itself. The company and Waymo brought autonomous ride-hailing to Austin and Atlanta on the Uber app, Uber and Avride launched robotaxi rides in Dallas, and Uber and WeRide began fully driverless fare-charging operations in Dubai. Uber also announced partnerships with Motional in Las Vegas, Lucid and Nuro for a global robotaxi service, and Rivian for up to 50,000 fully autonomous robotaxis over time.

Those deals reveal both the strength and fragility of the model. On one hand, Uber keeps the rider inside its app and can dispatch a mix of autonomous vehicles and human drivers on the same platform, which is exactly how it preserves choice and continuity for customers. On the other hand, the AV companies still own the core hardware and often the underlying autonomy stack, which means they can decide whether Uber remains the front end or gets reduced to a distribution channel.

Uber’s answer is to become indispensable on every layer that sits between the car and the customer. Its Autonomous Solutions pitch emphasizes demand generation, rider experience, customer support, and fleet management, while the AV Labs program turns the company’s human-driven network into a source of training signals for partners. The bet is that AV makers will need Uber’s demand, logistics, and data more than Uber will need any single AV supplier.

The real strategic question is ownership

The key question is not whether Uber will have AVs in its app. It already does, and the pipeline is widening across the US, Europe, the Middle East, and beyond. The question is whether the app remains the primary consumer relationship when the market matures, or whether the AV companies use Uber to reach scale before taking more of the value for themselves.

Uber’s current strategy is designed to prevent that squeeze. By pairing consumer products like hotel bookings and expanded travel tools with AV partnerships and data services, the company is trying to become more than a ride-hailing app and more than a middleman. If that effort works, Uber will own both demand and distribution in the AV era. If it fails, the cars may still arrive through Uber, but the most valuable relationship will sit somewhere else.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?