Credit card debt won’t affect Medicare eligibility, but can strain retirement costs

Credit card debt will not keep you off Medicare, but it can still push retirement health costs higher, from delayed enrollment to heavier premium and drug bills.

Credit card debt does not decide whether you can get Medicare. Eligibility generally hinges on age, disability status, or certain conditions such as end-stage renal disease or ALS, and people sign up for Original Medicare, Parts A and B, through Social Security. Work history matters for whether Part A is premium-free, not for whether debt blocks access in the first place.

Medicare eligibility is separate from consumer debt

That distinction is the core myth to bust. Medicare is a federal health insurance program for people age 65 or older, with some younger people qualifying through disability or qualifying medical conditions, and the application path for Part A and Part B runs through Social Security. Credit card balances, collection notices, or other household debts do not enter the eligibility test.

What debt can do is shape the rest of the retirement health equation. Original Medicare has no yearly out-of-pocket maximum unless you add supplemental coverage such as Medigap or enroll in a Medicare Advantage plan, so bills can accumulate through deductibles, coinsurance, copayments, and services Medicare does not cover. That is where financial strain can start to influence choices even when eligibility itself is untouched.

Where the bills hit hardest

Medicare’s own billing system helps explain why retirees can feel squeezed. Most people have their Part B premium deducted automatically from Social Security benefits, but if they do not get Social Security or Railroad Retirement Board benefits, Medicare sends a premium bill. For people who pay directly, Part B is billed every three months, while Part A premiums are billed monthly if they are owed.

Missed enrollment can make the pressure worse. Medicare says the Part B late-enrollment penalty is generally an extra 10% for each year someone could have signed up but did not, although that penalty can be avoided if the person qualifies for a Special Enrollment Period or enrolls in a Medicare Savings Program. In other words, debt does not block Medicare, but cash-flow problems can push someone into a more expensive path if they delay action.

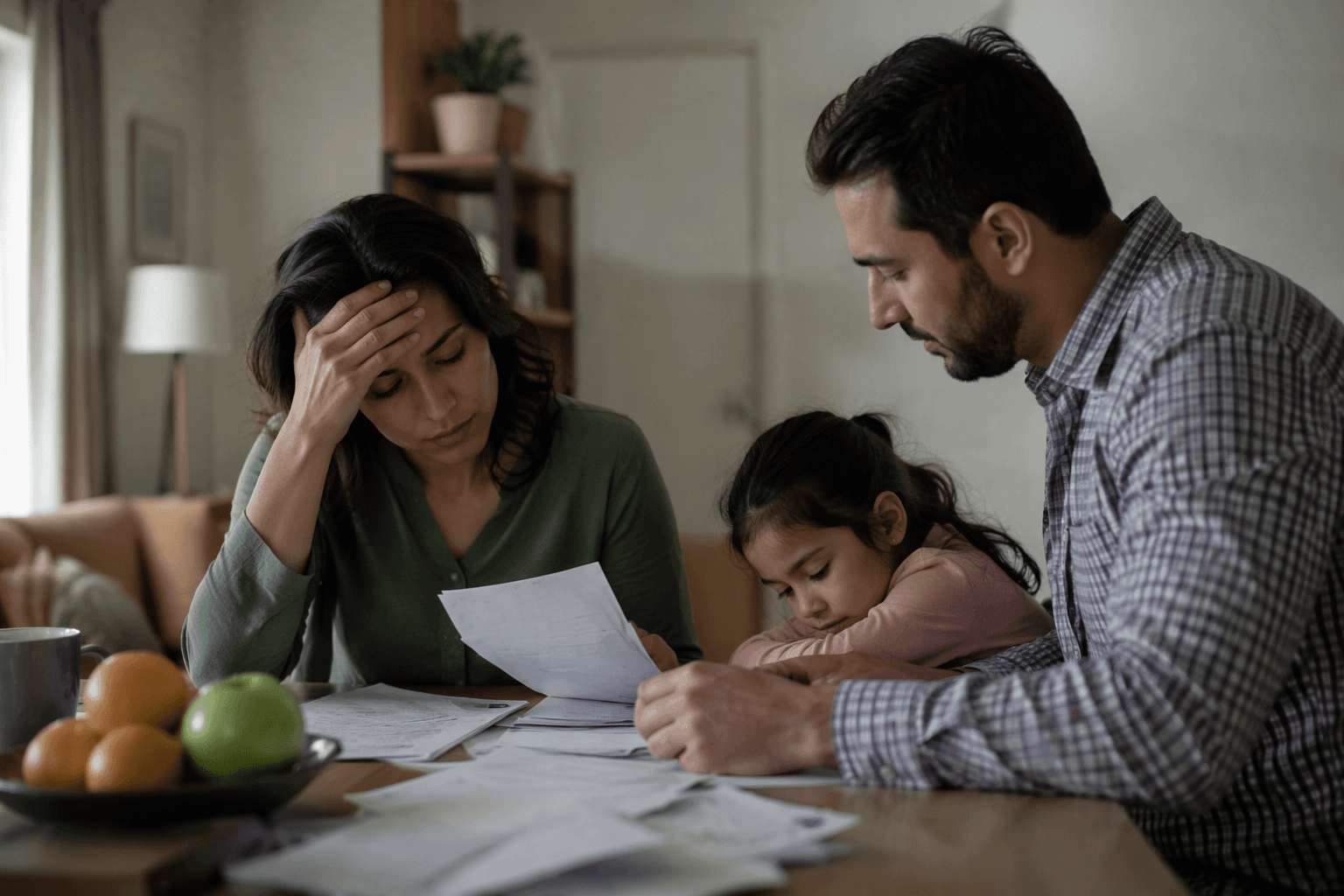

Debt in retirement is already widespread

The Medicare question sits inside a larger retirement balance sheet problem. The National Council on Aging says more older adults are carrying debt into retirement, and identifies medical debt, credit card debt, and mortgage debt as three of the most common categories. AARP’s research adds that nearly half of adults 50 and older carry credit card debt from month to month, with unexpected expenses a major driver.

That matters because credit card debt is expensive debt. AARP found that everyday expenses, housing costs, vehicle costs, and health care costs are all common reasons older adults lean on credit cards, and 87% of those carrying card balances said unexpected expenses contributed to that debt. For retirees living on fixed income, that mix can make a premium bill, a dental visit, or a prescription refill feel like a budget shock rather than a routine expense.

Medical debt is common even with Medicare

The broader health-cost burden is not theoretical. KFF found that in 2022, 22% of U.S. adults age 65 and older reported some form of debt from medical or dental bills, and among Medicare-age adults with health care debt, 29% said their household had been contacted by a collection agency in the prior five years while 23% said the debt hurt their credit score. KFF also found that many of those debts came from ordinary care, including lab fees and diagnostic tests, dental care, and doctor visits.

The Consumer Financial Protection Bureau paints a similar picture from the billing side. It says nearly four million adults 65 and older had unpaid medical bills in 2020, even though 98% had health insurance, and those unpaid bills totaled $53.8 billion, up 20% from 2019. The CFPB also notes that inaccurate bills and attempts to collect amounts not owed can feed coercive credit reporting and financial damage among older adults.

Medicare can ease distress, even if it does not erase it

There is one important counterpoint to the debt narrative: Medicare eligibility itself can reduce financial distress. A National Bureau of Economic Research analysis found that reaching Medicare eligibility was associated with a drop in debts in collection of just over $28, a 30% reduction, using credit panel data around age 65. The researchers also found no evidence that Medicare eligibility affected the likelihood of credit card delinquency or bankruptcy.

That suggests Medicare can act as a partial pressure valve, especially in states where many people aged 55 to 64 are uninsured. The same analysis found that increased insurance coverage after Medicare eligibility explained about a third of the decline in collection debt, and that the biggest drops occurred in places with higher poverty rates and larger baseline debt burdens. The policy implication is straightforward: Medicare is more likely to relieve financial strain than to be blocked by it.

Help programs matter when budgets are tight

For people who are struggling, Medicare has separate cost-help programs that can make the difference between coverage and a credit card charge. Medicare Savings Programs help eligible people with limited income and resources pay Part A and Part B premiums, and may also help with deductibles, coinsurance, and copayments. Extra Help is the drug-cost program, and it can lower Part D premiums, deductibles, coinsurance, and other prescription costs.

Those programs can also protect against extra penalties. Medicare says people who get Extra Help do not have to pay the Part D late-enrollment penalty while they receive it, and some people qualify automatically through Medicaid, a Medicare Savings Program, or Supplemental Security Income. The practical takeaway is that if debt is squeezing your budget, the safest move is often to check for assistance before costs snowball.

Why the policy debate is still active

Advocates keep pushing because the pain point is affordability, not eligibility. AARP is pressing to keep medical debt off credit reports, the CFPB says it is working to stop unfair medical debt collection and coercive credit reporting, and the Medicare Rights Center argues that Medicare’s out-of-pocket costs remain burdensome for many enrollees. Together, those positions underline the same reality: the system does not ask how much credit card debt you carry, but it can still leave you exposed to high costs that strain household finances.

Credit card debt therefore belongs in the Medicare conversation, just not as a gatekeeper. It is a symptom of retirement pressure, a factor that can delay enrollment or limit supplemental coverage, and a warning sign that premiums and medical bills may already be crowding out other essentials. The rule is simple, but the economics are not: debt does not decide Medicare eligibility, yet it can still decide how comfortably you can afford to use Medicare.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip