Dollar rebound seen fading as strategists forecast weaker months ahead

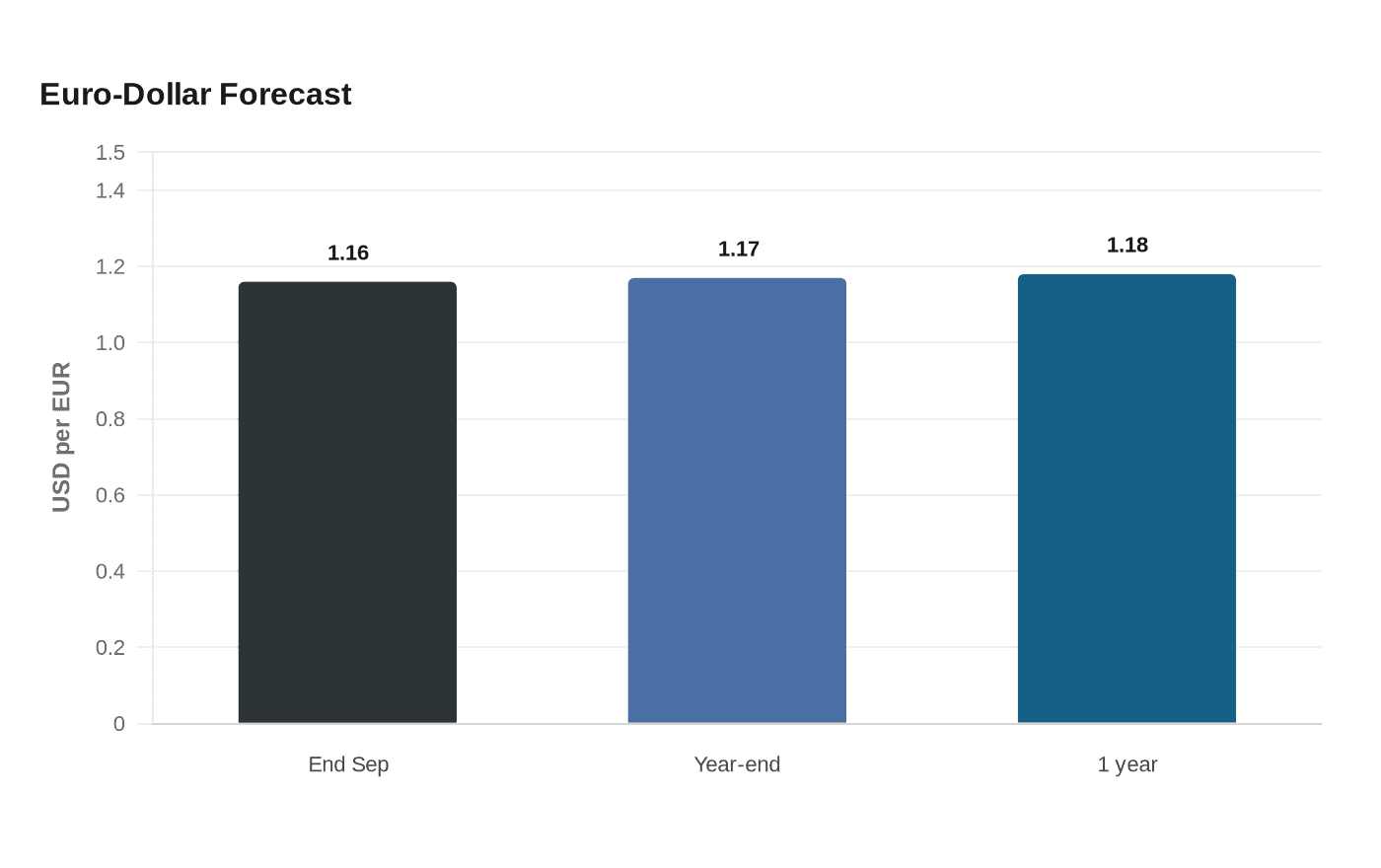

The dollar has climbed 4% from its May low, but strategists still see it slipping later this year. The median euro forecast points to 1.18 within a year.

The dollar’s 4% rebound from its May low still has momentum, but a Reuters poll of foreign exchange strategists taken from June 26 to July 1 found that most still expected the rally to fade over the coming months. The move has been supported by lower crude prices, which have drifted back near pre-war levels after the U.S.-Israeli war with Iran eased, along with a resilient U.S. economy, elevated Treasury yields and market expectations that the Federal Reserve may keep policy tighter for longer.

That near-term strength has been reinforced by positioning. Long-dollar bets in futures markets rose to their highest level since January 2025, according to Commodity Futures Trading Commission data, while interest rate futures were pricing in almost two Fed hikes by year-end. Even so, the survey’s median forecast pointed the other way over time, with euro-dollar seen at 1.16 by the end of September, 1.17 by year-end and 1.18 in one year.

Jane Foley, a strategist at Rabobank, said the market could eventually strip out those expected rate hikes, which would hit the dollar. “Pricing out those hikes would weigh on the dollar,” she said, adding that the coming weeks could be choppy. That tension between immediate support and a softer later path is shaping trading across currencies, especially as investors weigh whether inflation staying above target and the Fed’s policy debate can keep the greenback firm for much longer.

The poll also showed how crowded the bullish trade had become. Among 41 respondents, 71% said current net-long positioning would hold or increase by the end of July, and none expected it to swing to net-short. At the same time, about one-third of the 70 strategists surveyed said euro-dollar would stay flat or edge lower over three months, up from about one-fifth in June, showing how many traders still see room for more dollar strength before any broader reversal.

That split matters well beyond currency desks. A stronger dollar can hold down import prices for U.S. consumers and businesses, but it also makes travel abroad more expensive and cuts into the overseas earnings of American multinationals when they are translated back into dollars. For governments and borrowers with dollar debt, the direction of the currency can change servicing costs quickly. A Reuters analysis earlier this year said the dollar still looked overvalued on a real basis, with a wider U.S. budget deficit, doubts about Fed independence, tariff worries and improving growth outside the United States all pointing to a weaker medium-term backdrop.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?