Experts see no quick return to 5% mortgage rates in 2026

Five percent is the real mortgage threshold. Even if 2026 stays closer to 6%, the payment gap would reshape what buyers can qualify for.

The monthly-payment line that matters

A 5% mortgage rate would change the math for buyers more than it would validate any forecast. On a typical $417,700 existing home, with 20% down, the loan amount is $334,160; at Freddie Mac’s 6.36% average in mid-May, principal and interest come to about $2,081 a month. At 5%, that payment falls to about $1,794, a drop of roughly $288 a month. Using a common 28% housing-cost benchmark, the income needed to qualify would fall from about $89,200 a year to about $76,900, and the same monthly payment would support roughly $67,000 more home price.

That is why a move to 5% matters most for first-time buyers and refinancers. For someone trying to stretch into a home, or lower the payment on an existing balance of about $334,160, the rate gap is not abstract. It is the difference between a payment that feels manageable and one that clears enough room in the monthly budget to make the deal work.

Why experts do not see a quick return

Most economists still see mortgage rates drifting lower only gradually, not snapping back to 5% anytime soon. Heather Long, chief economist at Navy Federal Credit Union, said, "I don't foresee the 30-year mortgage rate dropping close to 5% again in the foreseeable future." She tied any meaningful improvement to geopolitics, saying that if the war in Iran ends, mortgage rates could move back toward 6%, but that a longer conflict would keep inflation, defense costs, bond yields, and borrowing costs elevated. Melissa Cohn, regional vice president of William Raveis Mortgage, also sees the geopolitical climate as one of the main forces shaping rates right now.

The Federal Reserve added another reason not to expect a fast drop. In its April 29 statement, the Fed said inflation is elevated in part because of higher global energy prices, while job gains have remained low on average and unemployment has been little changed. That mix does not point to a sudden easing in borrowing costs, especially when broader uncertainty around the Middle East is still feeding market caution.

The housing market is still absorbing today’s rates

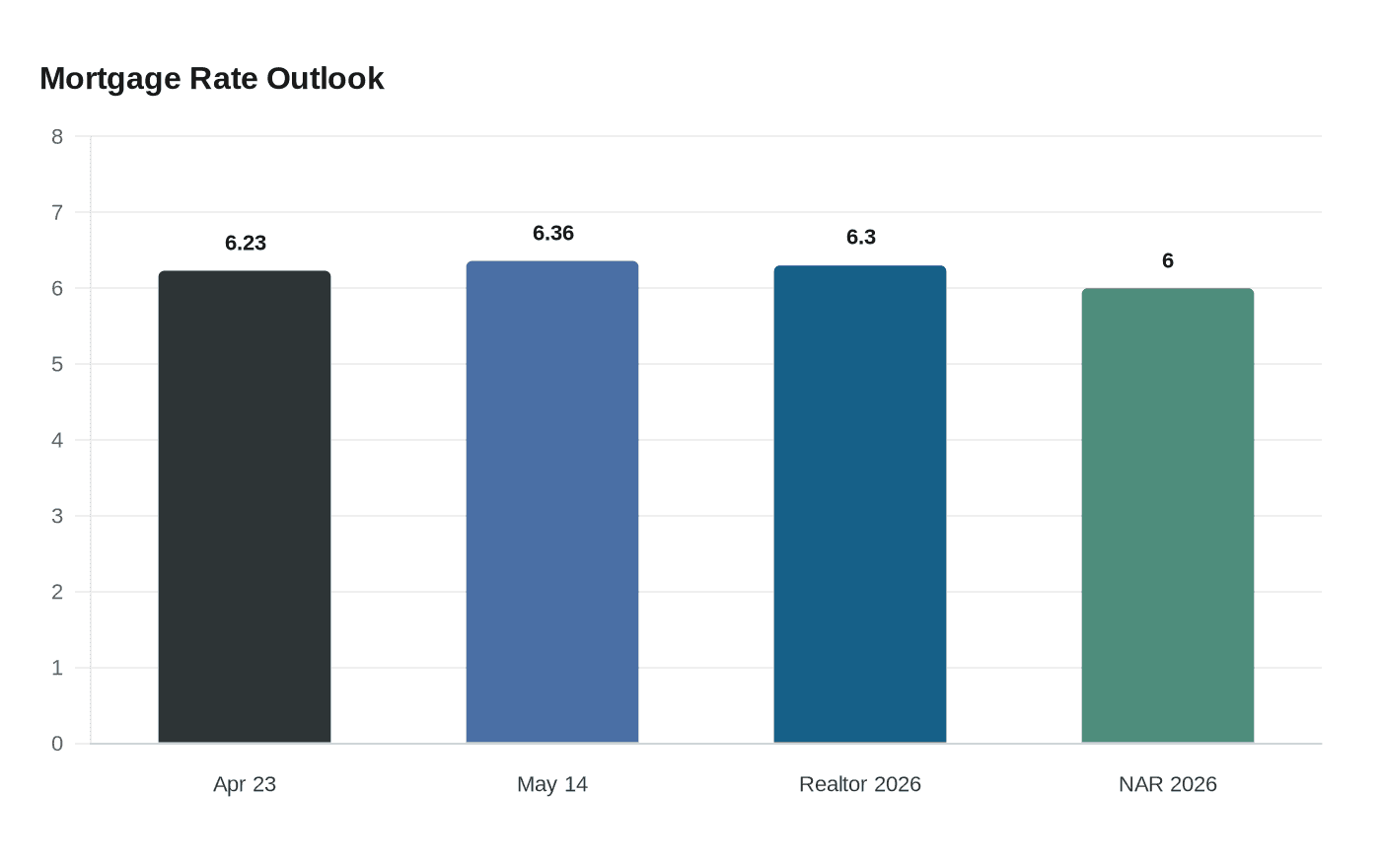

The latest housing data show resilience, not relief. Mortgage applications rose 1.7% in the week ending May 8, even with rates near a recent peak, which suggests some buyers are adjusting to the new normal rather than standing aside completely. Freddie Mac’s benchmark 30-year fixed-rate mortgage averaged 6.23% on April 23 and 6.36% by the week of May 14, while the Mortgage Bankers Association’s increase showed purchase demand still moving through that range.

Affordability has improved from last year, but only in increments. The National Association of Realtors’ Housing Affordability Index rose to 110.6 in April 2026 from 101.4 a year earlier, yet the median existing-home price still climbed to $417,700, up 0.9% from a year earlier, and inventory remained limited at 4.4 months’ supply. In other words, incomes and supply are helping at the margin, but they have not erased the burden created by higher financing costs.

What 2026 is likely to look like instead

The more realistic baseline is a steadier housing market, not a dramatic reset. Realtor.com’s 2026 forecast expects average 30-year mortgage rates of about 6.3% and says inventory should continue to recover, while existing-home sales rise modestly. Lawrence Yun, NAR’s chief economist, expects rates to average around 6% in 2026, but not a return to 3% borrowing costs. That leaves 6% as the more plausible psychological target, not 5%.

Freddie Mac’s long-running Primary Mortgage Market Survey, which has tracked weekly mortgage-rate data since 1971, puts the current cycle in perspective. The market has already moved down from the spike above 7% seen in earlier periods, but the next leg lower is likely to be slow and uneven. If geopolitical pressure eases and inflation cools, borrowers may get closer to 6% first. For buyers and refinancers, that is still meaningful progress, even if the clean break to 5% never arrives in 2026.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?