Expired ACA tax credits drive sharp premium hikes for millions of Americans

Millions face a 114% jump in ACA premium payments as tax credits lapse, with middle-income households above Medicaid limits losing the most help.

Congress’s refusal to extend the enhanced ACA tax credits is already showing up in household budgets: KFF estimates that subsidized Marketplace enrollees who stay in the same plan will see their premium payments rise 114% on average in 2026. The sharpest blow lands on working- and middle-income families who earn too much for Medicaid but not enough to absorb the higher monthly bill, and many people above 400% of the federal poverty level will lose eligibility for any credit at all.

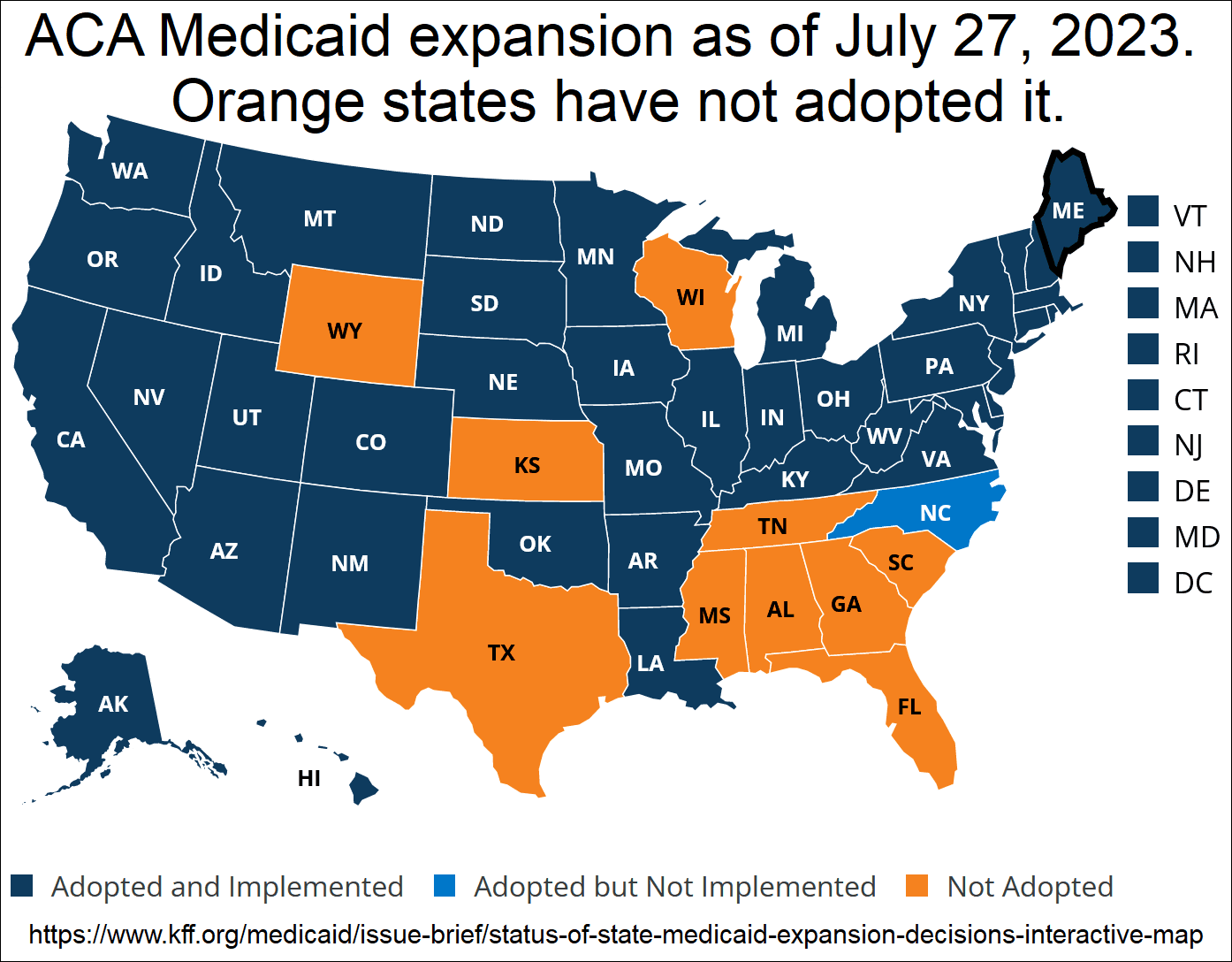

The credits, created in 2021 and extended through the end of 2025 by the Inflation Reduction Act, helped fuel one of the biggest coverage expansions in the law’s history. KFF says Marketplace enrollment climbed from about 11 million people to more than 24 million after the subsidies were enhanced, with the vast majority of enrollees getting some form of increased assistance. Without that help, the affordability squeeze is landing first on households that have no room in their budgets for a sudden jump in premiums.

Federal data show the pressure point. The 2026 Marketplace open enrollment period ran from Nov. 1, 2025, through Jan. 15, 2026, and the Centers for Medicare & Medicaid Services projected that the average HealthCare.gov premium after tax credits would be $50 a month for the lowest-cost plan, up $13 from 2025. By Jan. 28, 2026, 23.0 million consumers had selected 2026 Marketplace coverage nationwide, down from 24.2 million at the same point the year before. In the 30 HealthCare.gov states, 15.8 million selections had been recorded.

The selection totals, however, do not tell the whole story. KFF says plan-selection data do not show whether people actually pay premiums and keep coverage, so effectuated enrollment will be lower than the sign-up numbers. CMS also said it ended advance premium tax credits or coverage for nearly 1.5 million people found ineligible for financial assistance or enrolled without authorization on HealthCare.gov, a step that affected returning-consumer counts.

The mix of plans also shifted. CMS said bronze and gold selections made up a larger share of enrollment in 2026, while silver-plan selections fell from 56% in 2025 to 43% in 2026. That pattern suggests consumers are adjusting to higher prices by moving away from the plans that once drew the broadest interest.

Health groups are warning that the fallout will not stop at premiums. The American Heart Association said it was “deeply disheartened” by Congress’s failure to extend the credits and warned that the price increases threaten affordability for people managing cardiovascular disease and other chronic conditions. The full damage will unfold over months, but the policy choice in Washington, D.C. is already translating into fewer options, higher bills and more uninsured Americans.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?