FCA scheme could delay billions in car finance compensation payouts

Millions of drivers who expected compensation for mis-sold car finance face another wait as the FCA’s £7.5 billion redress plan is tested again.

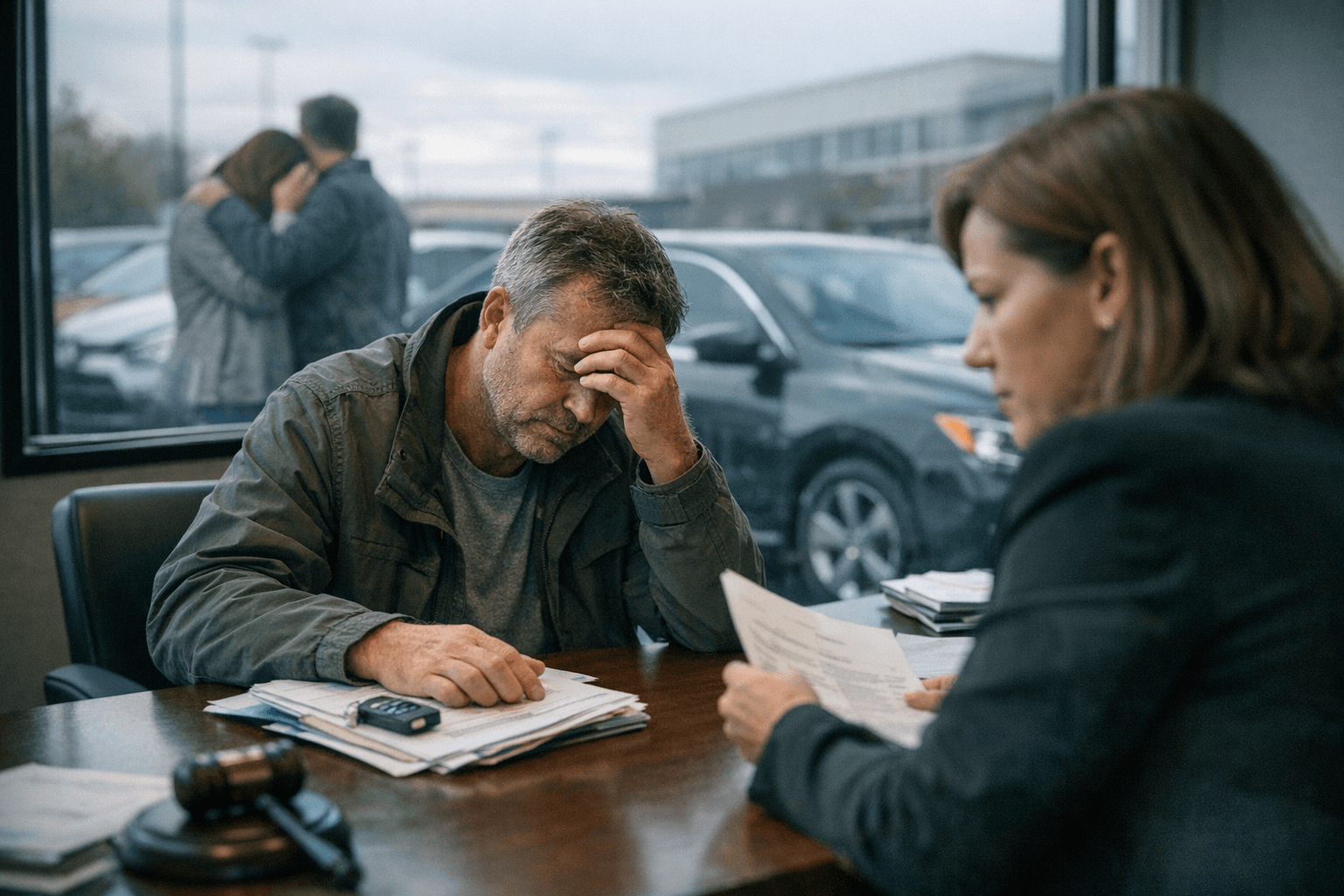

Millions of drivers who thought compensation for mis-sold motor finance was finally within reach now face another stretch of delay. The Financial Conduct Authority’s scheme, built to return £7.5 billion to consumers, has already become entangled in fresh legal and industry pressure, risking a slower path for households that have waited years for redress.

The dispute stems from car finance deals in which lenders paid commissions to motor dealers, often with no disclosure or only partial disclosure to customers. The UK Supreme Court said on 1 August 2025, in the joined cases of Hopcraft, Johnson and Wrench, that the commission model had been widespread for at least 75 years and was of major significance because most cars are bought on credit. That judgment followed a Court of Appeal ruling on 24 October 2024 and triggered the FCA’s decision, announced on 3 August 2025, to consult on an industry-wide compensation scheme.

The regulator said many firms did not comply with the law or disclosure rules in force when they sold loans, and it estimated that 14.2 million agreements, about 44% of all motor finance agreements made since 2007, could be classed as unfair because of inadequate disclosure. Under the final scheme introduced on 30 March 2026, customers treated unfairly between 2007 and 2024 are in line for payments, with millions of claims expected to be settled in 2026 and the vast majority by the end of 2027. The FCA also set deadlines of 30 June 2026 for loans taken out from 1 April 2014 and 31 August 2026 for earlier agreements.

The scale is large enough to ripple through Britain’s motor finance market. More than 2 million used and new vehicles are still bought each year using motor finance, and lenders have warned about the hit from provisions, redress costs and market stability. The FCA has argued that an industry-wide approach is the quickest and most cost-effective way to deliver fair compensation while preserving a well-functioning market, and it said it received more than 1,000 consultation responses from consumer groups, lenders, investors, manufacturers, trade bodies and others.

The episode recalls earlier mass mis-selling scandals in Britain, including pensions mis-selling, which the Financial Services Authority said cost at least £11.8 billion and affected more than one million customers. Each new delay risks deepening the same problem: the longer compensation takes, the harder it becomes to sustain public confidence that redress systems can deliver speed, scale and fairness at the same time.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?