Fed faces pivotal transition as Powell exits, Warsh awaits confirmation

Powell’s last Fed meeting has markets pricing no rate move and bracing for a leadership shift that could reshape borrowing costs and confidence.

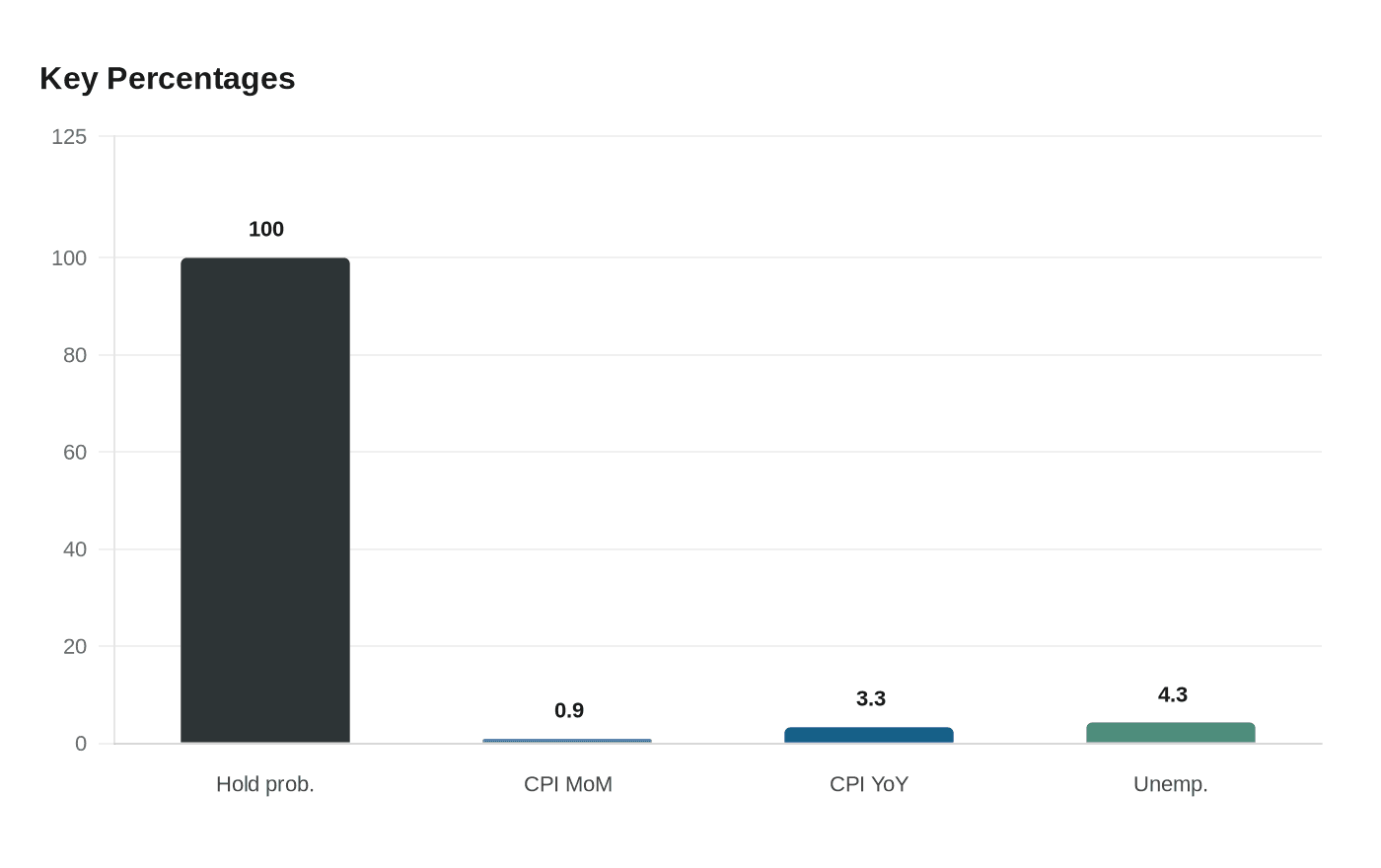

Jerome Powell’s final Federal Reserve meeting as chair landed with markets already convinced the central bank would do nothing. Fed funds futures were pricing a 100% probability of a hold at the April 28-29 Federal Open Market Committee meeting, underscoring how little appetite traders had for a policy surprise even as Washington prepared for a leadership handoff.

The bigger issue was not Wednesday’s rate decision itself, but what came next. Powell’s term as chair was set to end on May 15, while his separate term as a Fed governor runs until January 2028. If he stays on the board, it would be the first time a former Fed chair remained on the Fed’s board since 1948, a rare overlap that would leave investors parsing whether his influence survives beyond his chairmanship.

That uncertainty was heightened by the timing in Washington. The Senate was expected to vote around the same time on Kevin Warsh’s confirmation, placing the Fed’s policy meeting and the next chair debate on parallel tracks. Warsh has been nominated both to lead the Board of Governors and, separately, for a 14-year board term beginning February 1, 2026. The Senate Banking Committee was expected to advance his nomination, setting up a broader vote in the full Senate.

For markets, the immediate implication was straightforward: borrowing costs looked set to stay elevated for longer. Inflation remained sticky, with the March consumer price index rising 0.9% from February and 3.3% from a year earlier. The labor market also remained resilient, with March nonfarm payrolls up 178,000 and unemployment at 4.3%. Those numbers supported the view that the Fed had room to stay patient even as pressure from President Donald Trump for faster, deeper cuts continued to build.

The policy backdrop was unusually delicate because the Fed’s own composition was also in flux. Three of the seven current governors were Trump appointees, raising the stakes for how the central bank would manage its independence if a new chair took over amid continued White House pressure. Powell’s legacy was likely to be judged not just on rates, but on his defense of the Fed’s autonomy.

The institution itself is built around a predictable rhythm. The FOMC meets eight times a year, and minutes are released three weeks after each decision. That cadence usually gives investors a clear reading of the policy path. This year, the calendar offered less comfort. Markets had to price monetary policy without knowing whether Powell would remain on the board, whether Warsh would be confirmed, and how a new leadership team might define the Fed’s next phase.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?