Fed holds rates steady, but some borrowing costs stay low

The Fed paused again, but the cheapest money still goes to stellar-credit borrowers and homeowners with equity, not everyone shopping for relief.

The Federal Reserve’s latest pause did not make borrowing broadly affordable. It held its benchmark federal funds target range at 3.5% to 3.75% on June 17, its fourth straight hold of 2026, while updating its economic projections a day later and keeping its focus on maximum employment, stable prices and moderate long-term interest rates.

That matters because the Fed only influences consumer borrowing indirectly. Banks, credit unions and online lenders set their own pricing, so the cheapest deals still depend far more on credit profile, collateral and loan type than on the central bank’s headline decision. The result is a market where one borrower can still find sub-7% financing while another pays close to double digits for the same size loan.

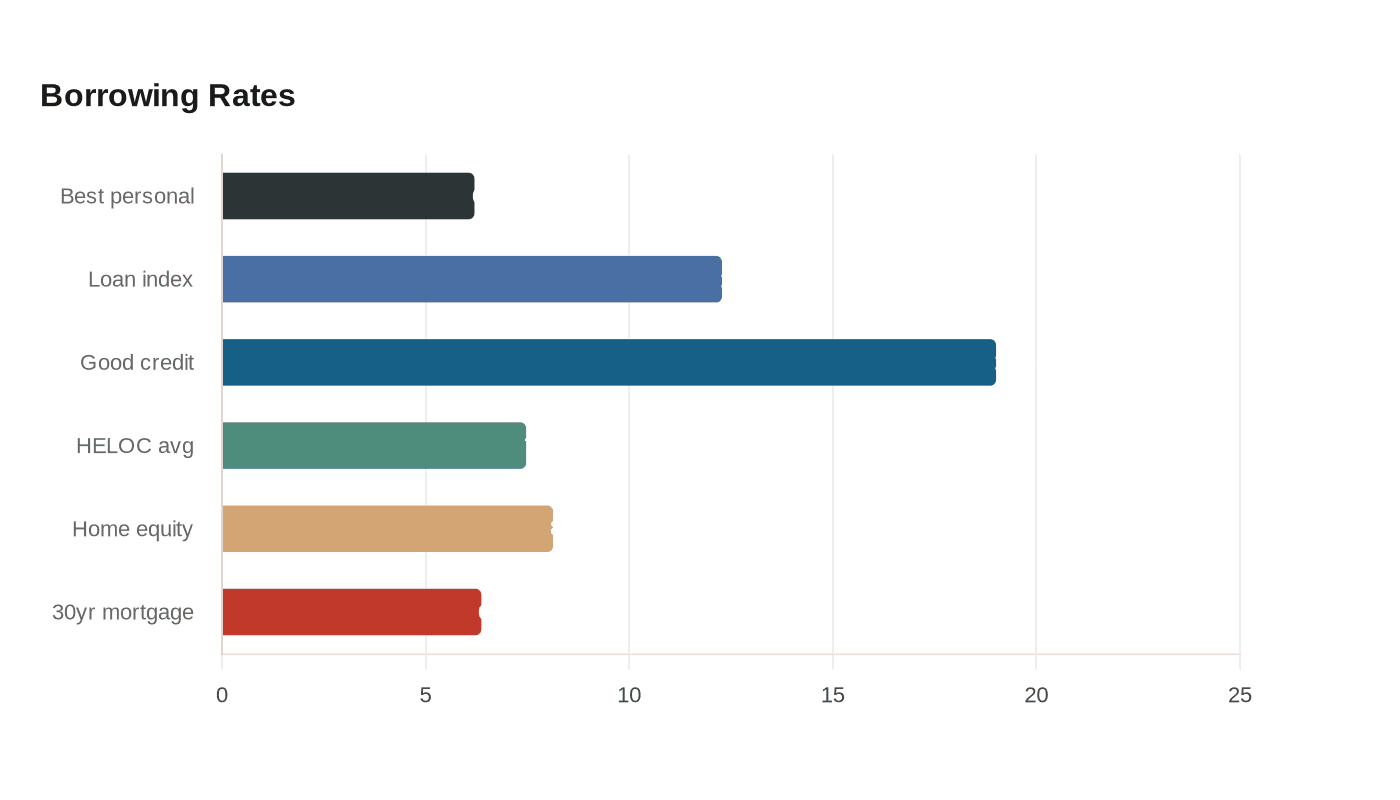

For unsecured borrowing, personal loans remain the lowest-cost option only for the strongest applicants. Bankrate said the best personal loan rates start at 6.20% for borrowers with stellar credit, but its personal-loan index stood at 12.28%. NerdWallet said the average personal loan rate for consumers with good credit was 19.01% on June 1, a reminder that the advertised floor and the typical offer are very different numbers. That spread is exactly where borrowers can get tripped up by focusing on the monthly payment instead of the full cost over the life of the loan.

Homeowners with equity have another path. Bankrate put the national average HELOC rate at 7.47% as of June 17 and the average home equity loan rate at 8.13%. A HELOC works like a reusable line of credit, while a home equity loan usually locks in fixed payments. Bankrate also said home equity loan rates rose modestly this week even as the Fed held steady, showing that these products can move on their own schedule.

Mortgage rates provide a broader benchmark. NerdWallet reported a 30-year fixed mortgage APR of 6.37% on June 18, which sits below the average home equity loan rate and close to the best personal-loan offers available to elite borrowers. On the savings side, certificates of deposit are still yielding around 4%, with NerdWallet putting the top nationally available CD rate at 4.30% APY and Bankrate saying the average five-year CD yield was 1.71% APY.

Bankrate expects CD yields to keep easing in 2026, though still above inflation. For borrowers, the message is sharper: the Fed pause may shape the backdrop, but the cheapest practical borrowing still comes down to credit quality, home equity and careful comparison shopping.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)