Fed's Warsh skips rate projection, opens review of dot plot

Kevin Warsh left his own rate dot blank, cutting the June plot to 18 submissions and signaling a wider review of how the Fed tells markets what comes next.

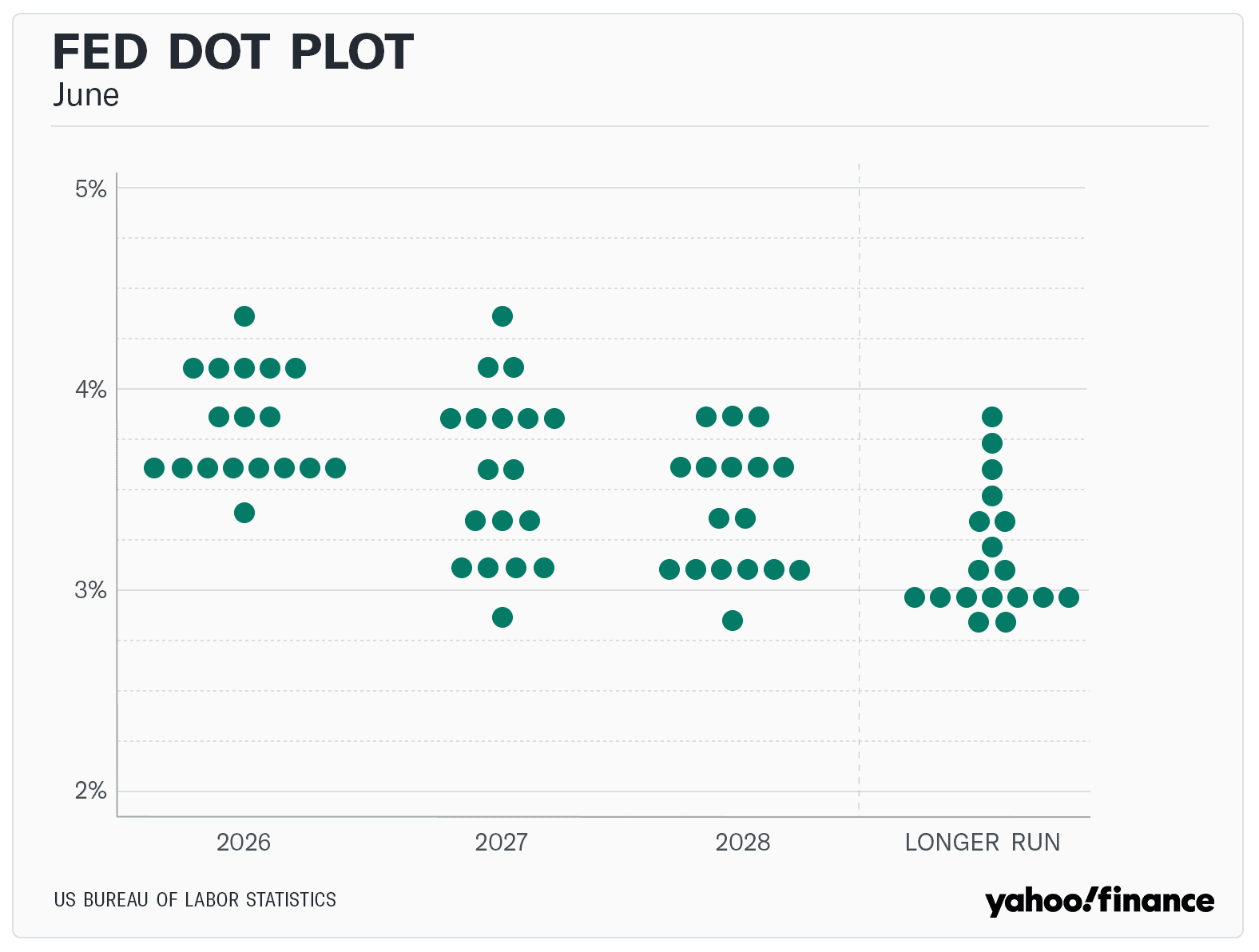

Kevin Warsh made an unusual choice in the Federal Reserve’s latest quarterly projection round: he left his own rate-path dot empty. The June 17 dot plot showed 18 submissions instead of the 19 that would normally be expected, a small omission that carried a larger message about how the central bank should communicate uncertainty, authority and policy intent.

Warsh said he encouraged his colleagues to keep filing their forecasts, but he declined to submit one himself because he disagreed with the way the Summary of Economic Projections is structured. That decision matters because the dot plot has become one of the most closely watched signals in U.S. markets, shaping expectations for bonds, stocks and the dollar even though policymakers know the chart is an imperfect guide to future policy.

The Fed has published the dot plot four times a year since 2012, part of a post-crisis push for greater transparency. A Federal Reserve research paper released in May said the dot plot began in January 2012 and can improve forecast accuracy while also slowing how quickly new information is reflected in market expectations. That tension is now at the center of Warsh’s move: whether the Fed is trying to reduce false precision in its forecasts or opening the door to a less predictable style of leadership.

The latest projection round underscored why the format can stir markets. The Fed kept the federal funds target range at 3.50% to 3.75%, and half of the officials who filed dots expected at least one rate increase in 2026. Six of the nine officials who saw a higher year-end rate thought more than one quarter-point hike would be needed, eight expected no change would be enough to return inflation to 2%, and one projected a cut. In other words, the dot plot still showed a split policy outlook even without Warsh’s own mark on the chart.

Warsh paired the omission with a broader communications review that will involve Fed staff and outside experts. The review will cover five areas: communications, balance-sheet policy, the use and reliability of existing data sources, productivity and jobs in an era of technological change, and inflation frameworks. Warsh said the work would begin within weeks, produce more information in the fall and aim to finish most or all of it by year-end. He also said the policy statement would be shorter and simpler and that the Fed had set aside forward guidance because it no longer fit current conditions. With inflation above the Fed’s 2% goal for more than five years, Warsh’s blank dot looks less like a procedural footnote than an early test of how much clarity the Fed should promise, and how much ambiguity it should preserve.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)