Fenwick & West agrees to pay $54 million in FTX fraud case

Fenwick & West agreed to pay $54 million to settle claims from FTX customers, putting the crypto collapse’s legal fallout on outside counsel as well as executives.

Fenwick & West has agreed to pay $54 million to settle claims that the Silicon Valley law firm helped enable FTX’s collapse, a deal that pushes the crypto exchange’s legal fallout deeper into the ranks of outside advisers.

The preliminary agreement was filed Friday, May 22, 2026, in federal court in Miami and still needs a judge’s approval. The case centers on Fenwick’s role as FTX’s lead outside law firm before the exchange’s 2022 bankruptcy, when customer money disappeared into one of the largest financial frauds in U.S. history.

FTX customers alleged that Fenwick helped craft and implement strategies that facilitated the fraud. Fenwick disputes wrongdoing and said it was not aware of fraud at FTX, while also standing by the integrity of its legal work. The firm employs more than 500 lawyers, and its decision to settle suggests it would rather lock in certainty than risk years of discovery, depositions and trial over its role in the company’s rise and collapse.

Plaintiffs’ lead lawyer, David Boies, told the court the deal was reasonable and would avoid long, complex litigation. The settlement is part of a second wave of agreements in the sprawling FTX litigation, following earlier deals with two former FTX executives. It also arrives as the legal perimeter around the scandal keeps widening beyond Sam Bankman-Fried and the exchange’s inner circle.

That expansion is already visible in a separate lawsuit filed last week in Washington, D.C., where 20 FTX victims from five countries sought at least $525 million from Fenwick and accused the firm of helping conceal the fraud. The overlapping cases underscore a larger question for Silicon Valley, Wall Street and the legal profession: how far outside counsel can go in servicing a fast-moving client before it is drawn into the fraud itself.

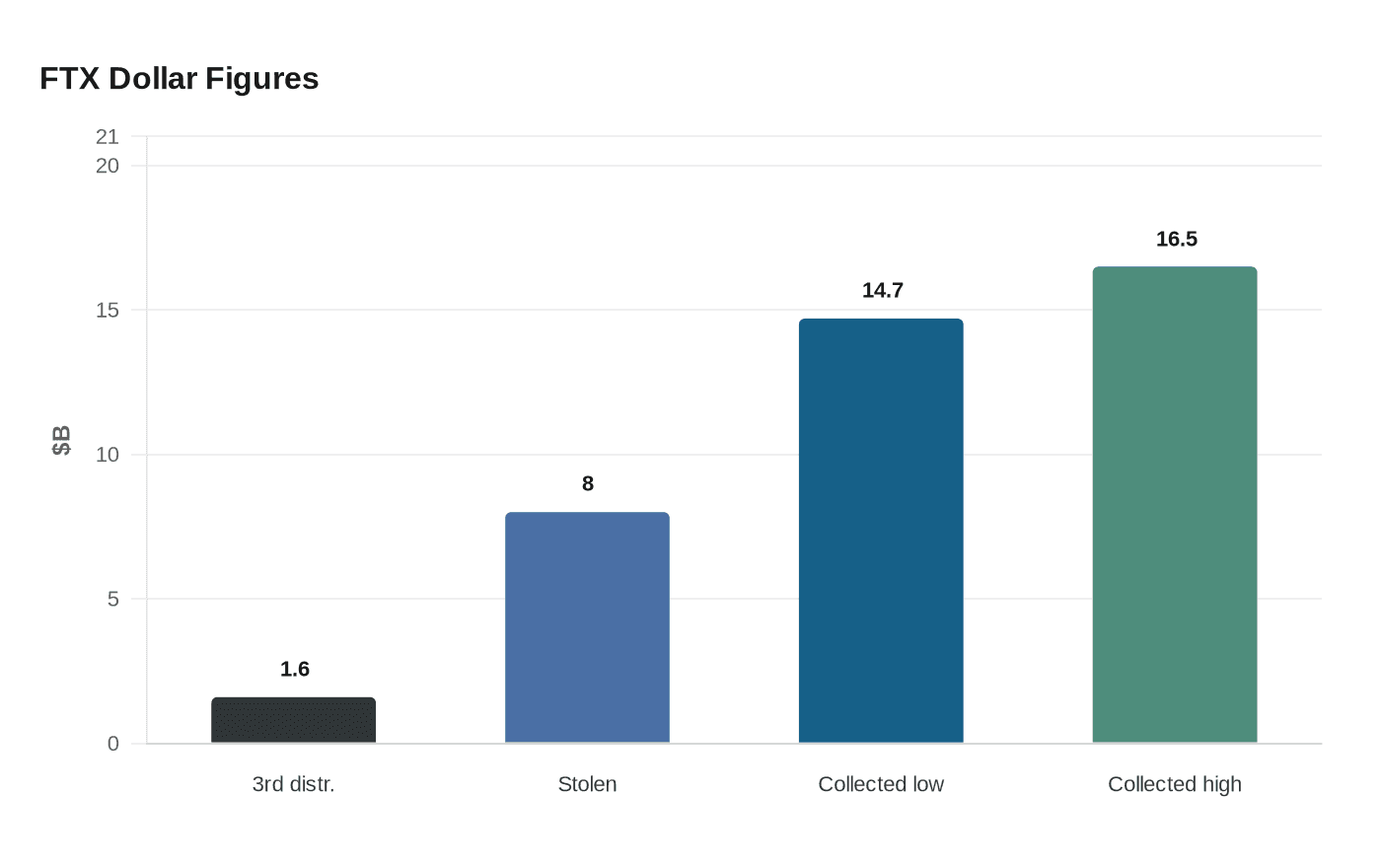

Bankman-Fried was sentenced in 2024 to 25 years in prison for stealing $8 billion from customers, and his conviction is on appeal. His punishment closed one chapter, but the bankruptcy and civil cases have kept producing new ones. In October 2024, a Delaware bankruptcy judge approved FTX’s reorganization plan, and the company said it had collected between $14.7 billion and $16.5 billion in property for creditors. It said 98% of creditors were projected to receive 119% of the amount of their allowed claims.

FTX later announced a third creditor distribution of about $1.6 billion on September 30, 2025, with payouts routed through BitGo, Kraken or Payoneer. Against that backdrop, Fenwick’s $54 million settlement is less about one check than about the broader message: in the post-FTX era, gatekeeper accountability is no longer limited to founders and executives.

Know something we missed? Have a correction or additional information?

Submit a Tip