Former Fed officials urge Warsh to focus on crisis tools, not balance sheet size

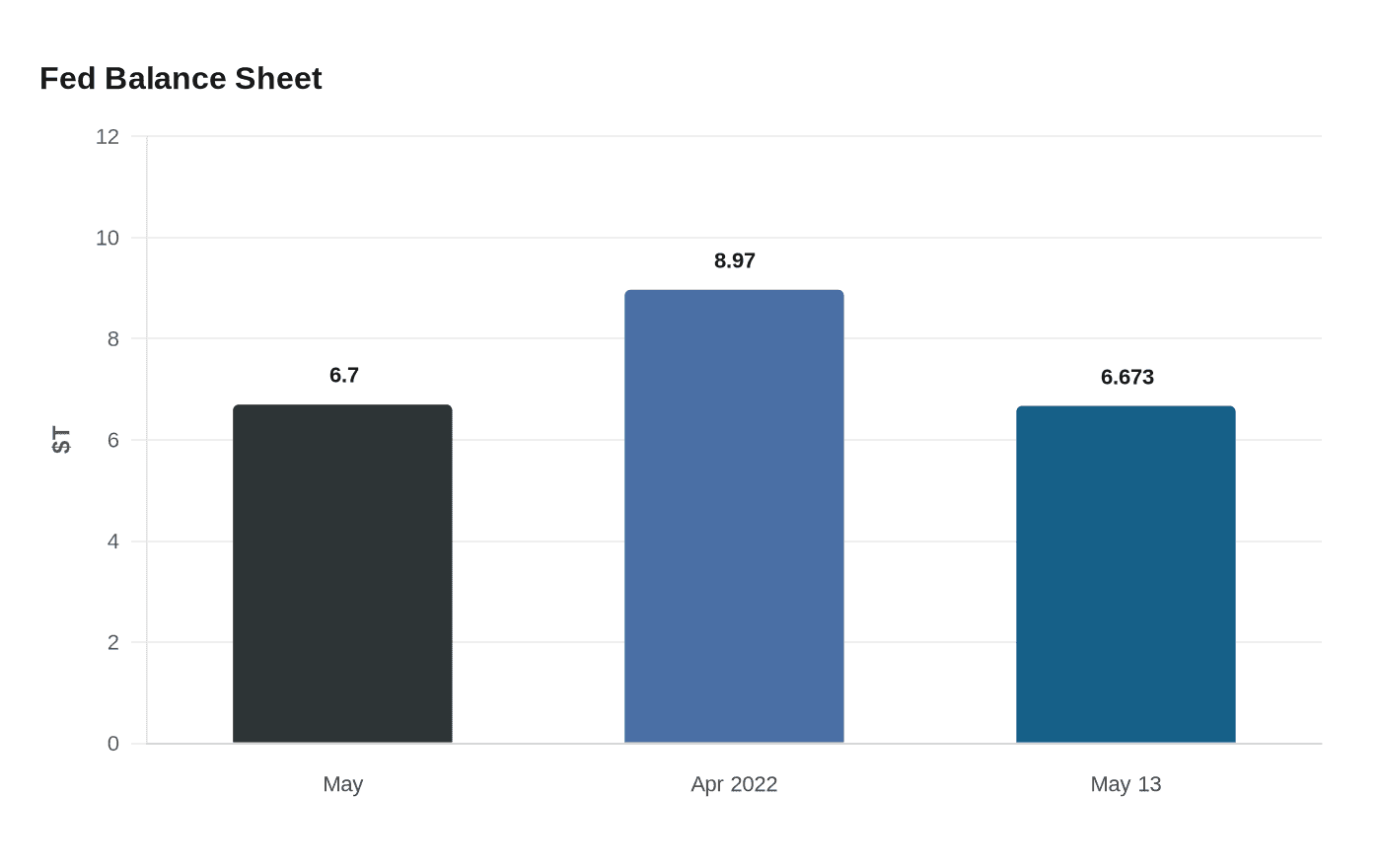

Former Fed officials said Kevin Warsh should debate how the balance sheet works in a crisis, not just whether it is bigger than $6.7 trillion.

The Federal Reserve’s balance sheet may be a political target, but former officials and economists said the more important question is what rules govern its use when the next crisis hits.

At a financial markets conference in Amelia Island, Florida, veterans of the Fed’s crisis-fighting era urged incoming Chair Kevin Warsh to look past the headline number and concentrate on how the central bank deploys its portfolio in an emergency. The Fed’s balance sheet stood at about $6.7 trillion in May, far below its $8.97 trillion peak in April 2022 but still large enough to fuel criticism in Congress and debate inside markets.

Warsh has made shrinking the balance sheet part of his argument for regime change, but former officials said the composition of the holdings matters more than the total. Harvard economist Jeremy Stein, who served as a Fed governor during the quantitative easing era, said the balance sheet’s size had become an optical political football and argued that changing the mix of assets would matter more than simply cutting the total. The point, they said, is not whether the balance sheet is large in the abstract, but whether it remains flexible enough to stabilize markets without blurring the line between monetary policy and market intervention.

That distinction carries practical stakes. The Fed’s H.4.1 release for May 13 showed reserve bank credit at $6.673 trillion and securities held outright at $6.427 trillion, underscoring that most of the portfolio remains in securities rather than emergency lending. A separate Fed report released in May said total assets were about $6.7 trillion, or 21 percent of nominal GDP, as of March 25, and that securities holdings had fallen by $126 billion over the prior two quarters, mostly because of runoff in agency mortgage-backed securities.

Even so, the Fed’s room to shrink further is constrained by reserve demand. In December 2025, the Federal Open Market Committee said reserve balances had declined to ample levels and that it would begin buying shorter-term Treasury securities as needed to maintain an ample supply of reserves. Jerome H. Powell later said those purchases would be solely to keep reserves ample over time. That makes the balance sheet less a simple size question than a management problem tied to how much liquidity banks need and how the Fed signals its intentions to markets.

Warsh’s own history suggests he will have to navigate both the economics and the politics. He served on the Federal Reserve Board from February 24, 2006, to April 2, 2011, supported quantitative easing during the 2007 to 2009 financial crisis, and later became a sharp critic as the program expanded. The Fed said on May 15 that Powell would serve as chair pro tempore until Warsh is sworn in, a handoff Michelle W. Bowman and Stephen I. Miran called unique and unlike any historical precedent. The next chair will inherit not just a balance sheet, but the credibility of the Fed’s crisis playbook.

Know something we missed? Have a correction or additional information?

Submit a Tip