French private-sector activity slips as services PMI hits three-month low

France's private sector unexpectedly contracted in January; services PMI fell to 47.9, signaling renewed downside risks to growth and monetary policy choices.

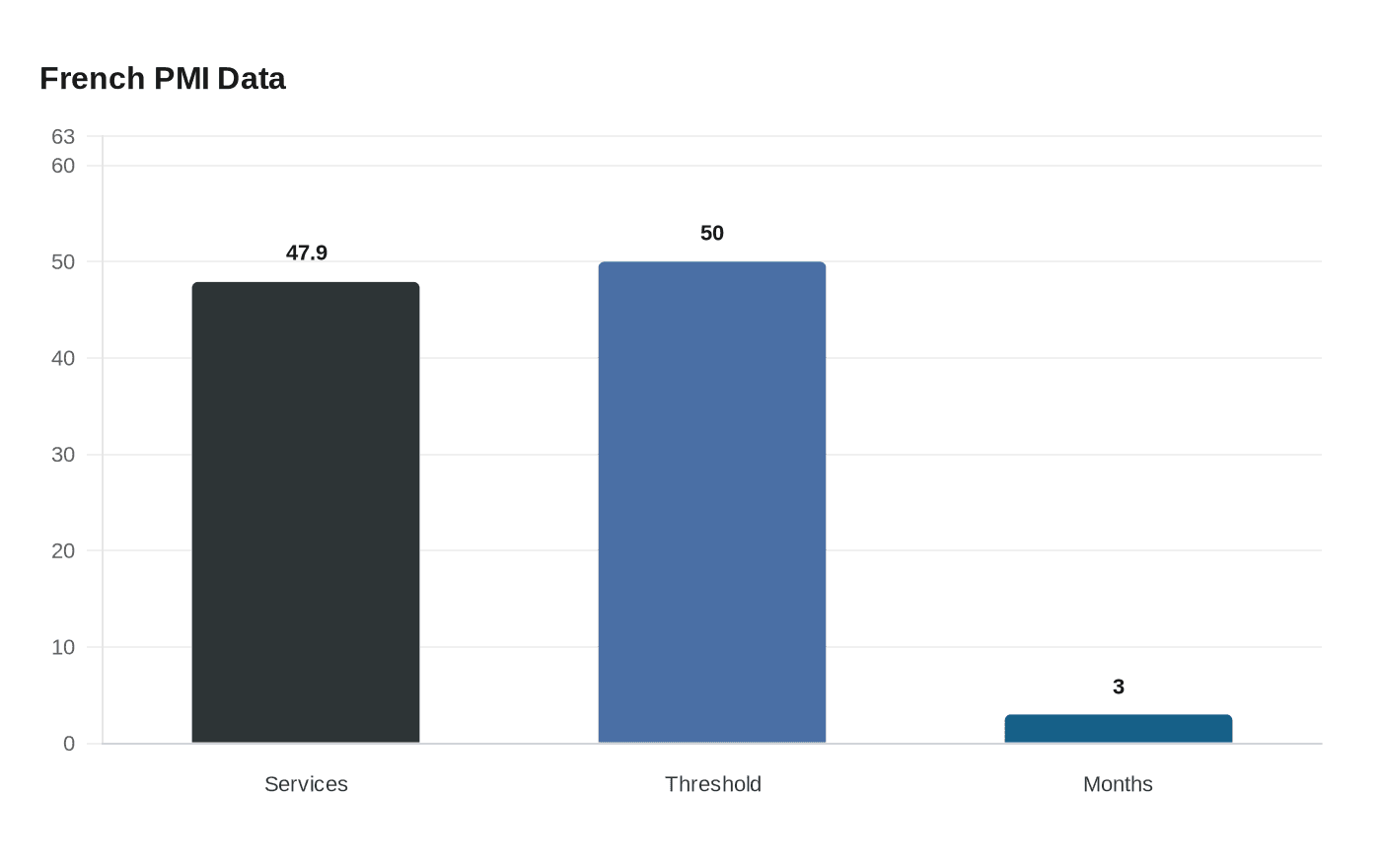

HCOB and S&P Global's flash Purchasing Managers Index readings showed French private-sector activity unexpectedly contracted in January, with the services PMI sliding to 47.9, a three-month low and well below the 50 threshold that separates expansion from contraction. The result underscores a weakening in the domestic demand channel that has previously insulated the economy from external shocks.

A services-sector reading this low suggests that firms are scaling back activity, new business and hiring in key consumption-facing industries. Services account for the bulk of French economic output, so a contraction in that sector carries outsized implications for overall growth momentum. The flash figure implies that any near-term rebound in output will be fragile and dependent on improvements in household spending and business confidence.

The PMI snapshot comes amid a broader, uneasy balance between slowing growth and still-elevated inflation across the euro area. For policymakers at the European Central Bank, a services-sector contraction creates a dilemma. On the one hand, weaker activity tends to ease price pressures, which could argue against further tightening. On the other hand, central bankers must weigh the risk that a premature easing of policy could reignite inflationary dynamics. The January reading therefore complicates the trade-offs facing monetary authorities, particularly as inflation has proven sticky in some service categories in recent years.

For markets, the flash reading increases the probability of a reassessment of growth expectations for France and potentially for the wider eurozone. Investors typically react to lower-than-expected PMI prints by revising down forecasts for GDP and by shifting allocations toward safer assets, which can put downward pressure on government bond yields and the currency. Corporate sector forecasts will also be scrutinized, with analysts likely to reassess revenue and earnings projections for firms exposed to domestic demand.

From a fiscal policy perspective, the contraction may add pressure on the French government to consider demand-support measures, but any stimulus would have to be balanced against fiscal rules and debt sustainability considerations. Policymakers face the question of whether targeted measures to support households and services firms would be more effective than broad-based fiscal loosening, given the concentrated nature of the weakness.

Looking beyond the immediate shock, the PMI reading highlights longer-term structural challenges that have constrained France's growth potential. Heavy reliance on services for employment and output can amplify the impact of swings in consumer spending, while productivity gains in services have historically lagged manufacturing improvements. If services-sector weakness becomes a recurrent theme, it could depress investment and labor market dynamism over the medium term.

Investors and policymakers will be watching subsequent full PMI releases and other high-frequency indicators of consumption and employment for confirmation of January's signal. A single flash reading is not definitive, but a sustained sequence of sub-50 prints in services would strengthen the case for a downward revision to growth forecasts and force a recalibration of both monetary and fiscal strategies.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)