Fusion Funding Booms, But Public Market Strategy Splits Investors

Fusion startups pulled in about $1.6 billion, but investors are now demanding timelines, milestones and real business plans. TAE and General Fusion show how public-market ambitions are splitting the field.

Fusion’s funding boom is still pouring money into the sector, but the easy enthusiasm is giving way to a harder question: which companies can survive when investors want timelines, technical milestones and commercial realism instead of moonshot optimism.

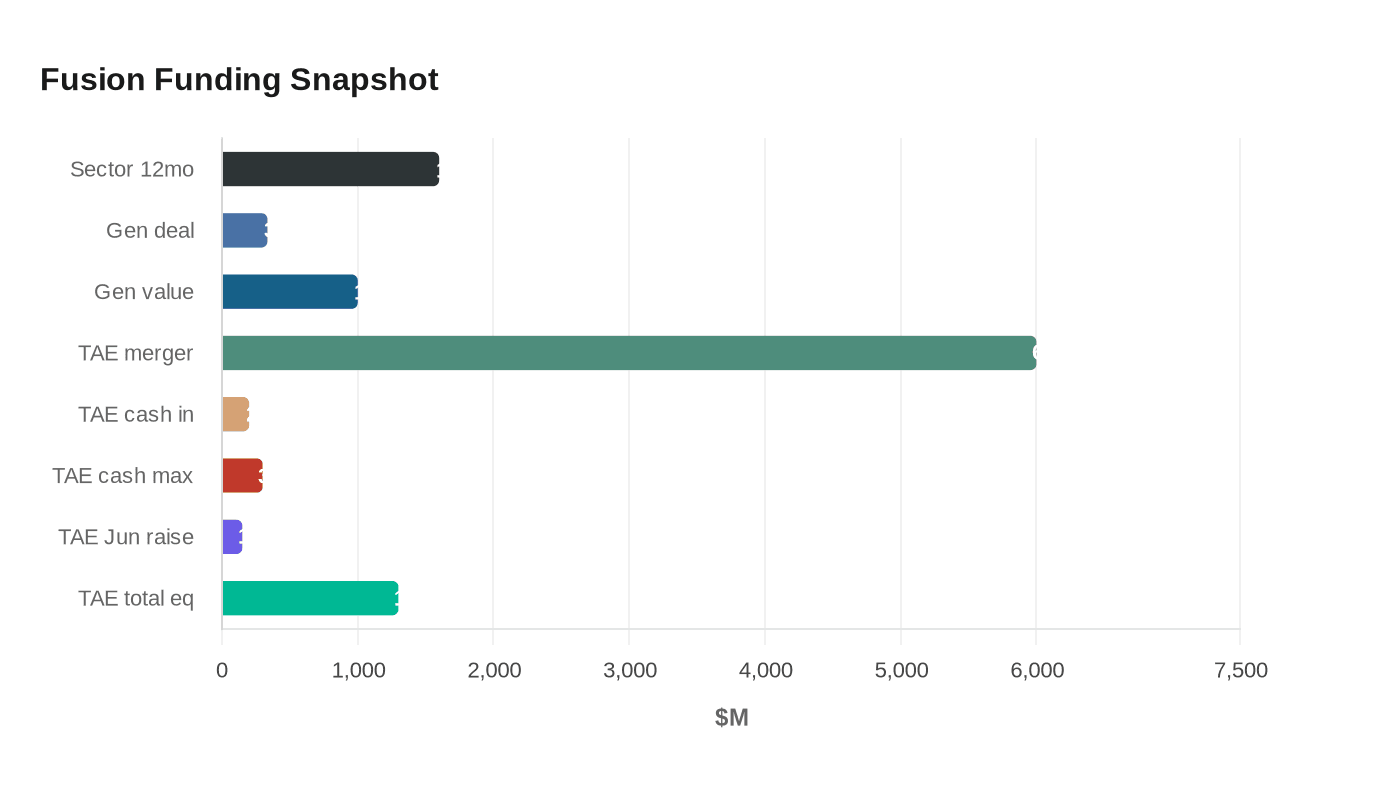

Fusion startups collectively raised about $1.6 billion over the past 12 months, a striking figure for a field that has spent decades trying to move from physics experiment to power source. Yet the mood at Fusion Fest in London was far less unified than the capital totals suggest. Investors and founders are increasingly split over how fast fusion companies should reach public markets, what their business models should look like and whether side ventures strengthen the mission or pull attention from it.

Two companies now sit at the center of that debate. General Fusion announced on January 22, 2026 that it would go public through a reverse merger with Spring Valley Acquisition Corp. III, a deal it said could bring in $335 million and value the combined company at $1 billion. On February 24, 2026, General Fusion filed its Form F-4 publicly, describing that filing as a milestone toward becoming the first publicly traded pure-play fusion company. The company has said its Magnetized Target Fusion approach is aimed at cost-efficient power plants within the next decade.

TAE Technologies has made an even bigger public-market bet. The company announced an all-stock merger with Trump Media & Technology Group valued at more than $6 billion, and said the structure included $200 million already received out of a possible $300 million in cash. TAE said in June 2025 that it raised more than $150 million in a round backed by Chevron Technology Ventures, Google and NEA, and it says it has raised more than $1.3 billion in equity capital since inception.

The concern now is whether these moves arrive too early. Fusion still depends on expensive experiments, heavy equipment and long development cycles, which makes public listings a delicate proposition for companies that have not yet proved commercial generation at scale. General Fusion has already faced layoffs and an earlier public plea for investment, while TAE has spent nearly 30 years building toward utility-scale power. For some investors, that history shows persistence; for others, it underscores how long the road still is.

The policy backdrop is also pushing the industry toward a more serious phase. The U.S. Department of Energy released Fusion Energy Strategy 2024 on June 6, 2024, after the 2022 White House Fusion Summit, with the goal of accelerating commercial viability. The International Atomic Energy Agency’s World Fusion Outlook 2025 has framed fusion as a long-term clean-energy source with major global significance. Together, the public-policy push and the rush toward market listings are forcing a reckoning: fusion is no longer just a scientific promise, but a capital-markets test of which teams can turn breakthrough claims into durable businesses.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?