Germany pension commission proposes higher retirement age, funded pillar

Germany's pension panel urged a higher retirement age and a Swedish-style funded pillar, a test of how far aging democracies can push reform.

Germany’s pension overhaul is no longer a theoretical warning. A commission appointed by Chancellor Friedrich Merz proposed a gradual increase in the retirement age and a new funded pension pillar, a package designed to keep the system stable as the country ages and the ratio of workers to retirees keeps shrinking.

The report, presented on Tuesday, June 23, 2026, called for a state-managed fund modeled on Sweden’s pension system, with mandatory contributions from workers and employers invested in financial assets to help pay future benefits. Reuters-linked summaries said the new pillar could start at 0.5% of gross wages and rise to 2% over time. The commission also recommended ending the option of retiring at 63 without deductions and linking the retirement age more closely to life expectancy.

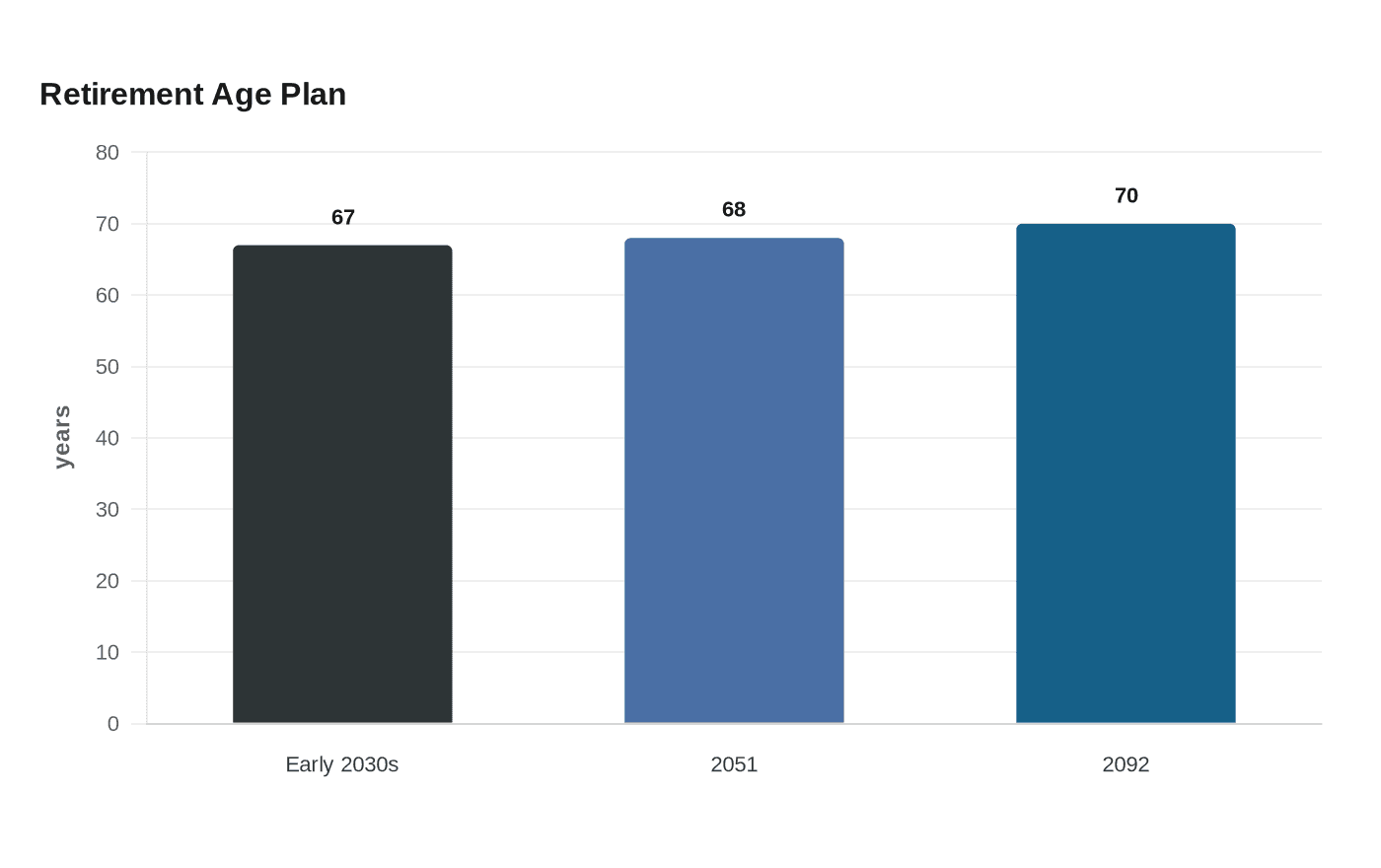

Under the proposal, the increase would begin in 2032, rise to 68 by 2051 and reach 70 by 2092. Germany is already on a legal path toward a retirement age of 67 in the early 2030s, which means the commission’s plan would push the system further and faster over the next seven decades.

The politics are already volatile. Merz has said the goal is to strengthen state pensions while keeping contributions manageable and giving younger workers a more secure future. But the timing is delicate: his coalition is trying to settle tax and welfare reforms before parliament breaks for summer recess, and pensions have become a live test of whether Berlin can absorb demographic pressure without triggering a backlash from retirees, workers and employers.

The stakes are broader than Germany. The European Commission’s 2024 Ageing Report says the first-pillar statutory pension scheme covers about 87% of the population, making the system central to old-age security. OECD data show another fault line: in 2024, women’s average pension in Germany was 26% lower than men’s, underscoring how reform can widen or narrow inequality depending on who bears the cost.

That is why the proposal lands as a stress test for aging democracies. It asks how far a wealthy country can raise retirement ages and shift part of the burden into market-based funding before political resistance hardens. In the United States, where Social Security faces similar demographic strain, the German debate offers a blunt lesson: reform is not just about solvency, but about how risk is shared between generations, and whether workers are being asked to finance a future that also exposes them to market swings.

The backlash is already visible. The Deutscher Gewerkschaftsbund has rejected a pension age of 70, arguing that older workers are often laid off first and hired last. Employers, by contrast, have long pushed for changes that stabilize contribution rates and expand occupational and private savings. The federal government is also advancing other pension measures, including an early-retirement pension, an active pension and stronger company pensions, while a separate DGB-led commission is working on its own retirement concept due in summer 2026.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip