Gilead raises sales outlook as HIV drug Yeztugo beats forecasts

Yeztugo topped sales forecasts and lifted Gilead’s outlook, but acquisition charges flipped 2026 guidance to an adjusted loss and sent the stock lower.

Gilead Sciences is leaning on its HIV franchise to finance expansion beyond it. Strong first-quarter sales from Yeztugo and Descovy let the Foster City company lift its 2026 revenue outlook, but the same quarter also showed how costly its acquisition spree has become: adjusted earnings are now expected to swing to a loss.

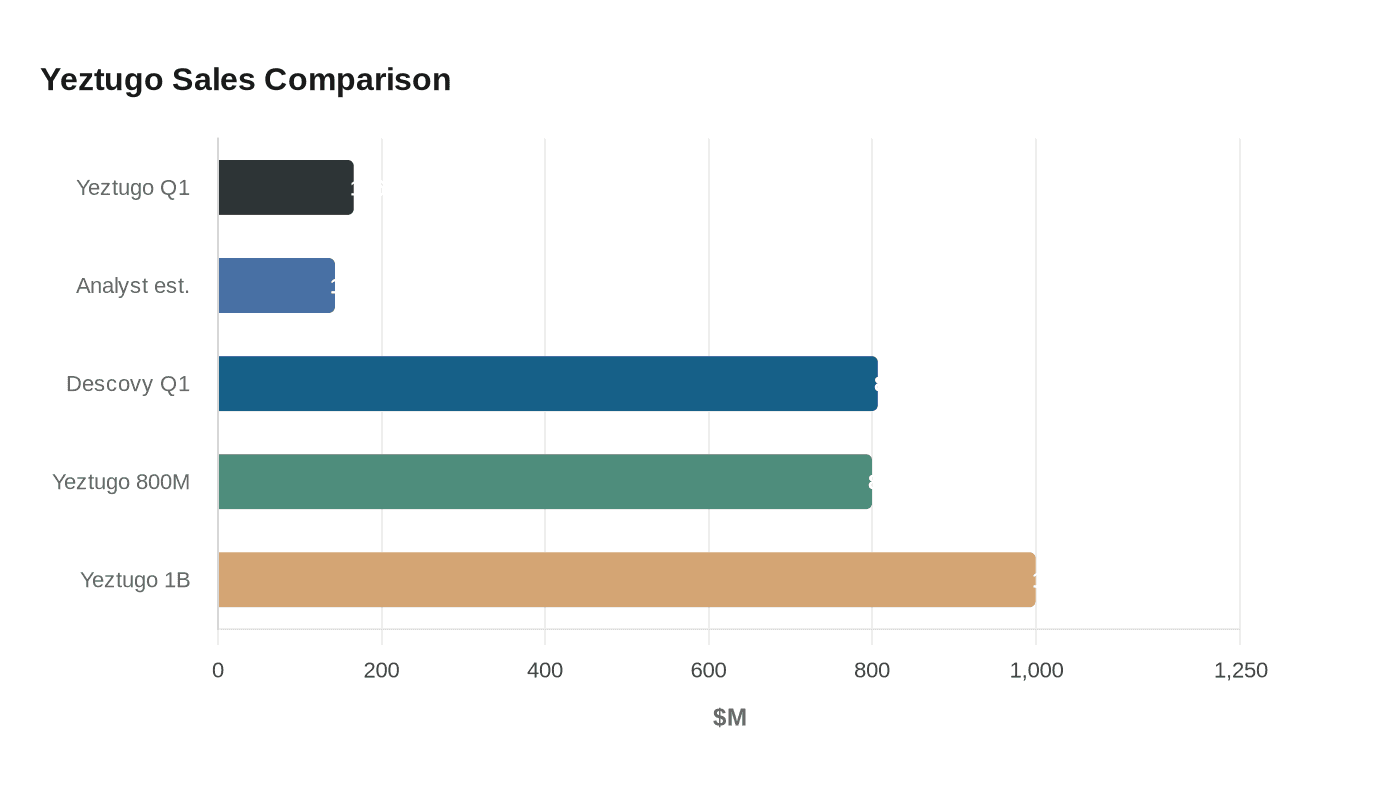

Yeztugo, the twice-yearly HIV prevention option approved by the U.S. Food and Drug Administration in June 2025, generated $166 million in sales in the quarter, ahead of the $143 million analysts had expected. Gilead lifted its 2026 Yeztugo sales forecast to $1 billion from $800 million. Descovy, another HIV pill used to prevent infection, added to the momentum, with sales up 38% to $807 million. Together, the products helped Gilead raise its overall 2026 sales outlook by $400 million to a range of $30 billion to $30.4 billion.

That top-line strength, however, did not translate into a better profit picture. Gilead now expects an adjusted loss of $1.05 to $0.65 per share for 2026, reversing an earlier forecast for earnings of $8.45 to $8.85 per share. The company said charges and financing costs tied to recent deals drove the change, including acquisitions of Arcellx, Ouro Medicines and Tubulis. It completed the Arcellx purchase in April and struck definitive agreements for Ouro Medicines in March and Tubulis in April, moves aimed at broadening its cell therapy, inflammation and oncology pipelines.

The strategy reflects a familiar big-pharma trade-off: a mature cash-generating core can fund the search for the next growth engine, but the balance sheet and earnings may feel the strain long before new drugs pay off. Gilead said its HIV portfolio produced $20.8 billion in sales in 2025, up 6% from 2024, giving the company room to invest. Still, Yeztugo’s launch has faced insurance coverage gaps and some patient reluctance around an injectable regimen, even as prescriptions have risen. Gilead has said a once-yearly version could reach the market as soon as 2028, and it has also expanded access efforts with PEPFAR and The Global Fund to reach up to an additional 1 million people in high-incidence, resource-limited countries.

Investors focused first on the earnings reset, and Gilead shares fell after the outlook change. For now, the HIV franchise is doing the heavy lifting, but the acquisition burden shows how expensive it is to buy a future that still has to prove itself.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?