Peloton swings to profit, raises forecast as turnaround gains traction

Peloton returned to profit on stronger sales and pricing, but paid subscribers still slipped to 2.66 million as the company leans on higher fees.

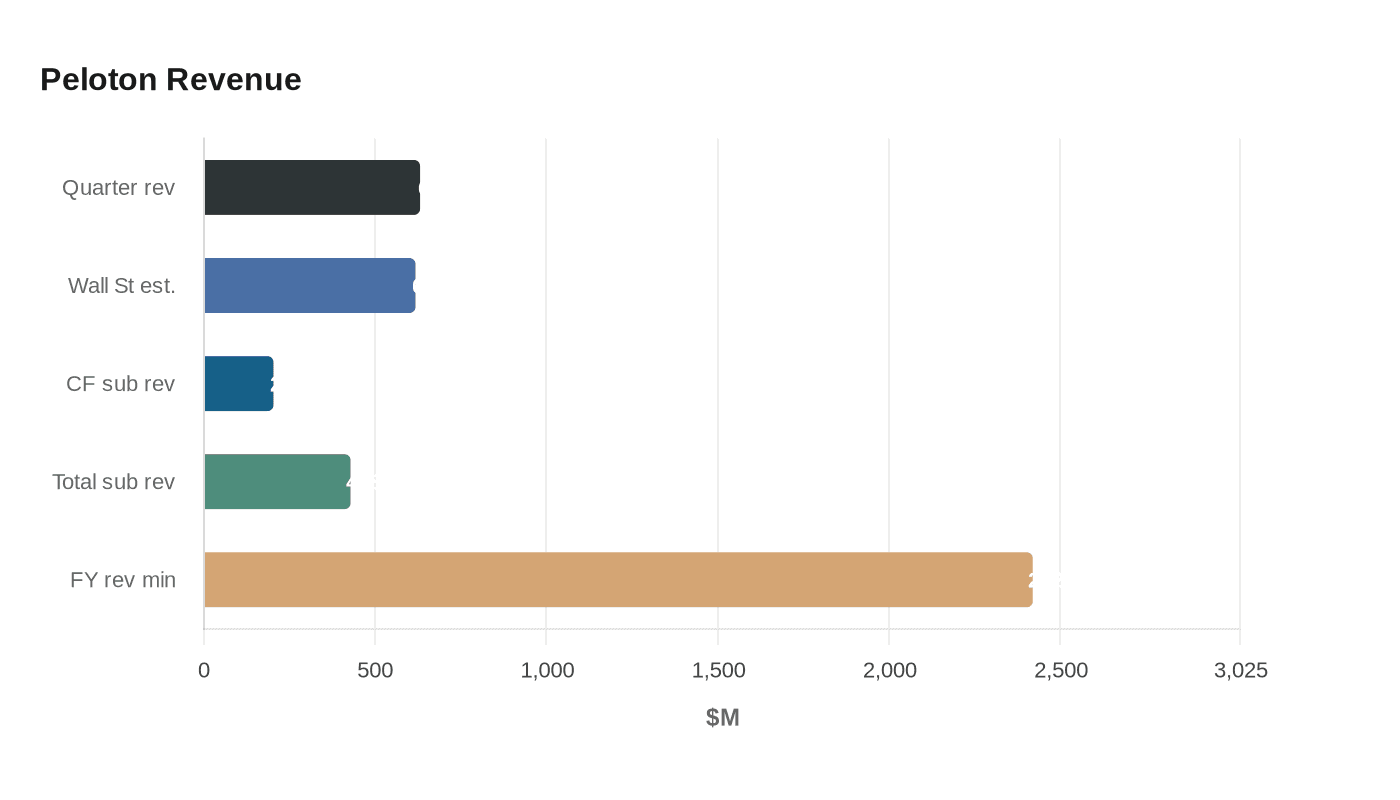

Peloton’s latest quarter offered the clearest evidence yet that its turnaround is taking hold, but it also showed how dependent that progress remains on pricing power and tighter execution rather than a renewed surge in membership growth. The connected-fitness company swung to net income of $26.4 million, or 6 cents a share, from a loss of $47.7 million a year earlier, and revenue reached $630.9 million, topping Wall Street expectations of $617.6 million.

Investors rewarded the results. Peloton shares rose about 8% by the close after climbing as much as 13% intraday, a sharp reaction to a business that is once again generating profit and more cash. Adjusted free cash flow improved by nearly 60%, reinforcing the idea that management’s discipline on costs is starting to matter as much as top-line growth.

The stronger quarter came with a more complicated message underneath. Paid connected-fitness subscribers fell to 2.66 million, down from a year earlier, showing that the company is still struggling to expand its installed base at the pace it once did. Connected-fitness subscription revenue came in at $202.9 million, above estimates but below the $205.5 million posted a year earlier, while total subscription revenue rose 2% to $428 million. Peloton said stronger equipment sales and subscription revenue helped the quarter, with management also leaning on a new pricing strategy.

That pricing strategy is now central to the argument for the business. Chief executive Peter Stern said higher subscription prices were a value-driven move, not a simple markup, and Peloton has framed the change as a way to strengthen revenue while preserving the brand. In February, the company said the membership price increases announced on October 1 had produced better-than-expected churn, even as gross additions softened. That trade-off remains at the center of the turnaround: higher recurring revenue can improve the model, but only if customer retention stays intact.

Peloton raised the low end of its full-year revenue outlook to $2.42 billion from a lower prior floor, suggesting management sees enough momentum to expect a better finish to the year. Still, the broader question is whether the company is building durable expansion or simply squeezing more revenue from a loyal but largely capped audience. Peloton has been selling more equipment to existing members and pushing products such as its Cross Training Series, the Pro Series for commercial fitness facilities and Peloton IQ, all aimed at keeping users inside the ecosystem longer. For now, the numbers suggest stabilization. The harder test is whether that stability can become sustainable growth.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)