HELOC Rates Drop Below 8%, Offering Homeowners a Rare Borrowing Opportunity

HELOC rates have dropped below 8% for the first time since 2023, creating a rare borrowing window for homeowners sitting on record levels of accumulated equity.

For the first time since 2023, the national average HELOC rate has slipped below 8%, landing at approximately 7.20% according to data analytics firm Curinos. That single number carries significant weight for millions of American homeowners who have been watching borrowing costs from the sidelines. With the Federal Reserve having cut rates multiple times since late 2024, additional cuts projected through 2026, and average home equity sitting near $300,000 per borrower, the conditions for tapping a home equity line of credit are as favorable as they have been in years.

Rates at their most competitive level since 2023

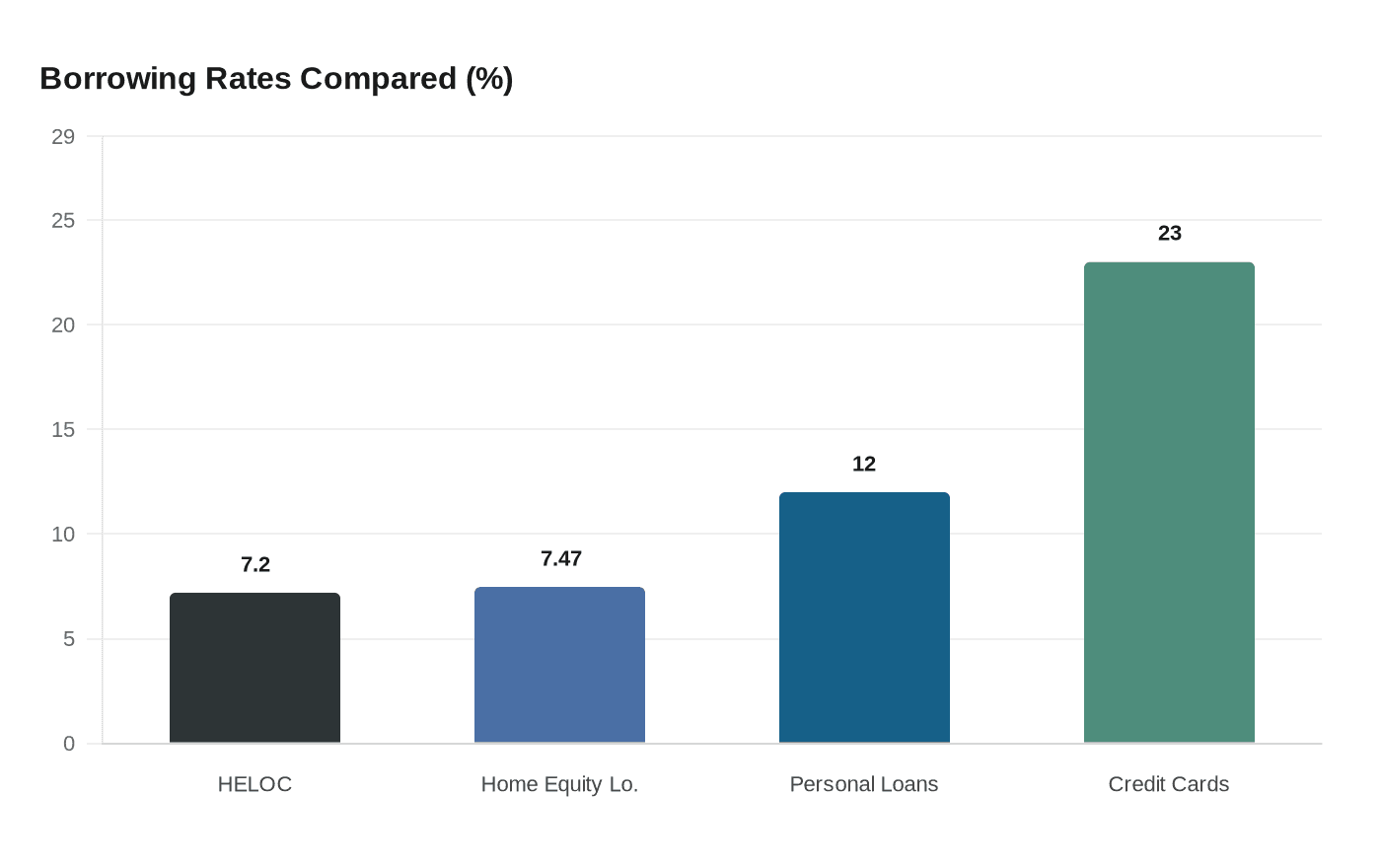

The milestone arrived in early April 2025, when HELOC rates fell below 8% for the first time in roughly two years, according to CBS News. The national average monthly adjustable HELOC rate now sits at approximately 7.20%, while the average fixed rate on a comparable home equity loan stands at 7.47%, both figures sourced from Curinos based on applicants with a minimum credit score of 780 and a maximum combined loan-to-value ratio of 70%.

HELOC rates are priced off the prime rate, currently at 6.75%, plus a lender margin. When a lender adds a typical margin of 0.75 percentage points, the resulting rate lands around 7.50% — a figure that looks dramatically different from alternatives available to most borrowers. Personal loan rates have been frozen near 12% for months. Credit card rates only recently began declining, and only from a record high of 23%. Against that backdrop, a 7.20% HELOC rate is not just competitive; it represents one of the most cost-effective borrowing tools available to qualifying homeowners right now.

For context, borrowing $50,000 at 7.25% on a HELOC generates a monthly interest payment of approximately $302 during the draw period. Critically, borrowers only pay interest on the amount they actually draw, not the full approved credit line, which keeps carrying costs flexible throughout the life of the product.

Variable structure: a feature, not a flaw, in a falling-rate environment

One of the most misunderstood aspects of a HELOC is its variable interest rate. In a rising-rate environment, that variability feels like a liability. In the current climate, it is one of the product's most valuable features.

The Federal Reserve cut rates three times in 2024, in September, November, and December, totaling 100 basis points, according to The Truth About Mortgage. It then cut an additional 75 basis points in 2025. Federal Reserve projections and economic forecasts analyzed by MidFlorida Credit Union suggest further reductions of 0.50 to 0.75 percentage points over the 2025-2026 period. Karen Mayfield, national head of originations at Multiply Mortgage, expects one to two additional cuts in the second half of 2025 alone: "I think we'll see one to two cuts this year…and that they would be the second half of this year."

Because HELOCs are tied to the prime rate, those future reductions pass through to borrowers automatically, typically within 30 to 60 days of each Federal Reserve decision. There is no need to refinance, pay new closing costs, or renegotiate terms. As Shayowitz, a mortgage expert cited by CBS News, put it: "If somebody took out a home equity line of credit today, and there was a 50 basis point cut in September, starting October 1st, they would get the benefit of the lower interest rate."

This automatic adjustment mechanism puts the HELOC in stark contrast to a fixed-rate home equity loan, which locks in a rate at origination regardless of what the Fed does next. For borrowers who believe rates will continue declining through 2026, the HELOC's variable structure represents a meaningful long-term financial advantage with no administrative friction attached.

Record equity levels and a tax advantage fixed alternatives cannot match

The rate environment is one part of the story. The equity backdrop is equally striking.

According to Selma Hepp, chief economist at Cotality, the average U.S. homeowner has approximately $295,000 in accumulated home equity. A separate CBS News analysis puts that figure comfortably over $300,000. These are record levels, and they give qualifying homeowners substantial borrowing capacity they can access without touching their primary mortgage.

That last point matters more than it might initially seem. First-mortgage rates are currently averaging close to 7% on a 30-year fixed loan. Homeowners who locked in rates of 3% or 4% in prior years would effectively surrender that rate advantage if they pursued a cash-out refinance. A HELOC sidesteps the problem entirely, drawing on home equity as a separate credit facility and leaving the first mortgage fully intact.

There is also a tax dimension worth factoring in. HELOC interest is tax-deductible when the line of credit is used for IRS-eligible home repairs and renovations, an advantage that personal loans and credit cards simply do not carry. For homeowners directing borrowed funds toward qualifying improvements, the effective cost of the HELOC drops further once that deduction is applied to annual tax calculations.

What borrowers need to know before applying

A HELOC is a 30-year product in practice: a 10-year draw period during which borrowers can access funds as needed, followed by a 20-year repayment period. Fixed-rate HELOC options exist with select lenders for borrowers who prefer payment certainty, though the variable-rate version remains the more widely available structure.

Eligibility generally requires a credit score of at least 620 (with 680 historically considered the standard threshold), a 15% to 20% equity stake in the home, and verifiable steady income. Because the home serves as collateral, missed payments carry the serious risk of foreclosure, making careful budgeting before drawing on a line of credit an essential first step, not an afterthought.

The combination of sub-8% rates, a structure that automatically benefits from future Federal Reserve cuts, record levels of accessible equity, and the tax deductibility of qualifying uses positions the HELOC as one of the more strategically useful financial instruments available in the current environment. Whether that window stays open will depend on how quickly broader economic conditions shift; the data right now, however, points in one direction.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)