High-yield savings accounts still offer 4% to 5% APY returns

Savers can still earn 4% to 5% APY, but the real gain depends on caps, deposit rules, and how taxes and inflation trim the headline rate.

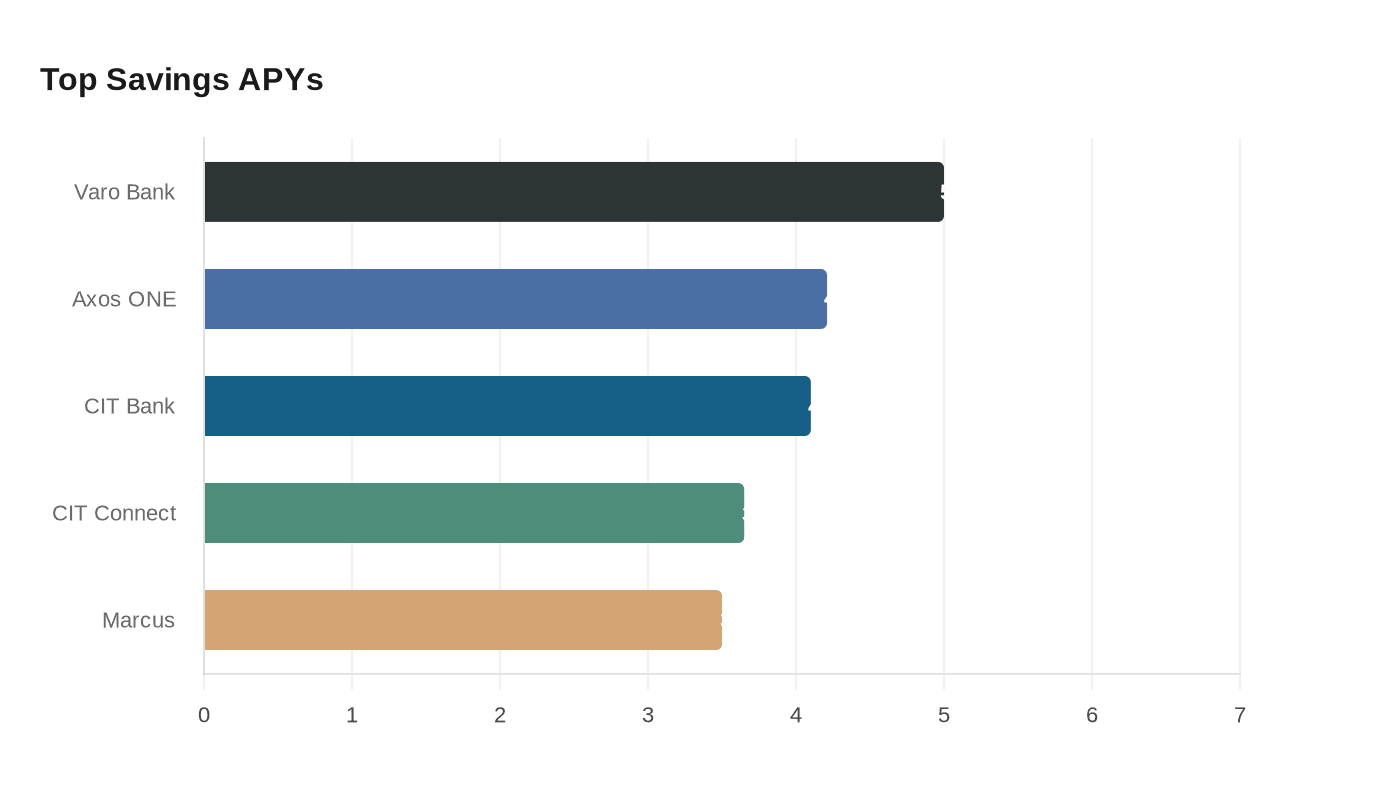

What your cash can earn right now

High-yield savings accounts still let cash earn 4% to 5% APY, and that spread matters again for anyone with idle money sitting in a low-paying bank account. Bankrate’s top advertised rate is 4.10% from CIT Bank, while NerdWallet’s headline rate is 5.00% from Varo Bank on balances up to $5,000 when qualifying deposit requirements are met. DepositAccounts also shows competitive offers such as Axos ONE Savings up to 4.21% APY, Marcus by Goldman Sachs at 3.50% APY, and CIT Bank Savings Connect at 3.65% APY with a $100 minimum deposit.

The practical difference shows up fast in dollar terms. A $5,000 balance at 4.10% APY earns about $205 a year, versus roughly $30.50 at Bankrate’s 0.61% national average and $19 at NerdWallet’s 0.38% average. On $10,000, the same 4.10% rate produces about $410 a year, or roughly $349 more than the 0.61% average and $372 more than the 0.38% average. On $50,000, the spread becomes about $1,745 a year versus the 0.61% average.

Why these rates are still elevated

The broader rate backdrop helps explain why savings yields remain appealing even after the Fed’s tightening cycle. The Federal Reserve Board’s H.15 data for May 15, 2026 shows the effective federal funds rate at 3.63%, which is still far above the near-zero era that shaped deposit pricing for years. The FDIC says the national rate cap for non-maturity deposits is the higher of the national rate plus 75 basis points or the federal funds rate plus 75 basis points, and that a less-than-well-capitalized institution may use a local rate cap for deposits gathered from within its local market area.

That structure matters because the best retail yields are usually coming from online banks and credit unions that are competing aggressively for deposits. Many of the strongest accounts also keep fees down, with no monthly maintenance charge and low or no minimum opening deposit requirements, and they are typically held at FDIC-insured banks or NCUA-insured credit unions. DepositAccounts’ best-online-savings list, for example, highlights several no-fee options, including Marcus by Goldman Sachs at $0 minimum deposit and Axos Bank’s up-to-4.21% offer with no monthly maintenance, minimum balance, account opening, or overdraft fees.

The fine print behind the headline APY

The biggest tradeoff is that the top rate is often not the rate on every dollar you hold. Varo’s 5.00% APY applies only up to $5,000 and requires at least $1,000 in total qualifying direct deposits, plus a positive combined checking and savings balance at month end. DepositAccounts shows a similar theme elsewhere, with CIT Bank Savings Connect paying 3.65% APY but requiring a $100 minimum deposit, while Marcus by Goldman Sachs offers 3.50% APY with a $0 minimum deposit.

That means the best account is not always the one with the single highest APY. If your cash balance is small and you can meet the activity rules, a tiered offer like Varo can be very attractive. If you want a larger balance parked without direct-deposit hurdles, a flat-rate account such as Marcus or a higher-balance option like Axos may be simpler, even if the headline number is a little lower.

Do these yields actually beat inflation after taxes?

The answer depends on two separate drags: taxes and inflation. APY is a pre-tax return, so a saver in a 22% federal tax bracket would see a 4.10% APY fall to about 3.20% after federal tax, and a 5.00% APY fall to about 3.90%. That is still a meaningful return for cash, but it is a lot thinner once taxes are taken out.

Inflation can narrow the real gain further. If prices rise faster than your after-tax yield, your purchasing power still falls even though the account is paying a strong nominal rate. That is why the headline APY is only part of the story: the more relevant number is the return you keep after tax and after the account’s balance caps, deposit rules, and tiering are applied.

What to check before moving your money

The best high-yield account for you is usually the one that fits your cash flow, not just the one with the flashiest APY. Before you move money, check whether the offer requires direct deposit, e-statements, or a minimum balance, and whether the best rate applies only to a capped slice of your savings. Also confirm the account is FDIC- or NCUA-insured and note whether the yield changes after a promotional period ends.

For readers parking emergency funds or short-term savings, the message is straightforward: cash still has a real return if you place it carefully. With national averages at 0.61% and 0.38% while strong online offers remain around 4% to 5%, the upside is large enough to matter, but only if the account’s rules match the way you actually save.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)