High-yield savings and CDs nearly match on $50,000 returns

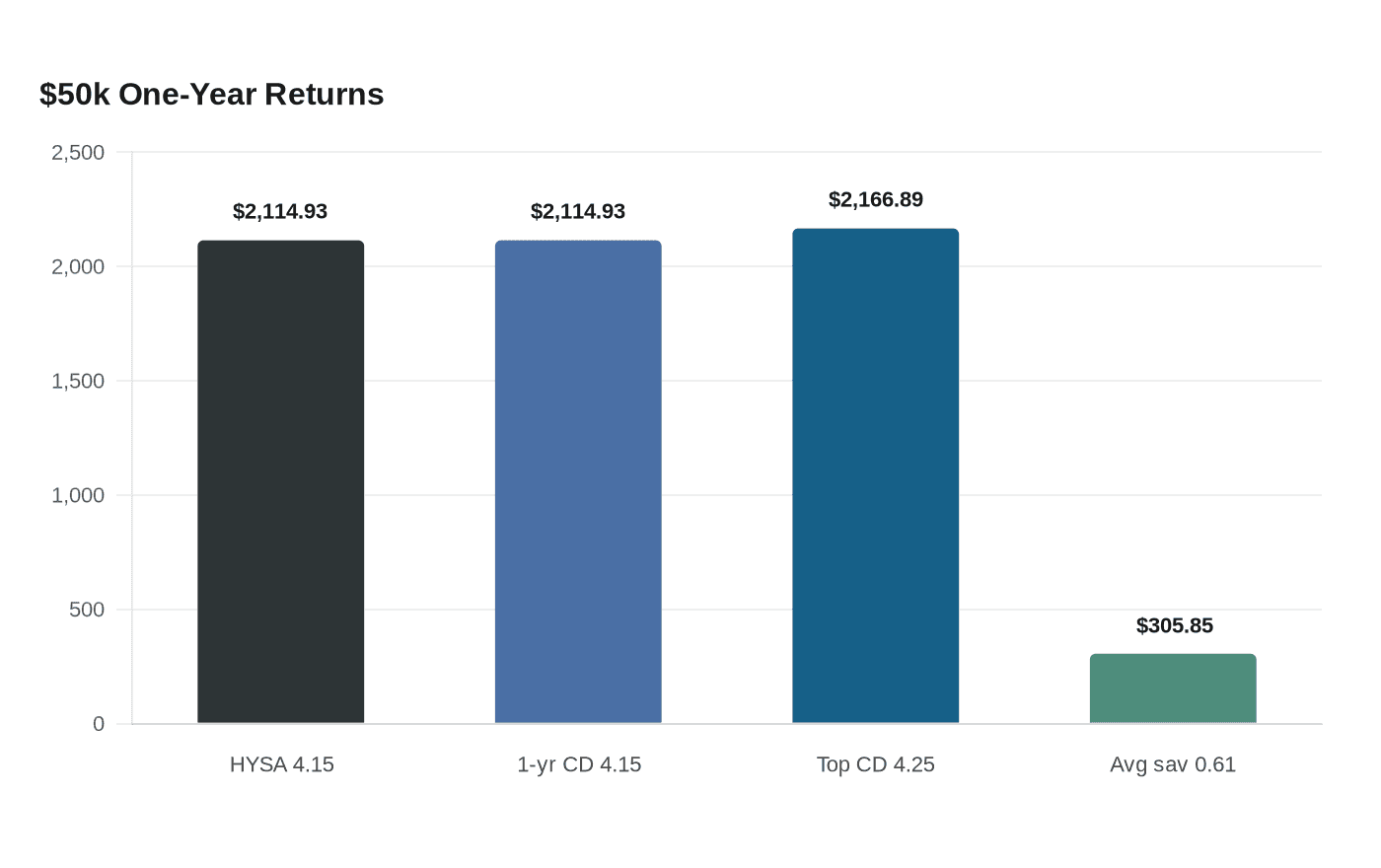

A $50,000 balance earns $2,114.93 in a top savings account and $2,166.89 in a top CD, but liquidity and rate bets still decide the winner.

A $50,000 deposit now produces nearly the same one-year return in a top high-yield savings account as in the best CDs, but the real choice is not the payout. It is whether savers want to keep cash accessible or lock in a rate while the Federal Reserve’s benchmark remains elevated.

Bankrate’s June 2026 rankings put the top high-yield savings rate at 4.15% APY from Forbright Bank, matching its top one-year CD rate from Popular Direct and sitting just below the 4.25% APY top CD tracked by Suncoast Credit Union. On a $50,000 balance compounded monthly, 4.15% APY would earn about $2,114.93 over a year, while 4.25% APY would earn about $2,166.89. That 20-basis-point spread amounts to only about $51.96 over 12 months, a narrow gap for anyone weighing whether to give up flexibility.

The broader contrast is with ordinary savings accounts. Bankrate says the national average high-yield savings rate is 0.61% APY, and the same $50,000 would earn only about $305.85 in a year at that level. The difference between 4.15% APY and 0.61% APY is about $1,809.07, which shows why the best online savings offers still matter even when they barely trail the top CDs.

The policy backdrop helps explain why deposit rates remain high. The Federal Reserve Board’s H.15 release showed the federal funds effective rate at 3.63% on June 15, 2026, a level that keeps pressure on banks and credit unions to compete for deposits. FDIC’s national rates framework, which weights rates by domestic deposit share, also underscores how much the market still depends on institutions willing to pay up for customer balances.

For savers, the decision comes down to scenario planning. A CD wins if the goal is guaranteed growth for a set term and the expectation is that rates will fall over the next year, because the yield is locked in now. A high-yield savings account wins if cash might be needed sooner or if the outlook is for rates to rise, because the rate can adjust more quickly and the money stays liquid.

That liquidity comes with a tradeoff. Bankrate notes that early withdrawals from CDs can trigger penalties, so the extra few dollars of yield can disappear if the money has to come out before maturity. In today’s rate environment, the difference between the best savings account and the best short-term CD is small enough that access to cash may matter as much as the headline APY.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip