What a $50,000 CD earns as rates stay elevated

A $50,000 CD can still generate solid income, but the premium over flexible cash is slim. For many savers, the bigger call is access, not yield.

A $50,000 CD can still produce real cash, but the edge over flexible savings is narrower than many savers assume. Bankrate’s best one-year CD rate is 4.15% APY, which works out to about $2,075 a year before taxes on a $50,000 balance, while its broader tracker tops out at 4.25% APY and its best high-yield savings account is also at 4.15% APY. That makes the decision less about chasing yield and more about whether locking up cash is worth giving up access.

What $50,000 earns in a CD right now

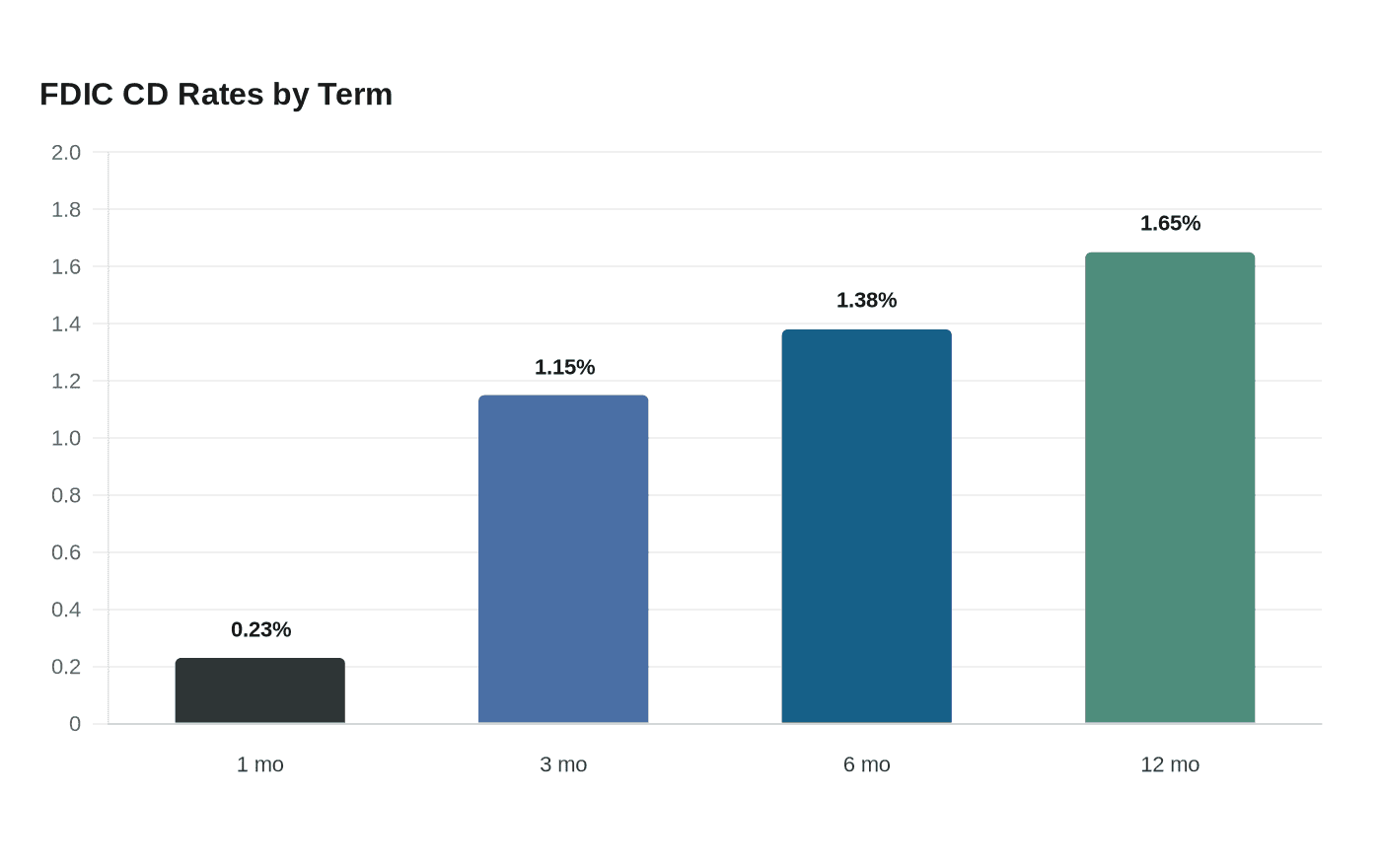

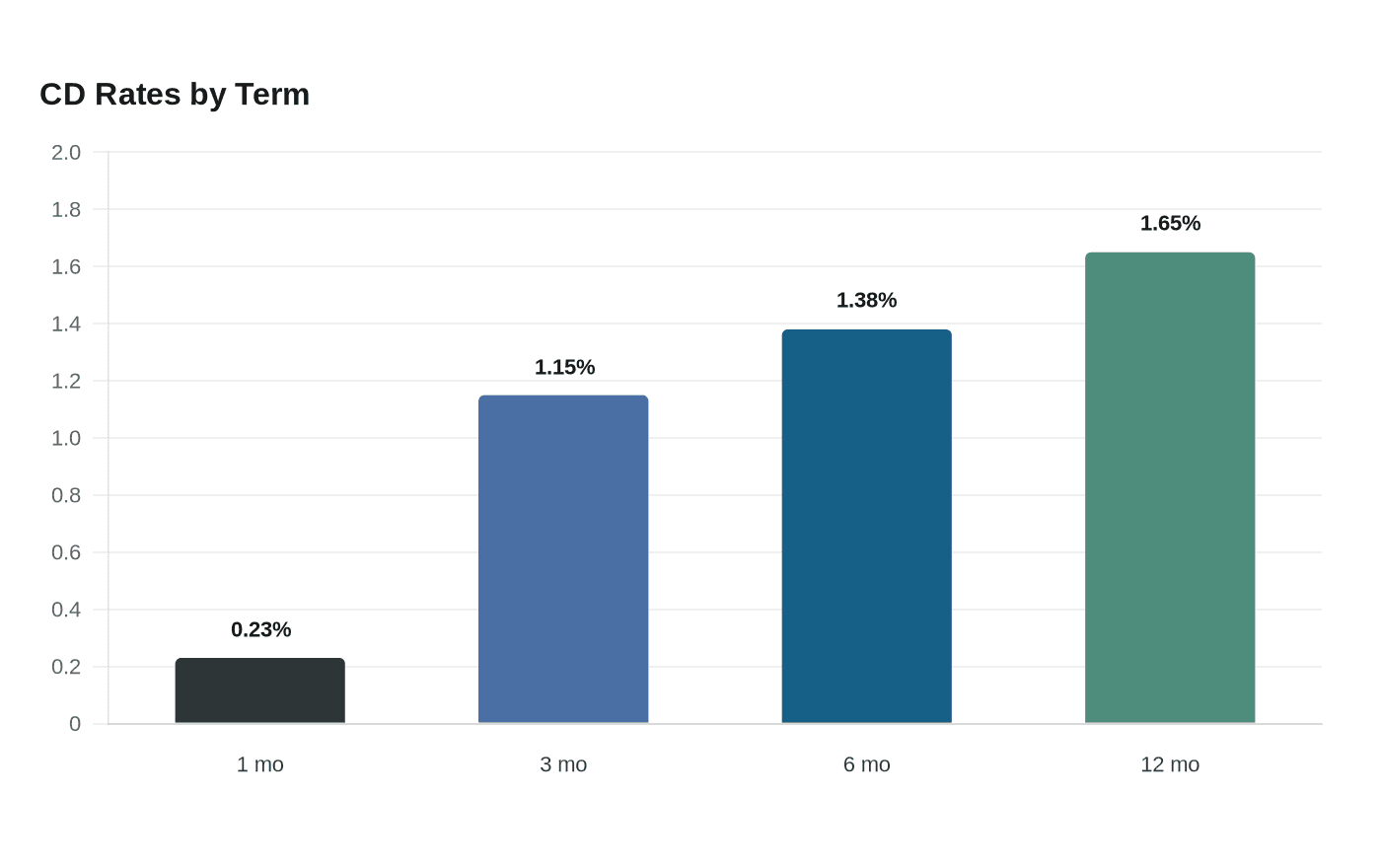

A CD is a fixed-amount savings account that holds money for a fixed period, and the bank pays interest in exchange; when it matures, you get your original deposit back plus interest. At an FDIC-insured bank, deposits are automatically insured up to $250,000 per depositor in each ownership category, so a $50,000 CD is fully covered as long as your total balance at that bank in that category stays within the limit. The FDIC’s June 15 national rate table puts the average at 0.23% for a 1-month CD, 1.15% for 3 months, 1.38% for 6 months, and 1.65% for a 12-month CD under $100,000, which works out to roughly $9.58, $143.75, $345, and $825 respectively on a $50,000 balance.

The savings-account comparison is tighter than it looks

The best high-yield savings accounts are currently paying up to 4.15% APY, according to Bankrate, while the national average savings rate is only 0.61% APY. On $50,000, that top savings rate also earns about $2,075 a year before taxes, versus about $305 at the national average, so the real comparison is not CD versus savings in the abstract, it is top-tier cash management versus average cash management. The spread between Bankrate’s 4.15% one-year CD and its 4.25% top tracked CD is only about $50 a year on $50,000, a reminder that the gain from locking money is often modest once you are already shopping in the best-rate part of the market.

Treasury bills and the Fed backdrop

Treasury bills sit in the same neighborhood, which is why they belong in this decision. The Federal Reserve says changes in the federal funds target range influence short-term interest rates, and the upper limit stood at 3.75% on June 16; that policy setting helps explain why money-market returns, CDs, and other short-term cash products are still elevated relative to the low-rate years after the pandemic and the Great Recession. In the Fed’s June 16 H.15 release, Treasury bills were quoted at 3.64% for 3 months, 3.68% for 6 months, and 3.68% for 1 year, which translates to about $455 over three months, $920 over six months, and $1,840 over a full year on a $50,000 balance before taxes.

Inflation is the real test

Inflation is where the glossy headline yield starts to fade. The Bureau of Labor Statistics says consumer prices rose 4.2% over the 12 months ending May, with core inflation at 2.9% and energy up 23.5% over the year, so a 4.15% CD barely keeps pace before taxes and leaves roughly $24 less purchasing power on a $50,000 balance. At the 1.65% national CD average, the erosion is much more obvious, about $1,224 in real purchasing-power loss on the same balance, which is why a below-average CD is a weak place to leave idle cash when inflation is still running hot.

When locking cash makes sense

That is why the right answer depends less on rate-chasing and more on timing. The FDIC has posted national CD rate data since May 18, 2009, and Bankrate notes that one-year CD APYs were above 11% nearly 40 years ago, fell below 1% after the Great Recession, and plunged below 1% again after the COVID-19 pandemic before recovering in the higher-rate environment of the 2020s. If the money has a firm date attached to it, a CD still offers certainty, and a CD ladder can preserve flexibility by staggering maturity dates; if the money may be needed soon, the small yield advantage is rarely worth surrendering access.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip