Higher inflation could push mortgage rates up, squeezing homebuyers

Inflation hit a three-year high in April, and mortgage rates were already edging up as the spring housing market lost momentum.

Higher inflation is pressing against the housing market just as many buyers make their spring decisions. The Consumer Price Index rose 0.6% in April and 3.8% over the past 12 months, the hottest annual pace since May 2023, with energy costs doing much of the work and shelter still climbing.

The energy index jumped 3.8% in April and accounted for more than 40% of the monthly increase in the all-items index. Shelter rose 0.6%, while core CPI increased 0.4% for the month and 2.8% from a year earlier. Gasoline, fuel oil and food also pushed prices higher, a mix that matters for households already stretched by housing costs.

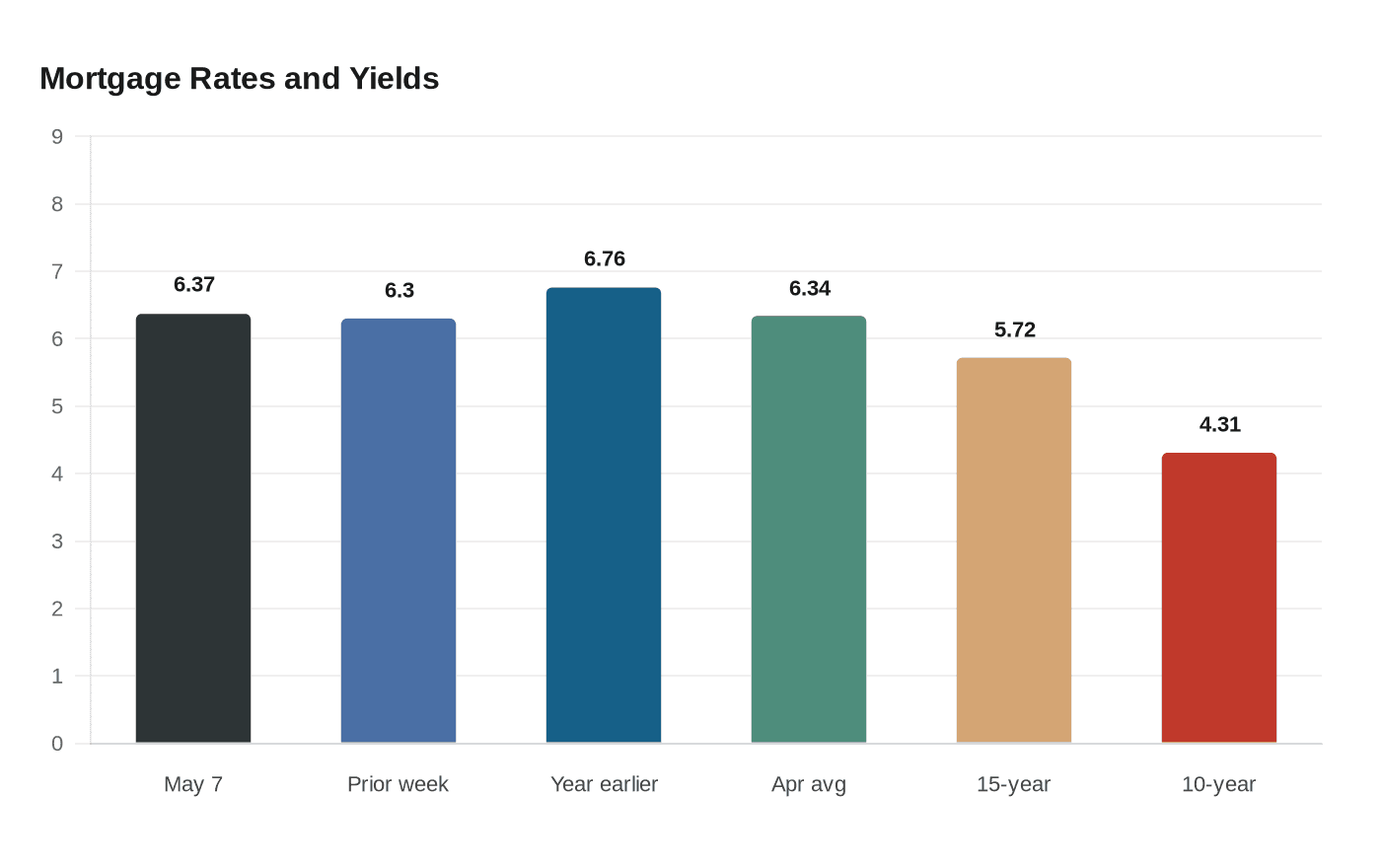

Mortgage rates had been drifting higher before the inflation report, and the latest numbers could keep pressure on them. Freddie Mac said the average 30-year fixed mortgage rate was 6.37% as of May 7, up from 6.30% the prior week and 6.76% a year earlier. The 15-year fixed rate averaged 5.72%. In April, Freddie Mac reported the 30-year rate averaged 6.34%, while the 10-year Treasury yield averaged 4.31%.

That combination is especially important for first-time buyers and people trying to refinance. Even small rate moves can change monthly payments enough to price borrowers in or out of a house search, and higher borrowing costs often force shoppers to lower their budget, increase their down payment or look farther from where they want to live. Refinancers who waited for cheaper money are finding less room to save, especially after a year in which the 30-year rate sat below current levels.

Jake Krimmel, senior economist at Realtor.com, said the inflation reading was troubling and warned that successive hot inflation reports would likely push up 10-year Treasury yields and mortgage rates, squeezing affordability and consumer sentiment. The National Association of Home Builders said mortgage rates continued to increase in April, adding more strain to a market already sensitive to borrowing costs.

The Federal Reserve left its benchmark federal funds rate unchanged at 3.5% to 3.75% on April 29, but the decision was unusually split, with four dissents, the most since October 1992. Policymakers are weighing persistent inflation against a softer labor market, and the April Beige Book said housing market activity softened in several districts as uncertainty and rising mortgage rates dampened buyer demand.

For borrowers shopping adjustable-rate products, the next few months may be a test of expectations. If inflation stays hot, Treasury yields can remain elevated, and mortgage rates can stay stubbornly high even without another Fed move. That leaves the spring market facing the same problem from two directions: prices that are still rising and financing that is not getting easier.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?