How much $30,000 can earn now in savings, money market accounts and CDs

A $30,000 cash stash can still earn more than $100 a month, but only if you choose the right account before the Fed moves again.

A $30,000 balance is earning very different returns right now, depending on whether it sits in a plain savings account, a money market account, or a certificate of deposit. The gap is wide enough to change the answer for anyone deciding between flexibility, guaranteed yield and the risk that deposit rates drift lower after the Federal Reserve’s next move.

Why the Fed backdrop matters

The Federal Reserve kept its benchmark rate unchanged at its April 28-29, 2026 meeting, leaving the effective federal funds rate at 3.64% on April 30. That pause matters for savers because deposit yields usually follow the Fed with a lag, and the next regularly scheduled FOMC meeting, June 16-17, is the next major checkpoint for whether banks and credit unions may have to adjust rates again.

Even with the policy rate still elevated by recent standards, the average savings returns on offer nationwide remain modest. The FDIC’s April 2026 national average was 0.38% for savings accounts, 0.57% for money market accounts and 1.53% for 12-month CDs. Those figures show why consumers shopping only by default can leave a lot of interest on the table.

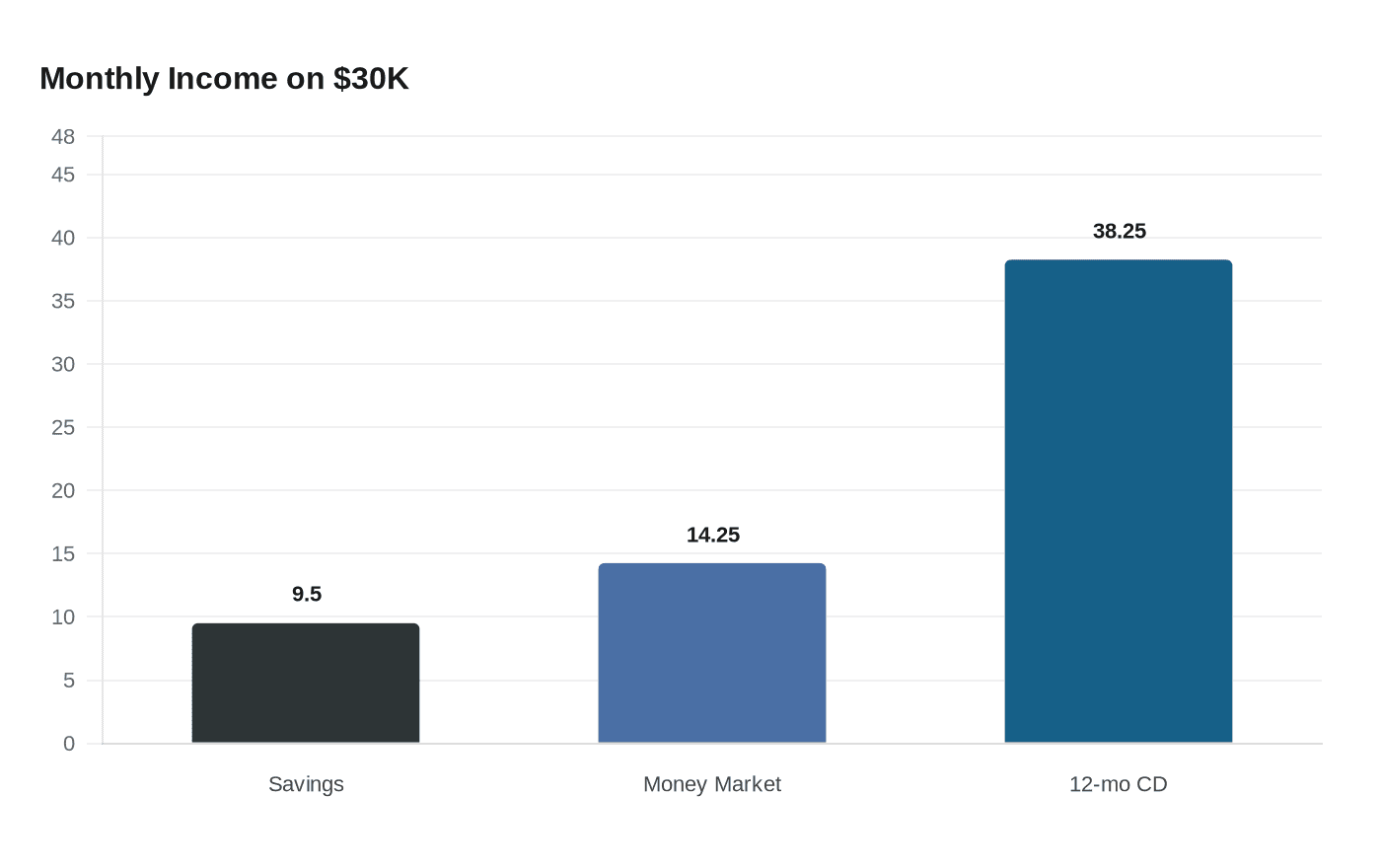

What $30,000 earns at the national averages

At the FDIC’s average rates, a $30,000 deposit produces only a small monthly stream of interest. Savings would generate about $9.50 a month, a money market account about $14.25, and a 12-month CD about $38.25, before compounding and tax considerations.

That is the first practical lesson in this rate cycle: the account label matters, but the rate matters more. The best headline offers now sit far above the averages, which means the real decision is whether you can qualify for an online or promotional rate, or whether you are settling for a broad national benchmark.

The FDIC’s rate-cap table for April 2026 shows adjusted benchmark rates of 1.13% for savings, 1.32% for money market accounts and 2.28% for 12-month CDs. Even those cap-adjusted levels trail the strongest competitive offers in the market, underscoring how much shopping around can matter for a $30,000 balance.

Where the best yields are showing up

The strongest advertised rates are still coming from online and promotional products. Bankrate’s May 2026 survey put the top CD rate tracked by its editors at 4.20% APY, offered by Mountain America Credit Union. Forbes Advisor reported the highest money market account rate at 4.22%, and its top high-yield savings accounts were still paying up to 5.00% APY.

On a $30,000 balance, those differences are not abstract. Using simple monthly interest math, $30,000 at 5.3% APY earns about $132.50 in one month, $30,000 at 4.22% APY earns about $105.50, and $30,000 at 2.5% APY earns about $62.50. That spread is the difference between a cash pile that quietly compounds and one that barely keeps pace with inflation and opportunity cost.

Savings: best when liquidity comes first

High-yield savings accounts win on accessibility. If you need same-day or near-term access to cash for emergencies, a home repair or an unpredictable bill, this is the cleanest option because the money stays liquid while still earning a competitive rate.

The catch is that savings rates move quickly when the Fed changes direction. If the central bank trims rates later this year, the top savings offers can slip as fast as they rose. That makes a high-yield savings account the right choice when you want flexibility and are willing to accept rate volatility in exchange for it.

Money market accounts: the middle ground

Money market accounts are the compromise account for savers who want some liquidity without surrendering all yield. In this snapshot, the strongest money market rate reported by Forbes Advisor, 4.22%, is close to the best savings yields and far above the FDIC’s 0.57% national average.

For a $30,000 balance, that difference is meaningful. A top-tier money market account can produce roughly $105.50 in a month at 4.22% APY, which puts it well ahead of a standard bank product while still leaving the cash available if plans change. The tradeoff is that money market accounts often come with balance rules, transaction limits or tiered pricing, so the headline rate only helps if the account structure fits your needs.

CDs: best for guaranteed yield

CDs are the clearest choice when the priority is locking in a known return. Bankrate’s top tracked CD rate of 4.20% APY is below the best savings headline rate, but it comes with a fixed term and a fixed yield, which can be valuable if you expect deposit rates to fall.

That matters especially now because the Fed is still holding policy steady and the next meeting could set the tone for the rest of the year. If you believe rates are more likely to drift down than up after June 16-17, a CD turns that uncertainty into certainty by preserving today’s yield. The cost is flexibility: money tied up in a CD is not as easy to tap as cash in a savings or money market account.

How to choose when policy is uncertain

The right answer depends less on the word in the account name and more on the role that $30,000 has in your finances.

- If liquidity is the priority, a high-yield savings account is the practical winner.

- If you want a balance of access and yield, a top money market account is the middle path.

- If you want guaranteed yield and can leave the money untouched, a CD is the better bet, especially if you think the Fed may cut later this year.

The policy signal is the final piece. With the federal funds rate at 3.64% and the next FOMC meeting set for June 16-17, deposit yields could come under pressure if the Fed shifts toward easing. For a cash holder with $30,000, that makes the current window valuable: the best returns are available now, but only for savers who choose the right account before the rate backdrop changes again.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?