How much a $10,000 CD can earn today, and why term matters

A $10,000 CD can still earn about $430 a year at the best July rates, but the FDIC average is just $165. Term choice decides how much interest you lock in and how much flexibility you keep.

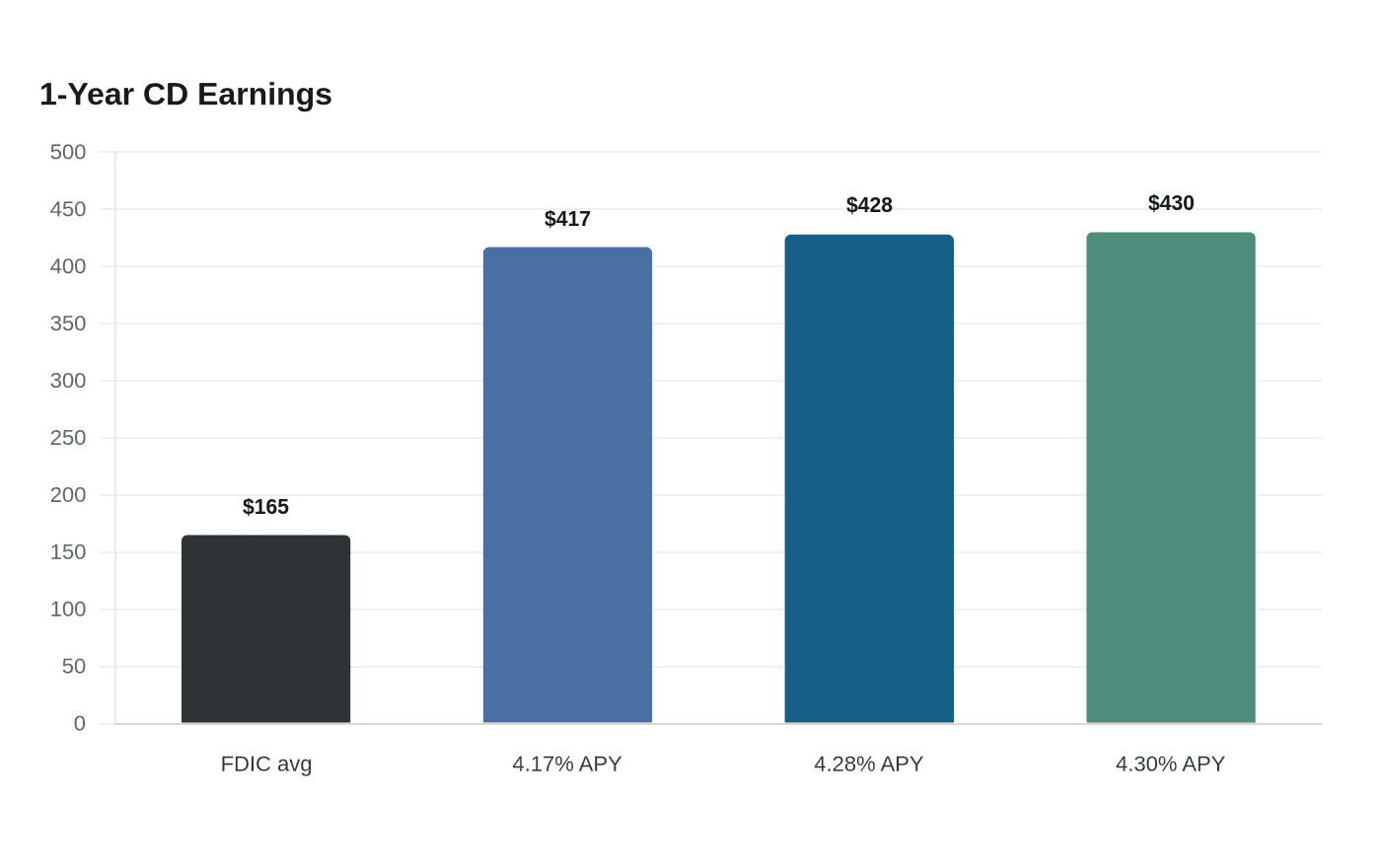

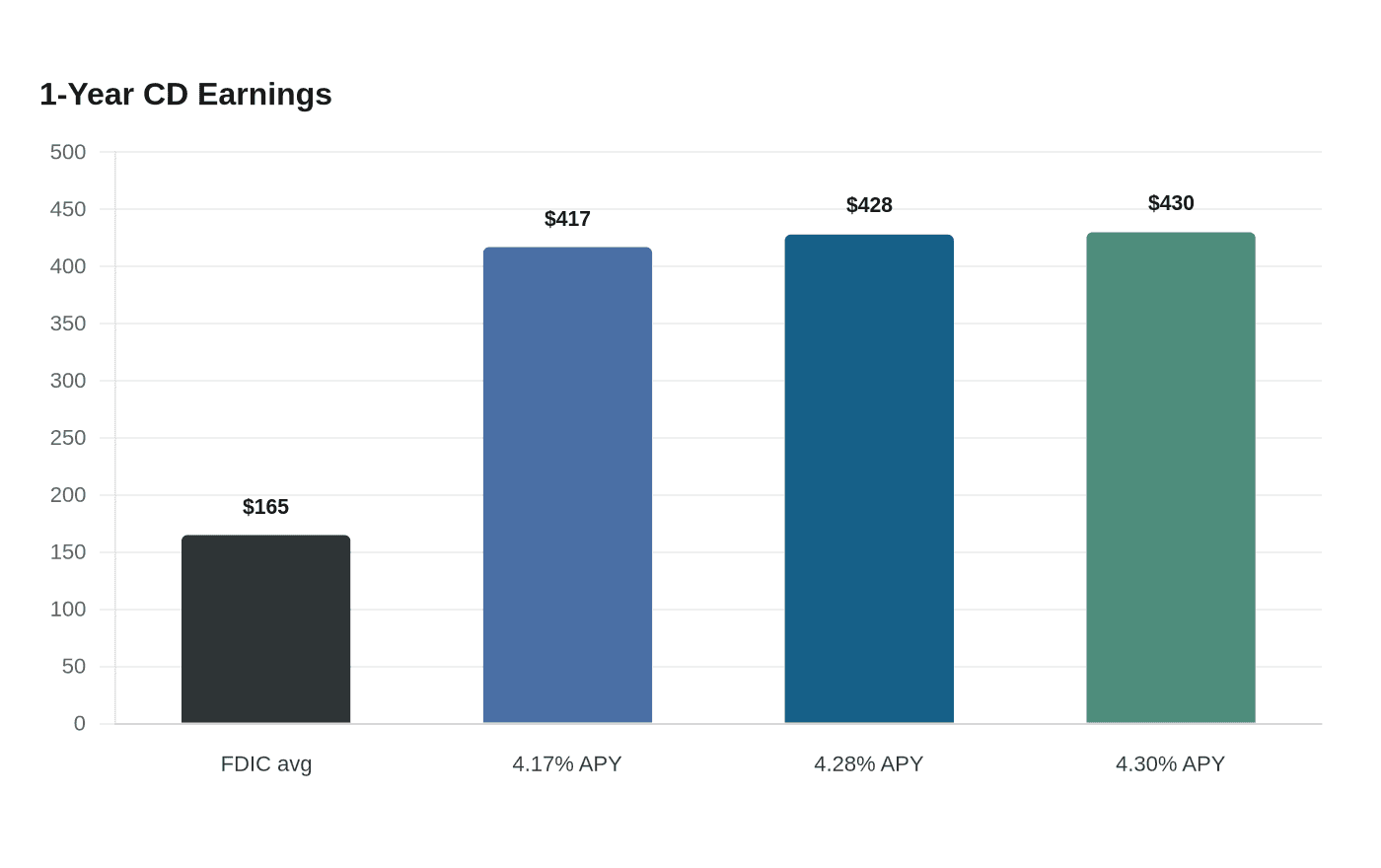

A $10,000 CD can earn only $165 at the FDIC’s national 12-month average, or about $430 at the best July 1-year rate. The right certificate can more than double the annual payout, but a longer lockup keeps your cash off-limits.

What a $10,000 CD earns right now

The Federal Deposit Insurance Corporation’s June 2026 table puts the national rate for a 12-month CD under $100 million at 1.65000%. On a $10,000 deposit, that works out to about $165 in interest over a year. The FRED series for the FDIC national rate on 12-month CDs, maintained in St. Louis, Missouri, runs through June 1, 2026.

The best advertised July rates are much higher, and the difference is easy to see in dollars:

- At 4.17% APY, a $10,000 one-year CD earns about $417.

- At 4.28% APY, it earns about $428.

- At 4.30% APY, it earns about $430.

In July 2026, Bankrate listed top advertised 1-year rates up to 4.17% APY. Investopedia and NerdWallet listed 4.30% APY still available, while CNBC Select listed up to 4.28% APY. The best short-term CDs can pay roughly $252 to $265 more than the FDIC average on the same $10,000 balance in a single year.

Why term changes the payout

Once the term length stretches out, compounding starts to matter just as much as the headline APY. In NerdWallet’s July rate snapshot, a 3-year CD was around 3.85% APY, and a $10,000 deposit would grow to about $11,200 if the rate held for the full term, producing roughly $1,200 in total interest. At 4.28% APY, a 5-year CD would compound to about $12,331, or roughly $2,331 in interest.

That extra return comes with a tradeoff built into the CD itself. A 5-year term can generate more than $1,100 in additional interest versus the 3-year example, but the cash stays tied up much longer. If rates fall, a long CD can look smart because you already locked in a stronger yield; if rates rise or a better offer appears, the money is still sitting in the old contract.

The real decision is rate versus flexibility

A 1-year CD at 4.30% APY gives you a fast reset point, which matters if the market shifts, if rate cuts show up, or if a stronger offer appears later. A longer CD can be useful when you want to secure today’s yield for several years, but it reduces your ability to move quickly.

Bankrate’s 2026 forecast expects CD APYs to trend lower, even if they still beat inflation. Locking in a 4%-plus rate now trades off against keeping some cash available for a later round of pricing. In a falling-rate environment, shorter terms preserve optionality; in a stable or declining market, longer terms can protect the return you already have.

Insurance and market context

Most bank CDs are backed by the Federal Deposit Insurance Corporation, and credit union CDs carry NCUA insurance, so the core choice is usually not about credit risk. It is about yield, timing, and whether your cash can sit still long enough to justify the rate. Many online banks are still advertising returns well above the national average.

Certificates of deposit have swung dramatically over time, with much higher yields in earlier eras than the lower averages common now.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?