How much wage garnishment can cut your take-home pay, by debt type

A garnished paycheck can shrink fast, but federal caps differ by debt type. Child support and student loan defaults can cut far more than ordinary consumer debt.

How much your paycheck can shrink depends first on the debt

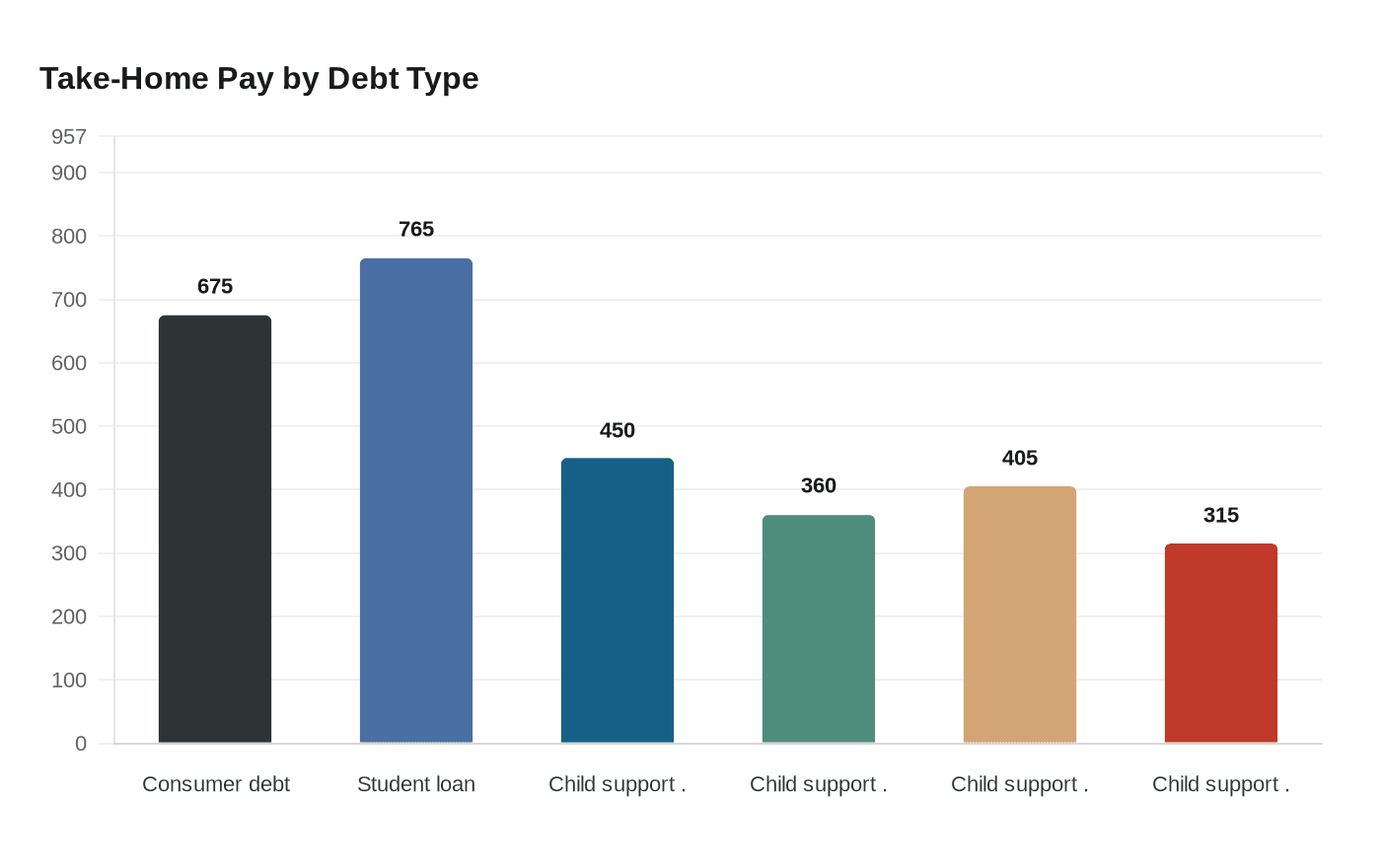

A worker bringing home $900 in disposable weekly pay could see that amount fall to $675 under the federal cap for ordinary consumer debt, to $765 if a defaulted federal student loan triggers withholding, or as low as $450 if child support reaches the 50% limit. The difference is not just legal fine print. It is the gap between a manageable hit and a paycheck that suddenly feels half gone.

Disposable earnings are the pay left after legally required deductions. Under federal law, ordinary consumer-debt garnishment is generally limited to the lesser of 25% of disposable earnings or the amount by which disposable earnings exceed 30 times the federal minimum wage, which is $7.25 an hour. That threshold works out to $217.50 a week. In practice, the rule creates a ceiling that is meant to protect lower earners from losing too much of every paycheck.

Ordinary consumer debt has the tightest federal cap

For standard consumer debts, the Consumer Credit Protection Act keeps the weekly garnish amount at the lesser of 25% of disposable earnings or the amount above 30 times the federal minimum wage. On a $900 weekly disposable paycheck, 25% equals $225, so that is the maximum cut. The remaining take-home pay would be $675.

The Department of Labor says this limit applies regardless of how many garnishment orders an employer receives for that week. In other words, multiple creditors do not multiply the federal cap for ordinary debt. The law also protects workers from being fired because wages were garnished for any one debt, a safeguard that matters as much as the dollar limit itself.

That protection has a long history. Title III of the Consumer Credit Protection Act, enacted in 1968, was written to keep wage seizure from turning into job loss and financial free fall. Congress recognized that if a paycheck can be carved up too aggressively, the worker can quickly lose the ability to stay employed, pay rent, or keep up with the next obligation.

Child support can take much more

Child support is the debt type that can cut deepest under federal rules. Federal guidance allows withholding of up to 50% of disposable earnings if the worker supports another spouse or child, or 60% if not. If support payments are more than 12 weeks overdue, those limits can rise by 5 percentage points.

That means the same $900 weekly disposable paycheck could fall to $450 under the 50% cap, or to $360 under the 60% cap. If payments are seriously overdue, the cut could rise to 55% or 65%, leaving just $405 or $315. For families living paycheck to paycheck, those percentages can change the monthly math immediately.

Child support is administered through a separate federal framework, including guidance from the Office of Child Support Enforcement within the U.S. Department of Health and Human Services. The practical lesson is simple: if the paycheck cut is unusually large, child support rules may be responsible, and the federal ceiling is far higher than the ordinary consumer debt cap.

Defaulted federal student loans can be garnished without court

Federal student loan default is another route to wage garnishment, and it does not require the lender to go to court first. Federal Student Aid says a loan holder can order an employer to withhold up to 15% of disposable pay to collect the defaulted debt. On a $900 weekly disposable paycheck, that would mean a maximum deduction of $135 and take-home pay of $765.

Unlike the one-time cut in some debt disputes, this withholding continues until the defaulted loan is paid in full or the default status is resolved. That makes the student-loan garnishment a running drag on cash flow, not a one-off event. For borrowers already juggling rent, food, and transportation, the ongoing nature of the deduction can matter as much as the percentage itself.

IRS tax levies work differently from standard garnishment

Federal tax debt is handled through an IRS levy system rather than a standard consumer garnishment. The exempt amount is not a fixed percentage. Instead, it is determined by IRS Publication 1494 and depends on filing status, dependents, and pay period. The IRS says the agency mails that publication with the levy notice, and employers must provide the worker a Statement of Dependents and Filing Status to complete and return within three days.

That makes tax levies harder to estimate from one generic rule. A worker may see a sharply reduced paycheck, but the exact amount depends on household size and filing details, not on the ordinary 25% consumer-debt cap. If the paycheck drops and an IRS levy is involved, the first move is to read the paperwork closely and respond quickly, because the exempt amount hinges on forms that shape how much pay is protected.

What to do immediately if your paycheck is smaller than expected

The first shock is usually the best time to act, because the law treats different debts differently. A worker who sees a sudden cut can move fast with a few practical steps:

1. Confirm the debt type.

Ordinary consumer debt, child support, student loans, and IRS levies all use different rules and different ceilings.

2. Compare the deduction with the federal limit.

For ordinary debt, check the 25% cap and the 30-times-minimum-wage test. For child support and student loans, check whether the deduction fits the higher percentages allowed by law.

3. Ask payroll or the withholding agency for the calculation.

The number should line up with disposable earnings, not gross pay.

4. Respond to tax levy paperwork right away.

If the IRS has sent a Statement of Dependents and Filing Status, the three-day deadline matters.

If the cut looks too large, state law may also matter. The National Consumer Law Center says state exemption laws can provide stronger protection than federal law, and that those rules need updating as inflation, layoffs, and rising debt collection suits put more pressure on households. That is a policy point with a real pocketbook effect: a state exemption can sometimes preserve more wages than the federal floor.

The bottom line is that wage garnishment is not one number. It is a set of rules that can leave a worker with 75% of disposable earnings in one case, 85% in another, or far less when child support or tax levies enter the picture. The fastest way to judge the damage is to identify the debt, apply the right cap, and move immediately if the paycheck is smaller than the law allows.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?