IDC warns smartphone shipments will plunge 12.9% to 1.12 billion units in 2026

IDC projects the largest-ever annual smartphone decline as DRAM and NAND prices spike, raising ASPs and squeezing low-end makers while Apple and Samsung stand to gain.

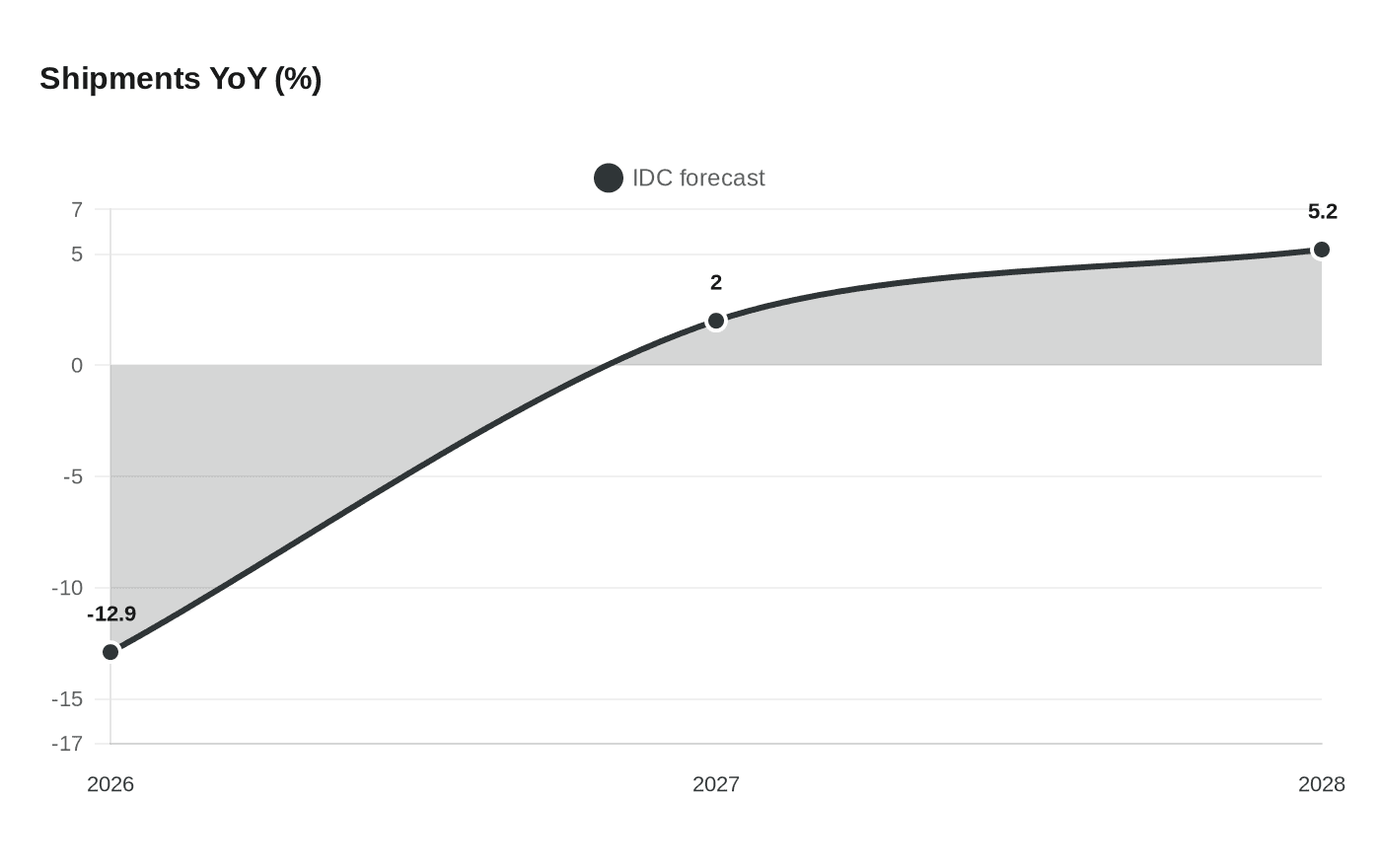

IDC projects global smartphone shipments will fall 12.9% in 2026 to 1.12 billion units, the research firm said, marking the steepest annual drop in the market’s history and setting shipments at their lowest level in more than a decade. The decline, IDC attributes primarily to sharp increases in DRAM and NAND memory prices as memory chips are diverted toward large-scale AI infrastructure projects, producing what one company executive called a structural shock to the supply chain.

“What we are witnessing is not a temporary squeeze, but a tsunami-like shock originating in the memory supply chain,” said Francisco Jeronimo, IDC’s vice president for Worldwide Client Devices. Nabila Popal, senior research director of IDC’s Mobile Phone Tracker, added that “the memory crisis will cause more than a temporary decline; it marks a structural reset of the entire market.” Popal warned that while memory prices may stabilize by mid-2027, they are unlikely to return to previous levels and that the sub-$100 phone segment will become “permanently uneconomical.”

IDC’s model projects the industry average selling price to rise about 14% to a record $523 in 2026 as manufacturers shift product mixes toward higher-margin models to absorb inflated component costs. That step-change in prices threatens to accelerate market consolidation: well-capitalized brands such as Apple and Samsung are expected to expand share, while smaller low-end Android manufacturers face the greatest risk of shrinking or exiting the market.

Independent researcher Counterpoint Research offered a corroborating forecast, projecting roughly a 12% year-on-year decline in shipments and describing 2026 as the “sharpest decline on record.” Counterpoint and IDC both expect the earliest meaningful inflection only once additional memory capacity comes online; IDC foresees a modest 2% recovery in 2027 followed by a 5.2% rebound in 2028, but cautioned that volumes are unlikely to return to prior norms.

The mechanics behind the shock are straightforward and consequential. Memory components account for a rising share of bill-of-materials costs as AI workloads demand higher-capacity DRAM and fast NAND for data-center accelerators. That diversion tightens supply to consumer-device makers, who face either absorbing higher costs or raising retail prices. The result is a simultaneous supply and demand adjustment: manufacturers raise prices and narrow lower-cost offerings, while some customers delay upgrades or buy refurbished models.

Macroeconomic implications extend beyond handset vendors. A sustained jump in device ASPs will feed into consumer electronics inflation measures and could depress discretionary spending in other durable categories. The memory shock also highlights strategic supply-chain risk: capital-intensive memory fabs take years to bring online, creating a multi-year window in which policy choices matter.

For policymakers and industry planners, the crisis increases pressure to accelerate capacity investment and coordinate incentives for memory manufacturing. It also raises questions about how to balance investment in AI compute against the broader digital economy’s hardware affordability.

The coming months will test whether additional capacity or inventory reallocation can blunt the shock, but for consumers and many small manufacturers the immediate picture looks stark: higher prices, thinner product ranges, and a reconfigured smartphone market shaped by memory economics rather than handset innovation alone.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?