Investment Bankers Keep Dealmaking Alive Despite Widening Iran War

Wall Street closed its strongest deal quarter while Brent crude hit $120 and BlackRock froze withdrawals; Bloomberg's Paul Davies calls the calm dangerous complacency.

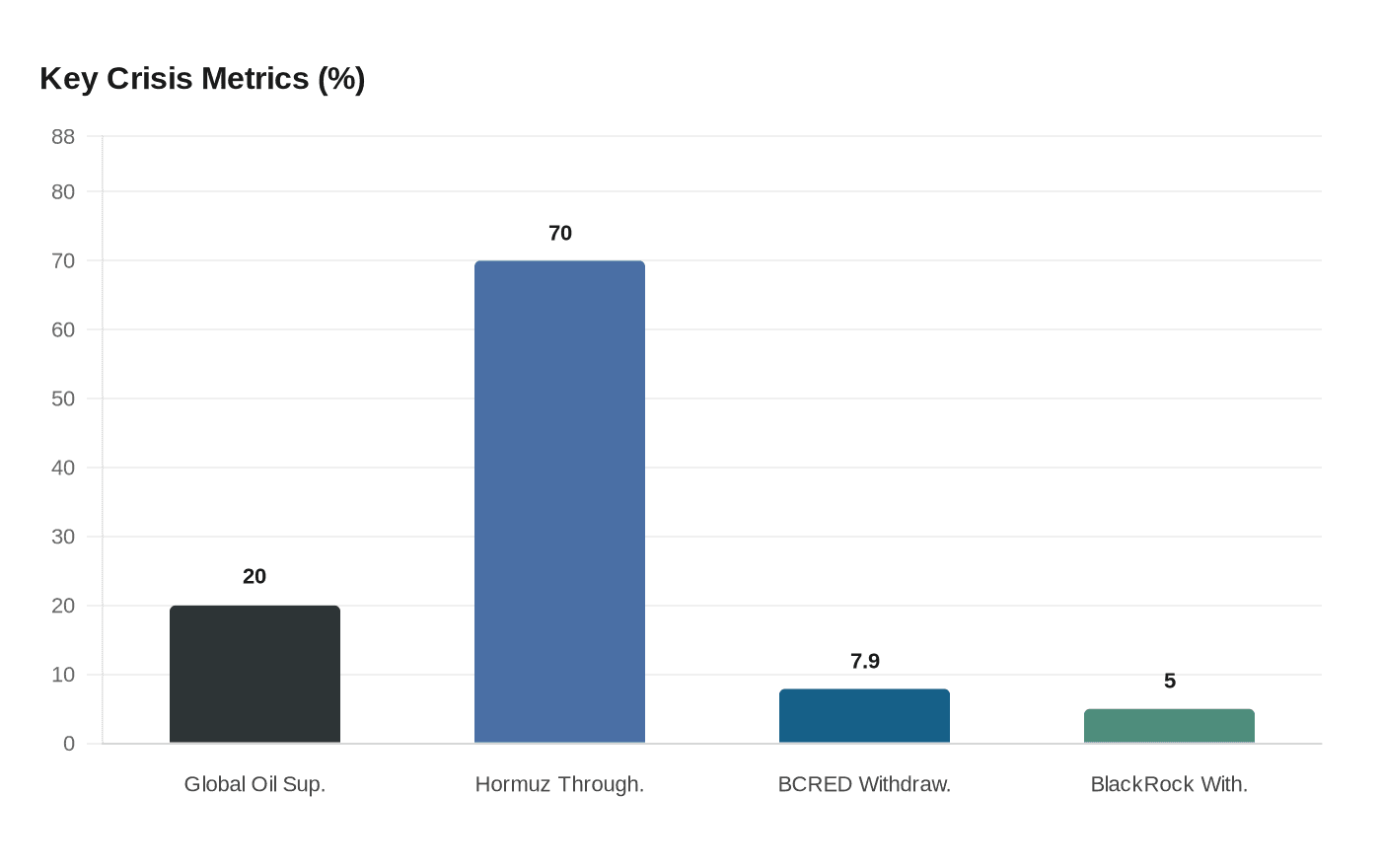

While Brent crude surged toward $120 a barrel, over 150 tankers anchored outside a shuttered Strait of Hormuz, and private credit funds began gating redemptions, Wall Street's deal desks stayed open. That gap between geopolitical reality and financial behavior forms the central paradox Bloomberg Opinion columnist Paul J. Davies examined Monday: investment banking rounded out what looked, on paper, like a strong first quarter despite a widening U.S.-Israel war against Iran that has disrupted roughly 20% of the global oil supply.

The pipeline of sizable transactions kept closing. Fees kept accruing. Private-equity firms pressed ahead with fundraising and acquisitions. Corporate issuers, wary of missing a window that could close without warning, rushed to print debt and equity. Banks showed little appetite for pulling back on underwriting even as energy markets signaled a supply shock of historic magnitude. US crude posted its largest single-week gain on record in data going back to 1983, and Goldman Sachs warned prices could climb above $100 per barrel if shipping disruptions persisted. The Strait of Hormuz closed to meaningful tanker traffic after the conflict began February 28, with throughput dropping first by roughly 70% and then to near zero, forcing Gulf producers to curtail output as storage capacity filled.

None of that, apparently, was enough to stop a deal from getting inked.

Davies argued that what looks like resilience could just as easily be complacency. The private credit market offered the most visible stress fracture already visible on the surface. Funds including BlackRock's HLEND and Blackstone's BCRED moved to gate withdrawals as investors sought exits. At Blackstone's vehicle alone, clients requested to pull $3.8 billion, equal to 7.9% of assets, forcing the firm to raise $400 million from its own capital and senior executives to satisfy redemptions. BlackRock, in its own disclosures, acknowledged "a structural mismatch between investor capital and the expected duration of private credit loans" as it imposed a 5% cap on withdrawals. The broader private credit selldown reached an estimated $265 billion.

That admission matters enormously for what comes next in deal markets. Davies identified a feedback loop that, once triggered, could move with unusual speed: elevated energy prices sustained by the Hormuz closure stress corporate borrowers, rising borrower stress drives default rates higher across private credit, and deteriorating private credit conditions erode the underwriting capacity and investor appetite that propped up the deal market all quarter. The Dallas Federal Reserve estimated that if the Hormuz disruption persists for three quarters, fourth-quarter global GDP growth in 2026 could fall 1.3 percentage points. An M&A season that started strong could unravel under that weight.

The sectors carrying the most concentrated risk sit precisely at the intersection of these vulnerabilities. Energy-intensive industrials face direct margin compression. Transportation and logistics operators contend with both rerouted shipping lanes and rising fuel costs that compress margins at both ends. Companies whose valuations rest on AI-driven growth assumptions may discover that a genuine credit tightening has a way of recalibrating even the most optimistic discounted cash-flow models.

Davies named his two most likely triggers for a reversal: an energy-price shock and accelerating private-credit defaults. He noted the quarter may "close strong" for investment banking fees, but warned there are "plenty of warning signs that things could come to a grinding halt." Institutional investors need to stress-test portfolios for higher energy and default scenarios rather than treating recent calm as a baseline. Corporate CFOs counting on continued market access in a protracted conflict are making a bet that history seldom rewards. The question Davies posed is whether bankers are reading genuine market resilience correctly or whether they are, as the tankers anchored off Hormuz might suggest, simply waiting to find out what is on the other side of the blockade.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?