Job‑cut announcements ease in early March after January’s dramatic surge

Bloomberg reported early‑March layoffs slowed after January’s 108,435 cuts; the shift may signal tentative stabilization amid still‑elevated corporate retrenchment.

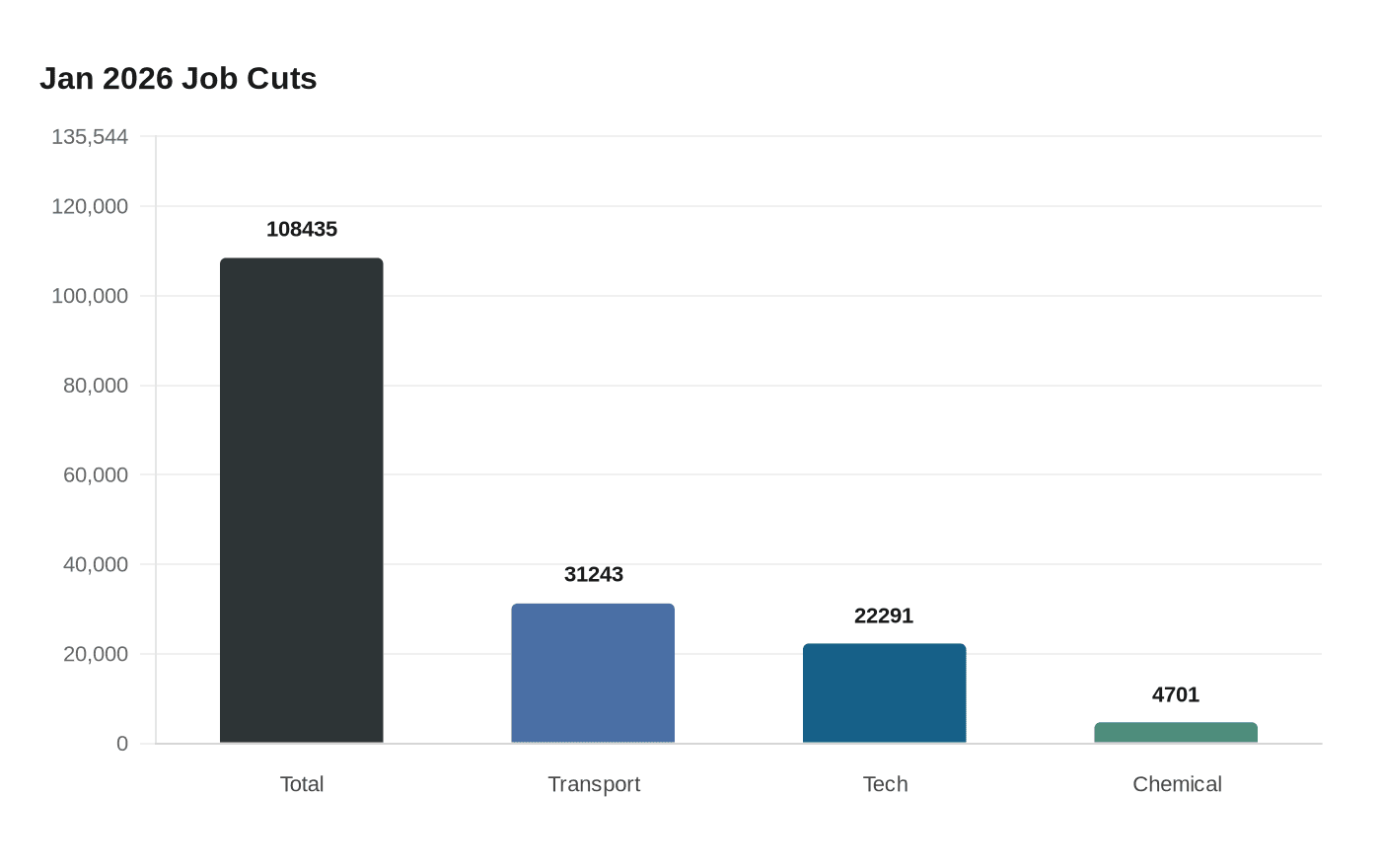

Bloomberg reported that U.S. job‑cut announcements eased in early March after a sharp surge in January, a development that analysts say could be an early sign corporate headcount reductions are beginning to level off. The January surge, however, remains historically large: Challenger, Gray & Christmas reported that U.S. employers announced 108,435 job cuts in January 2026, the highest January total since 2009 and the biggest monthly tally since October 2025.

Challenger’s January figure was up 118 percent from 49,795 cuts in January 2025 and, the firm said, up 205 percent from December 2025. Challenger’s release flagged January hiring plans as the lowest on record, listing hiring plans at just 5,306 people for the month. Andy Challenger, workplace expert and chief revenue officer at Challenger, Gray & Christmas, said, “Generally, we see a high number of job cuts in the first quarter, but this is a high total for January. It means most of these plans were set at the end of 2025, signaling employers are less-than-optimistic about the outlook for 2026.”

Industry detail underscores how concentrated the wave was. Transportation accounted for 31,243 announced cuts in January, a total driven almost entirely by UPS’s announcement it would cut 30,000 jobs after severing ties with Amazon. Technology firms announced 22,291 cuts in January, with Amazon’s 16,000‑role reduction the largest single contribution as the company restructures management layers. Chemical manufacturers recorded 4,701 job cuts, largely tied to a Dow Inc. announcement that cited a shift to implementing artificial intelligence and automation; Challenger noted that was the chemical sector’s worst month since February 2016, when merger‑related actions drove 6,640 cuts.

TradingEconomics, which republishes Challenger data and provides historical series context, noted the January total contrasts with long‑run averages: the Challenger series averaged about 67,152 monthly cuts from 1994 through 2026, with an all‑time peak of 671,129 in April 2020 and a record low of 14,875 in November 2021. TradingEconomics also flagged related labor metrics that help frame the picture of a still‑tight market: initial jobless claims at about 212,000 in February and JOLTS job openings near 6.5 million in December 2025.

For markets and policy makers, the pattern matters more than any single month. A sharp early‑year increase in announced cuts tilts near‑term risks toward slower payroll growth and weaker consumer spending in affected regions, while a pullback in announcements could relieve some pressure on hiring costs and the unemployment outlook. That dynamic feeds directly into Federal Reserve deliberations: sustained, broad declines in layoffs would lessen downside risk to payrolls and might slow calls for policy easing, while renewed spikes would raise concerns about a sharper labor market correction.

Caveats remain. Bloomberg’s report characterizes the early‑March easing as preliminary, and source releases show minor discrepancies in the December baseline Challenger used for month‑over‑month comparisons. Analysts say the decisive signal will come only if weekly and company‑level announcements through March confirm the slowdown. For now, the tapering in notices is a cautious sign, not a reversal, in a labor market still adjusting to automation, corporate restructurings and uneven demand.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?