Kimberly-Clark beats sales estimates, keeps 2026 outlook amid cautious shoppers

Kimberly-Clark grew first-quarter sales 2.7% to $4.2 billion as price cuts and steady volumes signaled shoppers are still buying staples, but more carefully.

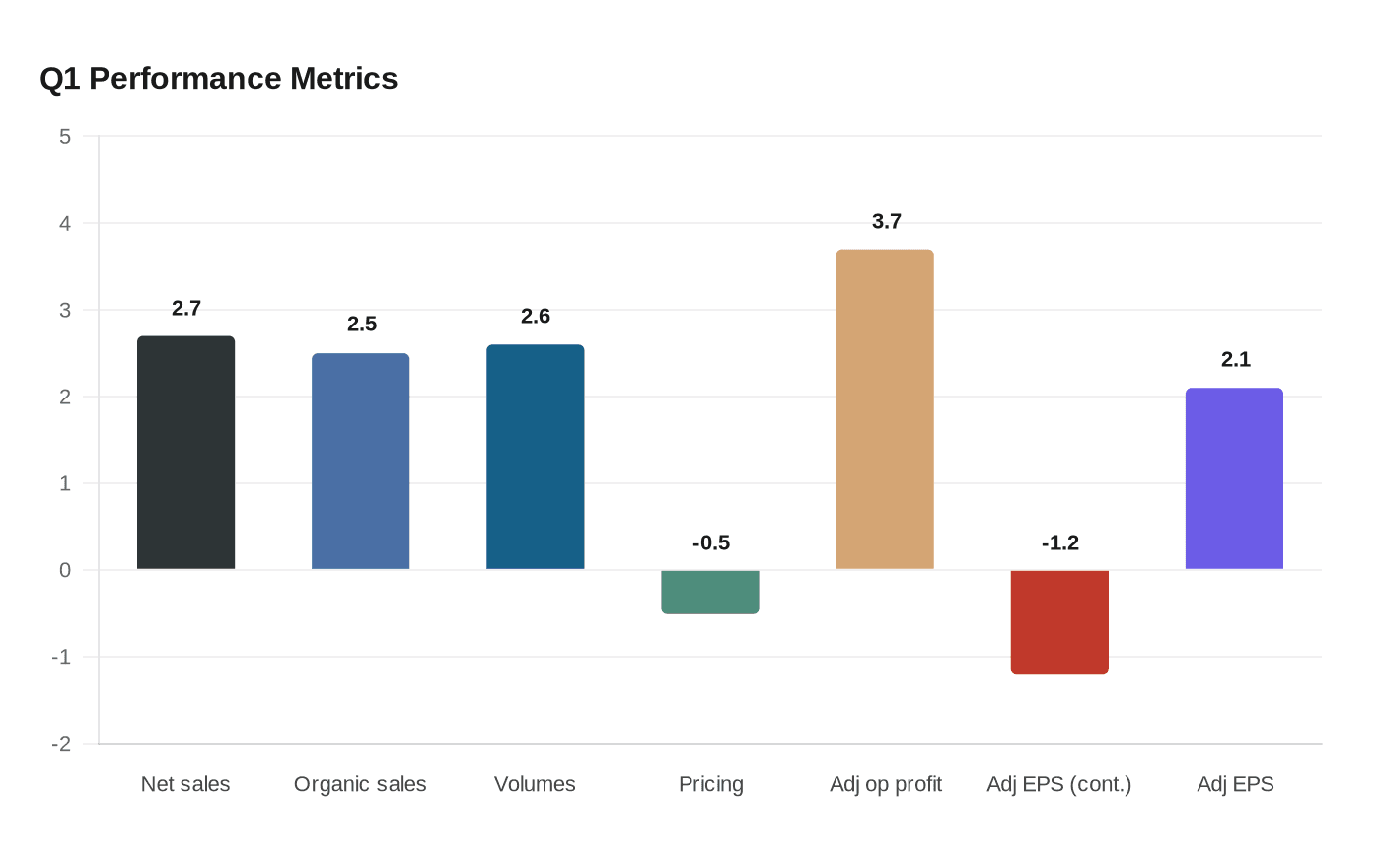

Kimberly-Clark showed how a consumer-staples company can still grow when household budgets are squeezed: families kept buying diapers, tissues and other paper goods, but they did so with a sharper eye on price. Net sales rose 2.7% to $4.2 billion in the first quarter, above analyst expectations, while organic sales increased 2.5% and overall volumes climbed 2.6% even as pricing fell 0.5%.

That mix matters because it suggests demand has not broken, but it has become more disciplined. Kimberly-Clark said favorable currency added 2.0 percentage points to net sales, while the exit of its U.S. private-label diaper business cut 1.8 points from sales growth. Gross margin came in at 36.8%, with adjusted gross margin at 37.9%, down 60 basis points from a year earlier as lower prices and spending on innovation and supply-chain work weighed on profitability. Adjusted operating profit still rose 3.7% to $732 million.

Earnings were more mixed. Adjusted EPS from continuing operations fell 1.2% to $1.60, while diluted EPS attributable to Kimberly-Clark was $2.00 and adjusted EPS attributable to Kimberly-Clark rose 2.1% to $1.97. Mike Hsu said the quarter reflected resilient consumer demand, consumer-inspired innovation and productivity gains, and he said the company was building share momentum heading into a second quarter that he described as one of Kimberly-Clark’s strongest launch and commercial activation periods in years.

The Dallas-based company kept its full-year 2026 outlook unchanged, calling for mid-to-high single-digit adjusted operating profit growth and double-digit adjusted EPS growth on a constant-currency basis. For a market still looking for signs that higher prices and tighter spending are slowing the staples category, that guidance suggests Kimberly-Clark believes shoppers are cautious, but still willing to pay for trusted brands when the value proposition is right.

The first-quarter performance also comes as Kimberly-Clark pushes ahead with its planned acquisition of Kenvue Inc. of Summit, New Jersey. The companies announced the cash-and-stock deal on Nov. 3, 2025, valuing Kenvue at about $48.7 billion enterprise value and saying the combined company would hold 10 billion-dollar brands with $2.1 billion in expected run-rate synergies. Shareholders approved the merger on Jan. 29, 2026, and the companies still expect it to close in the second half of 2026, a transaction that could broaden Kimberly-Clark’s scale just as consumers keep hunting for deals.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?