Kinderhook to buy Enhabit in $1.1 billion all‑cash deal, per‑share payout $13.80

Enhabit will be taken private in an all‑cash deal that could reshape home health access and workforce stability across 34 states.

Enhabit, Inc. said it has entered into a definitive agreement to be acquired by Kinderhook Industries in an all‑cash transaction with a reported enterprise value of approximately $1.1 billion, Citybiz reported, and HospiceNews said Enhabit stockholders will receive about $13.80 per share, a figure the outlet characterized as about 24.4% of the company’s closing stock price. The companies announced the agreement on February 23, 2026.

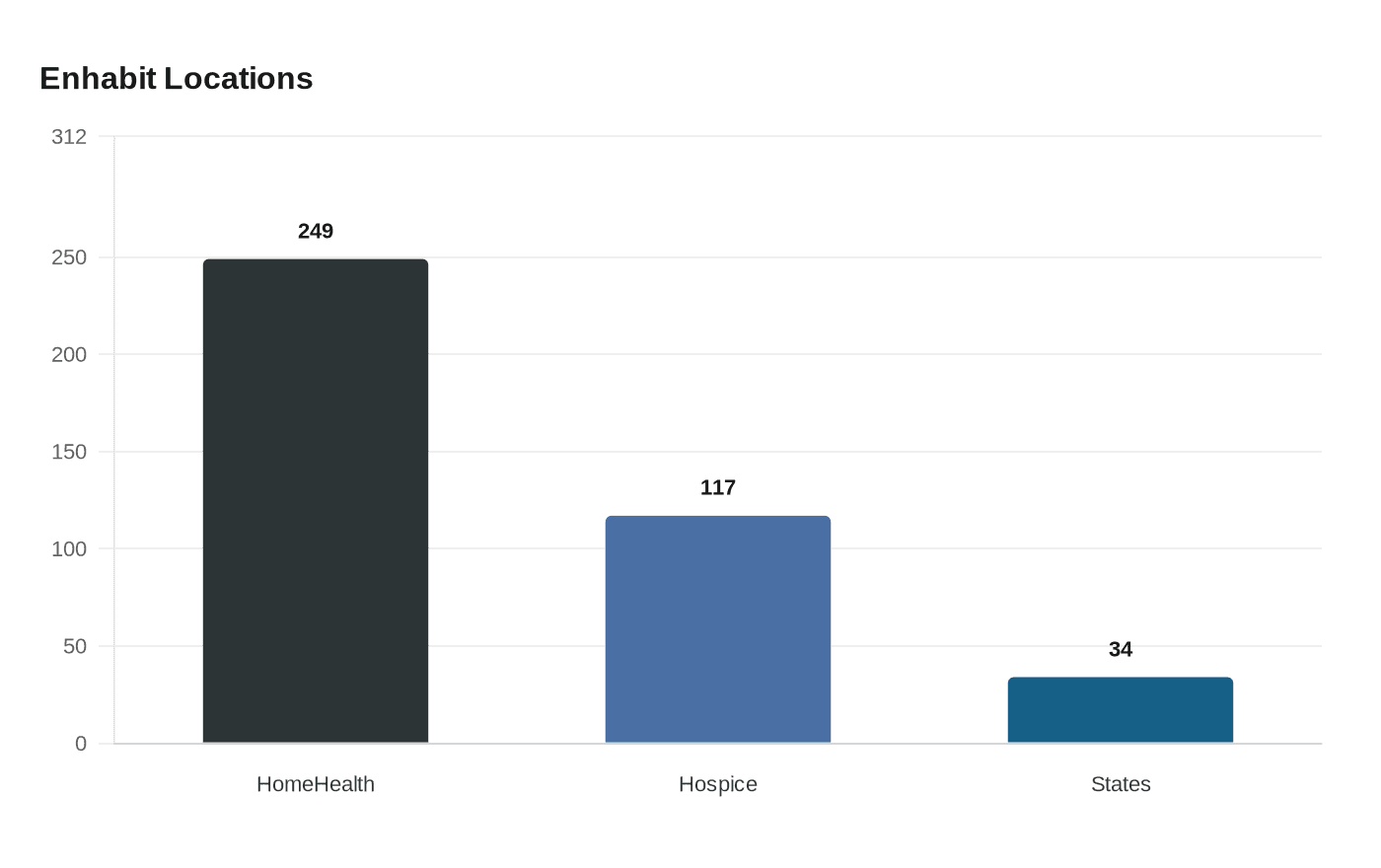

The deal consolidates a national home health and hospice provider that operates “more than 249 home health locations and 117 hospice locations across 34 states,” HospiceNews reported. Enhabit trades on the NYSE under the ticker EHAB and is led by President and Chief Executive Officer Barb Jacobsmeyer, who in Home Health Care News said, “Over the last four years, Enhabit has strengthened its role as a leading national provider of home health and hospice care, and this agreement is a terrific outcome for our stockholders, clinicians, caregivers, patients and their families.”

Kinderhook is described variously in the reporting as a middle‑market private equity firm and as a private equity investor focused on lower‑middle market healthcare. Home Health Care News noted Kinderhook’s investments span health care, environmental and industrial services, and light manufacturing and automotive industries; HospiceNews highlighted a “20‑year track record” of investing in industry‑leading companies. Kinderhook press release excerpts show recent portfolio activity in locations including Norwalk, CT; Phoenix, AZ; New York, NY; and Northville, MI, illustrating the firm’s dealmaking footprint.

Kinderhook leaders framed the transaction as growth capital for Enhabit. Matt Bubis, managing director at Kinderhook, told Home Health Care News, “Thanks to its exceptional care teams and strong leadership, Enhabit has built a reputation for excellence across the health care industry.” Citybiz quoted Chris Michalik, managing director at Kinderhook: “We have long admired Enhabit’s leadership, patient-centric culture and strong market position in home-based care. Our growth-oriented investment strategy provides our management teams with long-term capital and practical support so they can focus on what they do best – running a great company that expands access to care, elevates quality, and delivers better outcomes for the patients and families they serve.”

Observers say private equity purchases of home health chains often raise questions about continuity of care, staffing and access in rural and low‑income communities. Enhabit’s CEO told HospiceNews the company expects to use Kinderhook’s resources to “support long-term investments in our people, clinical excellence and innovation without the short-term pressures of the public markets,” and that the partners “look forward to working together to expand access to our critical home health and hospice services for families and their communities.”

The transaction remains subject to customary conditions. Finance Yahoo cautioned that forward-looking statements are subject to numerous risks and uncertainties and quoted a list including: “Because such statements are based on expectations as to future financial and operating results and are not statements of fact, actual results may differ materially from those projected and are subject to a number of known and unknown risks and uncertainties, including: (i) the risk that the proposed transaction may not be completed in a timely manner or at all, which may adversely affect Enhabit’s business and the price of its common stock; (ii) the failure to satisfy any of the conditions to the consummation of the transaction, including the receipt of certain regulatory approvals; (iii) the failure to obtain stockholder approval of the transaction; (iv) the occurrence of any fact, event, change, development or circumstance that could give rise to the termination of the transaction agreement, including in circumstances requiring Enhabit to pay a termination fee; (v) the effect of the announcement or pendency of the proposed transaction on Enhabit’s business relationships, operating results and business generally; (vi) risks that the proposed transaction disrupts Enhabit’s current plans and operations; (vii) Enhabit’s ability to retain and hire key personnel and maintain relationships with key business partners and customers, and others with whom it does business, in light of the proposed transaction; (viii) risks related to the diversion of management’s attention from Enhabit’s ongoing business operations; (ix) unexpected costs, charges or expenses resulting from the proposed transaction; (x) the ability of Kinderhook to obtain financing for the proposed transaction; (xi) potential litigation relating to the proposed transaction that could be instituted against the parties to the transaction agreement or their respective directors, managers or officers, including the effects of any outcomes related thereto; (xii) continued availability of capital and financing; (xiii) certain restrictions during the pendency of the proposed transaction that may impact Enhabit’s ability to pursue certain business opportunities or strategic transactions; and (xiv) other risks described in Enhabit’s filings with the U.S. Securities and Exchange Commission (the "SEC"), such”

No closing date, financing commitments or regulatory bodies were specified in the available reporting. As the transaction moves forward, industry stakeholders and policy makers will need to weigh whether promised investments translate to more equitable access and stable jobs for frontline caregivers, particularly in communities that rely heavily on home‑based care.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?