Low financial literacy leaves Americans vulnerable to money mistakes

Low financial literacy is turning routine money decisions into costly setbacks, from overdraft fees and scam losses to the risk of being unbanked. The strain is worst where prices and debt collide.

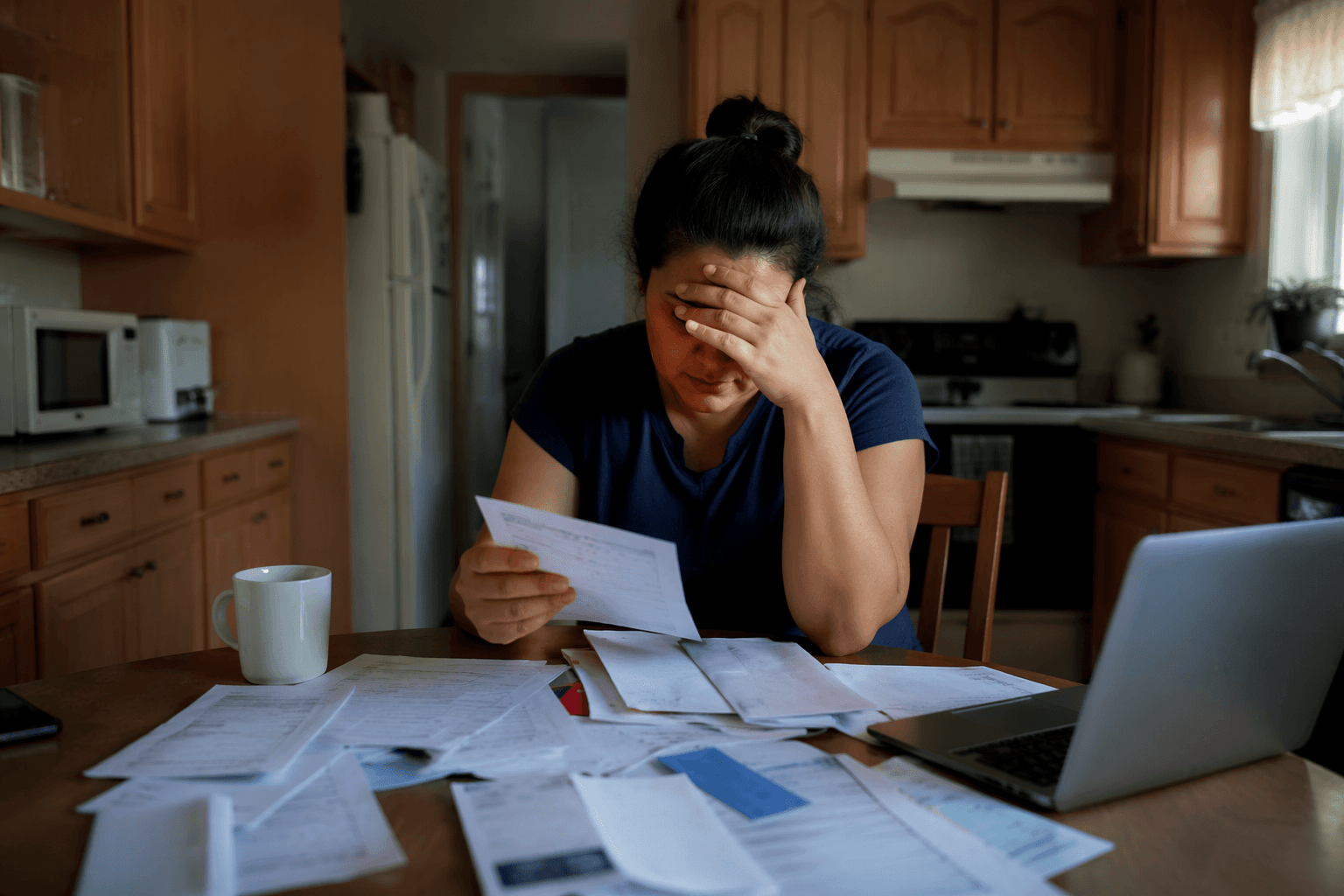

Americans are still making money decisions in a system that punishes small mistakes. The Federal Reserve’s latest household survey shows 27 percent of adults were just getting by or finding it difficult to get by, while inflation and prices remained the top financial concern. In that environment, weak financial literacy is not an abstract problem, it shows up as overdraft fees, unbanked households, and scam losses that many families cannot fully recover.

Where the pressure is showing up

The Fed’s Survey of Household Economics and Decisionmaking, fielded in October 2024 and published in May 2025, found that 73 percent of adults said they were doing okay financially or living comfortably. That was still below the 2021 high of 78 percent, a reminder that the recovery in household confidence remains incomplete even when the headline economy looks steadier. The same report found that 6 percent of U.S. adults were unbanked in 2024, with far higher unbanked rates among low-income adults, Black and Hispanic adults, and adults with disabilities.

The weaknesses do not stop at the bank branch door. Among banked adults, 11 percent said they paid an overdraft fee in the prior 12 months, a small number that becomes a real drag when money is already tight. The Fed also reported that adults of all incomes experienced financial fraud and scams, and many were unable to recover all of the money they lost. That is why financial literacy matters most in the places where Americans are most exposed, from checking-account balances and emergency savings to credit-card borrowing and the true cost of short-term debt.

Education and inequality shape the outcome

The gap in money confidence tracks closely with education. In the Fed’s 2025 findings, 87 percent of adults with at least a bachelor’s degree said they were doing okay financially or living comfortably, compared with 47 percent of adults with less than a high school degree. That spread is more than a measure of schooling. It signals how financial knowledge, bargaining power, and broader economic security often move together.

This matters because the hardest mistakes are usually the ones made under pressure. Misreading interest rates, misunderstanding debt terms, underestimating how inflation erodes purchasing power, or failing to build an emergency cushion can all become expensive when income is already stretched. When budgets are thin, a mistaken choice is not just a bad choice, it can mean higher monthly payments, delayed retirement saving, or a balance that lingers long after the original bill was paid.

Why the national picture is still fragile

Brookings has shown why these slips have such large consequences. In 2024, 45.5 percent of U.S. households did not earn enough to make ends meet, and more than 40 percent of American households struggled to make ends meet in nearly every year since 2014. That persistent affordability pressure helps explain why financial literacy is a national vulnerability, not a personal moral failing. When so many households are already operating close to the edge, even a small overdraft, a misjudged loan, or a scam loss can spill into missed rent, maxed-out cards, or depleted emergency savings.

The lesson is not simply that people need better habits. It is that the system asks families to navigate interest rates, price shocks, and debt contracts with very little room for error. In that setting, financial literacy becomes a form of household resilience, one that can determine whether a temporary setback stays temporary.

The evidence base points to where policy should focus

The FINRA Investor Education Foundation’s National Financial Capability Study gives policymakers a longer view of the problem. Launched in 2009, it was the first national study of the financial capability of U.S. adults, and it now includes six waves of data. Each wave surveys more than 25,000 adults across all 50 states and Washington, D.C., making it one of the clearest tools for seeing how money knowledge varies across the country.

The international picture reinforces the same warning. In June 2024, the OECD said more than two-thirds of students regularly use financial products and services, yet nearly one in five students in participating countries and economies did not reach baseline proficiency in financial literacy. OECD Secretary-General Mathias Cormann warned that rising financial frauds and scams make it even more important to equip young people with money skills. The OECD’s 2023 adult financial literacy survey also stressed that understanding current literacy levels is essential for effective policy and programming.

That is the practical takeaway for households and policymakers alike. The biggest vulnerabilities cluster around the basics that most people encounter every month: the cost of credit, the fine print on debt, the need for cash reserves, the math of retirement saving, and the growing risk of fraud. Until those gaps narrow, low financial literacy will keep turning ordinary money decisions into expensive mistakes.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip