Macy’s lifts forecast as quarterly sales return to growth

Macy’s posted its strongest first quarter in four years and raised guidance as Bloomingdale’s and Bluemercury outperformed the middle market.

Macy’s said its turnaround is gaining traction after first-quarter comparable sales rose 3.0%, the company’s strongest quarterly performance in four years, and net sales increased 1.8% to $4.68 billion. The department-store chain also lifted its full-year outlook, signaling that its push toward higher-end shopping is finding a customer even as the broad middle of the market remains under strain.

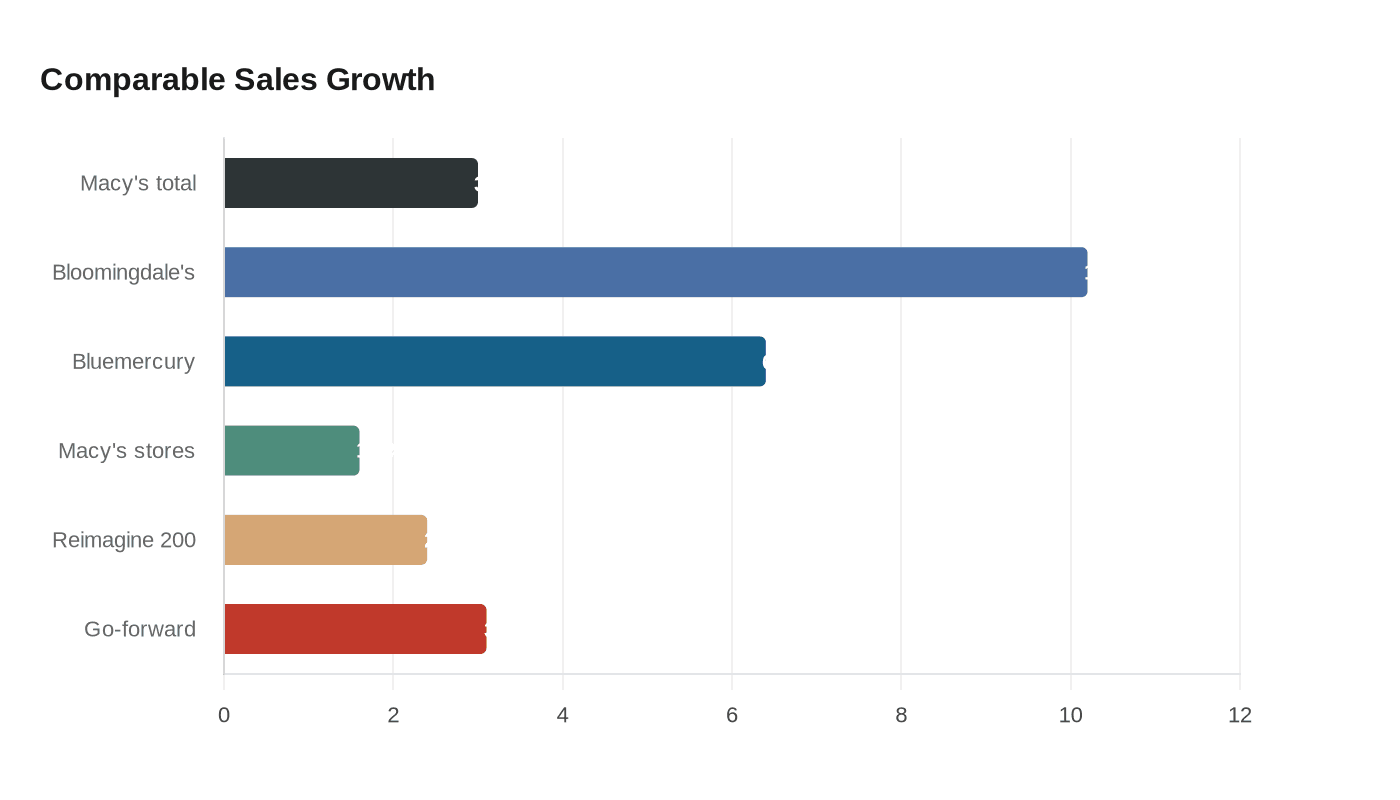

The clearest gains came from the company’s upscale banners. Bloomingdale’s comparable sales jumped 10.2%, its seventh straight quarter of gains, while Bluemercury rose 6.4%. Macy’s namesake stores posted a 1.6% increase, and comparable sales were positive across all three nameplates. The 200 locations in Macy’s “Reimagine 200” group, which have received heavier investment, produced 2.4% comparable-sales growth. Go-forward comparable sales rose 3.1%.

Chief executive Tony Spring said, “Customers are responding,” a sign of confidence that the company’s “Bold New Chapter” strategy is getting through. The plan has centered on modern luxury, stronger stores, full-price selling and the closure of weaker locations, a reset meant to pull Macy’s away from the tired department-store model that has been squeezed by changing shopping habits and harsher competition.

The results also offered a clean read on the split consumer economy. Higher-income shoppers are still spending on discretionary goods, especially in luxury apparel and accessories, while lower-income households remain more careful. Macy’s performance suggests that exposure to affluent customers can still move the needle, but it also raises a harder question for investors: whether this is a durable reinvention or a temporary lift helped by easier comparisons and a strong luxury mix.

Investors greeted the update with enthusiasm, sending shares up about 4% in premarket trading. Macy’s raised fiscal 2026 net sales guidance to $21.50 billion to $21.75 billion, from $21.40 billion to $21.65 billion, and increased its comparable-sales outlook to growth of 0.5% to 1.2%, from a prior range of a 0.5% decline to a 0.5% gain. Adjusted diluted earnings per share were raised to $2.00 to $2.20, from $1.90 to $2.10.

Profitability showed some pressure from trade costs. Gross margin was 38.9%, down 30 basis points, though Macy’s said it would have been flat excluding a 30-basis-point tariff hit. Credit card net revenues rose 11.7% to $172 million, and other revenue climbed 8.2% to $210 million, helping offset the strain.

For Macy’s, the quarter offered its strongest proof yet that its upscale pivot can work. The challenge now is making that progress last once luxury demand cools and the easy comparisons disappear.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?