Middle East Strikes Rattle Oil Markets, Pushing Risk Premiums Sharply Higher

Brent crude hit $112 a barrel as Middle East strikes triggered a two-day options frenzy, with nearly 20 million barrels of daily supply at risk through a near-idle Strait of Hormuz.

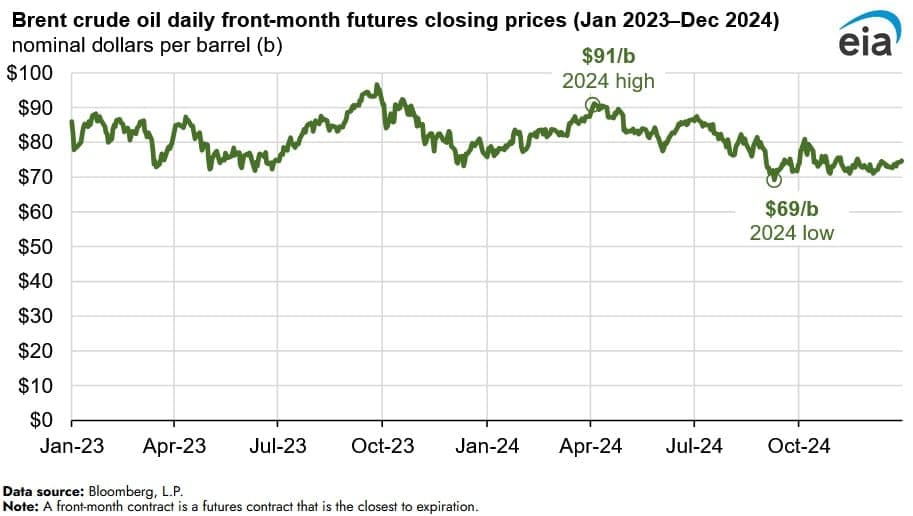

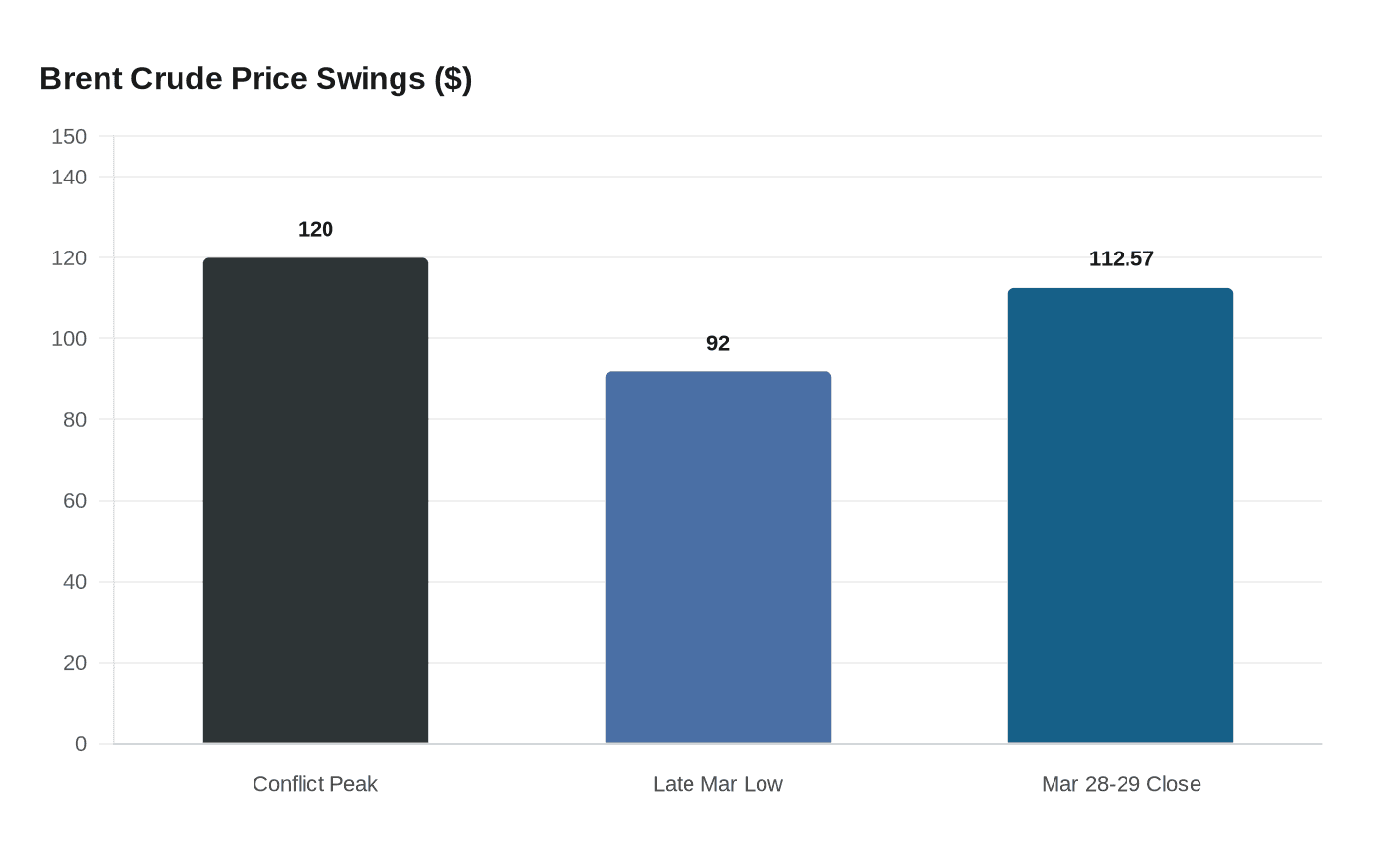

The last time West Texas Intermediate crude briefly crossed $100 a barrel, gasoline topped $5 a gallon in parts of the United States. That threshold fell again on March 27 when WTI surged $5.16, or 5.46%, to close at $99.64, with intraday trades clearing the century mark for the first time since mid-2022. By the following two days, as strikes and counterstrikes across Middle Eastern energy and industrial infrastructure continued to accumulate, the repricing had spread well beyond a single benchmark: Brent crude closed at $112.57, roughly 47% above the levels that prevailed before the first U.S. and Israeli strikes on Iran in February.

For American drivers, the arithmetic carries a predictable but painful delay. Retail gasoline prices typically lag crude benchmarks by two to three weeks on the way up, as refiners absorb initial margin compression before passing costs downstream. That puts a mid-April reckoning squarely in view, with national pump prices already tracking in the $4.10-to-$4.30-per-gallon range under current conditions, a figure that could move higher if the Strait of Hormuz remains effectively paralyzed.

The strait sits at the physical center of the market's anxiety. Traffic through the approximately 100-mile-long waterway has stalled, and the International Energy Agency calculates that nearly 20 million barrels per day of crude and product exports are now disrupted, a volume representing close to 20% of global supply that ordinarily transits that single chokepoint. Brent futures pierced $120 a barrel earlier in the conflict before diplomatic signals in late March briefly pushed prices back toward $92. The resumption of strikes on energy infrastructure then drove the sharp two-day reversal that defined the March 28-29 session.

What made those sessions structurally unusual was the activity beneath the price moves. Exchanges reported abnormal order flow concentrated in contracts tied to Middle East crude grades and insurance-linked instruments. Block trades in options and sharp increases in open interest in specific futures contracts drew scrutiny from market participants, with several telling Reuters the patterns were consistent with large speculative wagers. Trading firms described deploying a combination of outright crude purchases, options-based protection, and swaps: some to hedge existing exposures, others to place directional bets on continued price gains.

The volatility cascaded across related markets simultaneously. Crude futures and energy equities were bid up at different intervals over the two days, while some funds turned to index options and structured products to express short-term directional views. Shipping rates and war-risk insurance premiums moved in tandem, creating interlocking liquidity pressures that complicated even sophisticated hedging strategies.

Traders on major commodity desks described the market as "on edge," with the risk premium rising sharply after confirmed strikes on Gulf energy and industrial facilities. The deeper concern, energy analysts stressed, was not the infrastructure damage already recorded but the prospect of prolonged disruption. Iran alone produces roughly 3.4 million barrels a day; a strike on its production capacity, layered on top of a Hormuz blockage already straining global flows, would remove supply from markets with no near-term substitute.

For regulators, the concentrated, rapid flows tied to specific geopolitical developments present a familiar evidentiary challenge: distinguishing legitimate hedging from activity that may have benefited from non-public knowledge of imminent military action. Exchanges are expected to review the abnormal order patterns. For corporate energy consumers, the episode carries a more immediate conclusion: the conditions that once qualified as tail risks have become operating assumptions.

Know something we missed? Have a correction or additional information?

Submit a Tip