MobiKwik targets 50-billion-rupee loan book as it expands lending

MobiKwik is betting its new lending licence can turn a payments giant into a balance-sheet lender, but the move raises the stakes on defaults and regulation.

MobiKwik is targeting a 50-billion-rupee loan book over the next three to five years, a move that would push the Gurugram-based fintech much deeper into balance-sheet lending and far beyond its roots as a loan distributor. The company’s new ambition rests on an April approval from the Reserve Bank of India for a non-bank lending licence, giving its in-house arm the ability to originate and hold loans itself instead of routing credit through partner lenders.

That shift changes the business in a fundamental way. As a lending-service provider, MobiKwik could earn fees while leaving most of the credit risk elsewhere. As a lender, it will have direct exposure to repayments, underwriting errors and losses if borrowers weaken. MobiKwik’s expansion therefore hinges not just on growth, but on whether it can build enough underwriting discipline, data-driven risk controls and collections muscle to support a larger loan book without damaging asset quality.

The company said on April 27, 2026 that the licence would enable MobiKwik Financial Services Private Limited, a wholly owned subsidiary, to expand regulated lending capabilities, design new credit products and serve a broader base of consumers and merchants. That broader merchant focus matters. MobiKwik has long been known for payments and personal-finance products, but the new lending push suggests a bid to use its platform more aggressively as a distribution engine for credit.

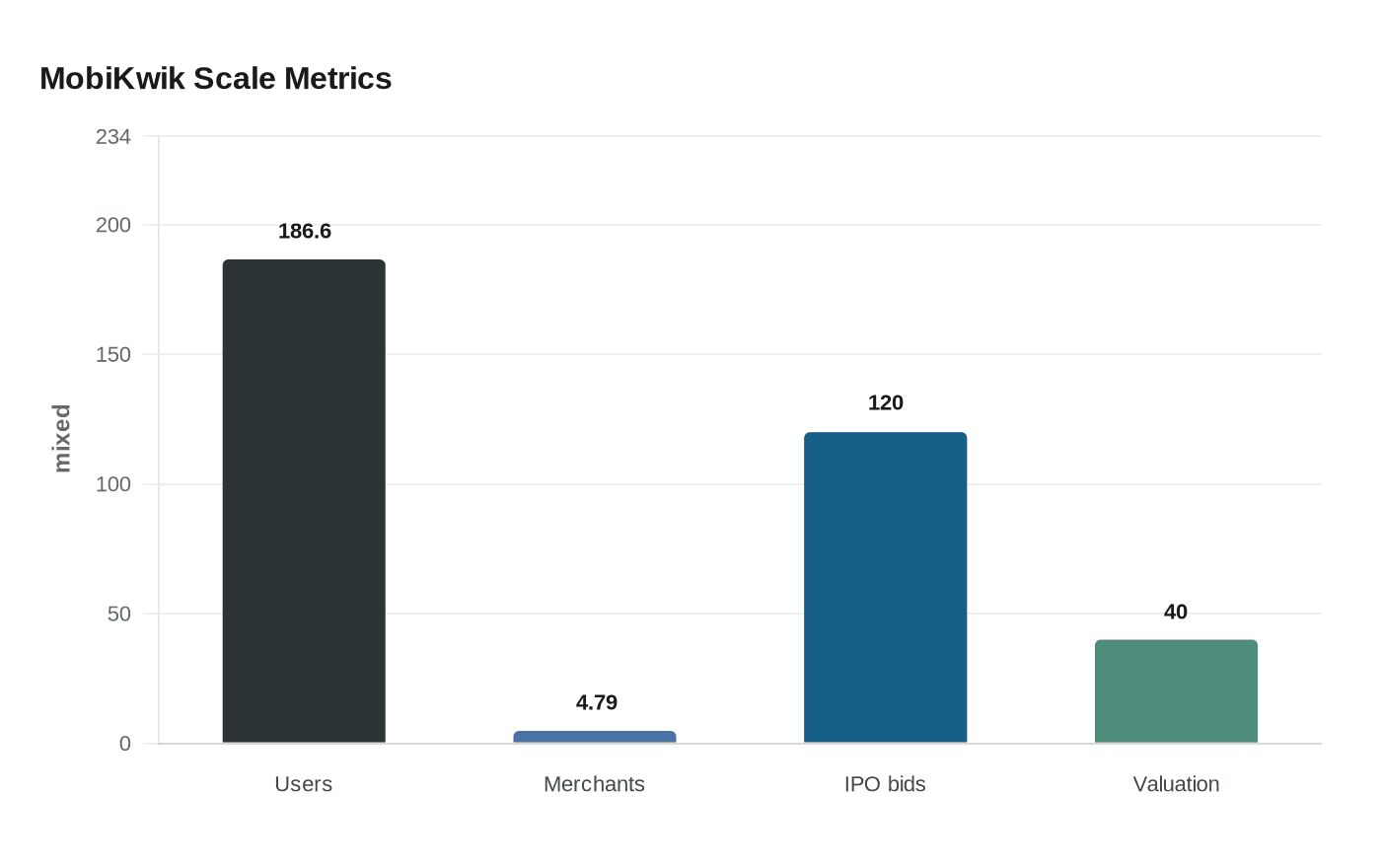

The scale of that platform gives MobiKwik a meaningful base to work from. In investor materials, the company says it is India’s largest digital wallet, with more than 186.6 million users and more than 4.79 million merchants. The company’s recent strategy materials also point to a wider push to reinvest profits from its core payments and financial-services business into new growth engines, including merchant payments.

Investors have already priced MobiKwik as a growth story. Its December 2024 IPO drew bids for about 120 times the shares on offer, and its market debut valued the company at about 40 billion rupees, or $474 million. MobiKwik has also said its core payments and financial-services business generated about 50 crore rupees of EBITDA in FY26, adding another layer of pressure to convert operating momentum into a larger, better-controlled lending franchise.

The next phase will test whether MobiKwik can move from platform economics to credit economics. For India’s fintech sector, the question is no longer only who can distribute loans fastest, but who can hold them, manage them and satisfy regulators as digital finance matures.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip